Introduction

Nonprofits face unprecedented financial volatility. 36% of nonprofits ended 2024 with an operating deficit—the highest rate in a decade—while 85% expect service demand to increase in 2025. Add variable grant funding, donor uncertainty, shifting regulations, and inflation-driven cost pressures, and structured financial risk assessment isn't optional. It's foundational to mission continuity.

The exposure runs deep across two distinct fronts. Without government grants, 60% to 86% of nonprofits in every state would have operated at a loss from 2021 to 2023. On the compliance side, approximately 275,000 501(c)(3) organizations lost tax-exempt status in the initial 2010–2011 automatic revocation wave alone. Both funding dependency and regulatory failure are recurring, quantifiable risks — not edge cases.

This guide walks you through how to define financial risk in a nonprofit context, identify the five core risk types, conduct a step-by-step assessment, and act on findings with targeted mitigation strategies that go beyond simply building reserves.

Key Takeaways

- Financial risk assessment identifies funding, operational, and compliance threats before they escalate into crises

- Core risk types include funding concentration, operational gaps, compliance failures, market volatility, and reputational damage

- A structured process scores each risk by likelihood and impact, then assigns clear ownership for follow-through

- Mitigation means diversifying revenue, tightening controls, and monitoring consistently—not simply building reserves

What Is Financial Risk Assessment for Nonprofits?

Financial risk assessment is the systematic process of identifying, analyzing, and prioritizing financial threats that could prevent a nonprofit from sustaining operations or achieving its mission.

Unlike general risk management—which covers programmatic, strategic, and reputational risks broadly—financial risk assessment focuses exclusively on financial threats: funding gaps, compliance violations, fraud exposure, cash flow shortfalls, and revenue concentration.

Nonprofit financial risk differs from for-profit risk in several structural ways:

- Restricted funds: Nonprofits manage multiple funding streams with donor-imposed restrictions, creating complex compliance requirements

- Thin margins: Operating surpluses are typically narrow or nonexistent, leaving little cushion for disruption

- External dependency: Revenue relies on grants, donations, and contracts outside the organization's direct control

- Elevated compliance obligations: IRS Form 990 filings, state charitable registrations, grant-specific spending rules, and restricted fund tracking create layers of regulatory exposure

These factors make the assessment process itself a distinct discipline. A financial risk assessment is the diagnostic phase — it produces the intelligence that precedes response strategy, identifying which risks warrant immediate mitigation, which require monitoring, and which can be deprioritized.

The Main Types of Financial Risk Nonprofits Face

Funding Risk

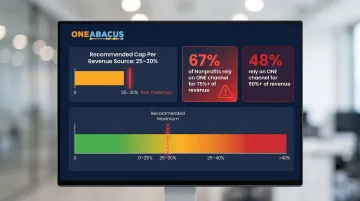

Over-reliance on one or two revenue streams creates concentration risk. If a single federal grant, major donor, or annual gala represents 30% or more of total revenue, the organization faces immediate operational jeopardy if that source disappears.

Nonprofits received approximately one-third of their revenue from government agencies in recent years, totaling $240 billion in 2023. In 2022 and 2023, no congressional district in the US had a typical nonprofit that could operate without government grants — and 84% of nonprofits receiving government funding expect cuts in the near future.

Industry best practice suggests no single revenue source should exceed 25-30% of total revenue. Yet two out of three nonprofits rely on a single revenue channel for more than 75% of their revenue, and nearly half rely on one channel for more than 90%.

Operational Risk

Operational risks stem from internal processes: cost overruns, staffing gaps, fraud, vendor dependency, and inadequate financial controls. Small finance teams have limited bandwidth for oversight, which compounds every other vulnerability on this list.

The financial exposure here is real. The median nonprofit fraud loss is $76,000 per case, with 48% of cases attributed to weak internal controls. Organizations with fewer than 100 employees face median losses of $141,000 — potentially devastating on a tight budget.

Staffing shortages make this worse:

- 65% of nonprofits report staffing shortfalls

- 77% struggle to recruit senior leadership

- 75% have eliminated staff positions entirely

Each gap reduces oversight capacity and creates new entry points for error or fraud.

Compliance Risk

Failure to meet IRS reporting requirements, state charitable solicitation registrations, grant-specific spending rules, or restricted fund tracking can trigger financial penalties, audit flags, or loss of tax-exempt status.

Organizations that fail to file Form 990 for three consecutive years automatically lose tax-exempt status. Approximately 275,000 501(c)(3) organizations lost status in the initial 2010-2011 wave, with roughly 28,000 additional revocations annually from 2012-2017. Between revocation and reinstatement, organizations operate as taxable entities and donors cannot claim deductions.

State charitable solicitation registration compounds the risk. 38 states plus DC enforce registration requirements, with penalties ranging from fines to felony charges in Ohio and Florida. One documented case resulted in 10 separate state violations totaling $50,000 in penalties.

Market and Economic Risk

Economic downturns affect donor generosity, investment portfolio values, and operating costs simultaneously. Interest rate changes increase debt service burdens, while inflation erodes purchasing power and drives up labor costs. Many nonprofits assume donor behavior is insulated from economic cycles — the data says otherwise:

- Total US charitable giving fell 10.5% in inflation-adjusted terms in 2022, only the fourth current-dollar decline in 40 years

- Individual giving dropped 13.4% inflation-adjusted that same year

- Total giving fell 13.4% combined over the 2008-2009 Great Recession

- 86% of nonprofit respondents reported inflation negatively impacted their organizations in 2024

Reputational Risk with Financial Consequences

Financial mismanagement—even unintentional—erodes donor trust and triggers rapid declines in contributed revenue. Poor financial transparency, missed grant deadlines, inaccurate Form 990 filings, or audit findings create reputational damage that directly impacts funding.

Watchdog organizations enforce financial transparency standards. BBB Wise Giving Alliance requires at least 65% program spending; Charity Navigator prefers 70% or more. Falling short signals inefficiency to donors, foundations, and institutional funders who screen nonprofits using these ratios.

How to Conduct a Nonprofit Financial Risk Assessment

A financial risk assessment requires examining both internal financial structure and the external funding environment. It should involve board leadership, the CFO (or equivalent), and program directors—not just finance staff. Cross-functional input surfaces risks finance teams wouldn't see.

Step 1: Map Your Financial Landscape

Revenue review:

- Categorize all revenue streams by source type (grants, donations, earned income, investments)

- Identify restriction levels (unrestricted, temporarily restricted, permanently restricted)

- Assess reliability and renewal likelihood for each source

- Flag any single source representing more than 25-30% of total revenue as concentration risk

Expense audit:

- Separate fixed costs (rent, salaries, debt service) from variable costs

- Calculate payroll as a percentage of total expenses

- Document long-term contractual obligations that cannot easily be reduced

- Identify vendor dependencies or single-source contracts

This landscape map establishes your baseline financial profile and exposes structural vulnerabilities.

Step 2: Identify and Categorize Financial Risks

Use the five risk categories—funding, operational, compliance, market, reputational—as a structured lens. Document both known risks and hypothetical scenarios: "What happens if our largest grant is not renewed?" or "What if our development director leaves mid-campaign?"

Common tools at this stage:

- SWOT analysis (Strengths, Weaknesses, Opportunities, Threats)

- Financial trend review over 3-5 years to identify patterns

- Stakeholder interviews with program and development staff who surface operational and pipeline risks finance staff may not see

Encourage teams to think broadly. Compliance risks often hide in grant agreements, while operational ones surface in conversations about staffing gaps or manual workarounds. Weak donor communication practices are a common—and frequently overlooked—source of reputational exposure.

Step 3: Score and Prioritize Each Risk

Assign each identified risk two scores:

- Likelihood: Low, medium, or high probability of occurrence

- Impact: Minor, moderate, or severe financial consequence if it occurs

Plot risks on a 2x2 matrix:

- High likelihood + high impact: Immediate mitigation required

- High likelihood + low impact: Monitor and address proactively

- Low likelihood + high impact: Develop contingency plans

- Low likelihood + low impact: Document but deprioritize

A three-level financial risk profile framework helps boards calibrate the scale of response required:

| Profile Level | What It Looks Like |

|---|---|

| Stable | Risks identified and managed; reserves adequate; controls strong |

| At Risk | Concentration risk present; reserves below benchmark; compliance gaps exist |

| Crisis | Active funding shortfall; structural deficits; programs or tax-exempt status threatened |

This profile helps boards understand whether tactical fixes suffice or structural intervention is needed.

Step 4: Document, Assign, and Monitor

Formalize findings into a written risk register that captures:

- Each identified risk

- Likelihood and impact scores

- Assigned owner responsible for monitoring or mitigation

- Planned response or mitigation strategy

- Review timeline

- Scheduled review cadence (at minimum annually, and after major funding changes, leadership transitions, or regulatory shifts)

Without a written register, the assessment loses its impact the moment the meeting ends.

How to Act on Your Risk Assessment: Mitigation Strategies That Work

Build (and Right-Size) Operating Reserves

A reserve fund is the most direct buffer against funding disruptions. The standard benchmark is 3-6 months of operating expenses, though the right target depends on your revenue volatility and risk profile. According to the NFF State of the Nonprofit Sector Survey, 52% of nonprofits hold 3 months or less of cash on hand, and 18% have one month or less. These organizations are one grant delay away from a payroll crisis.

Reserves should not exceed two years' budget, but the floor is three months' expenses. Organizations with volatile revenue, seasonal funding, or single-funder concentration should target the upper end of the 3-6 month range.

Diversify Revenue Streams

Concentration risk requires long-term structural response. Strategies include:

- Expanding the individual donor base through planned giving, monthly giving, or mid-level donor programs

- Developing earned income programs that align with mission and leverage existing capacity

- Pursuing a broader mix of government, foundation, corporate, and individual giving

Diversification takes time and must be planned proactively. A nonprofit cannot launch a major donor program mid-crisis — build pipeline now, before concentration risk materializes.

Strengthen Internal Controls

Key financial controls reduce operational and compliance risk:

- Dual authorization for payments above a set threshold (e.g., $5,000)

- Monthly reconciliations of all accounts

- Segregation of duties so no single person controls both authorization and execution

- Timely board financial reporting with variance analysis and cash flow projections

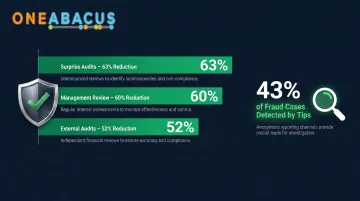

Research shows that surprise audits reduce fraud losses by 63%, management review by 60%, and external audits by 52%. Even modest investments in controls yield measurable risk reduction. Organizations with formal reporting mechanisms (hotlines, web forms, email) detect fraud more frequently, as 43% of all fraud is detected by tips.

Maintain Compliance Vigilance

Compliance risk is often underestimated by smaller nonprofits. Assign clear ownership of:

- Form 990 preparation and filing deadlines

- Grant reporting and drawdown schedules

- Restricted fund tracking and expenditure documentation

- State charitable solicitation registration renewals

Many compliance failures result from missed deadlines or unclear ownership, not deliberate wrongdoing. A compliance calendar with assigned owners and automated reminders prevents costly oversights.

Consider Structural Responses for High-Risk Profiles

Organizations in the "Significant Areas at Risk" or "Existential Redefinition" categories may need more substantial responses:

- Program consolidation to align capacity with sustainable funding

- Outsourcing back-office functions to improve efficiency and reduce fixed costs

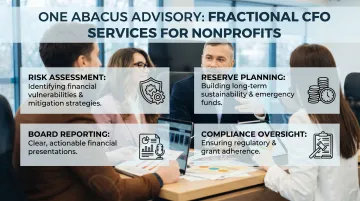

- Engaging a fractional CFO to provide financial leadership at a fraction of the cost of a full-time hire

This is where One Abacus Advisory's fractional CFO and COO services are built to help. Founder Lorin Port brings over 25 years of finance and accounting experience, with nine years focused exclusively on nonprofits, working with organizations like the San Diego Food Bank and Philadelphia Zoo. For nonprofits navigating high-risk periods, that kind of focused expertise — available on a right-sized, cost-effective basis — can make the difference between stabilization and crisis.

How One Abacus Advisory Can Help

One Abacus Advisory serves as a fractional CFO and financial leadership partner for nonprofits navigating financial risk, leadership transitions, and operational complexity. Rather than hiring a full-time CFO to lead the risk assessment process, nonprofits get senior-level financial expertise scaled to their actual needs.

Services include:

- Financial risk assessment: Identifying, scoring, and prioritizing financial threats across funding, operations, compliance, and market exposure

- Operating reserve planning: Cash flow analysis and scenario modeling to right-size reserves based on your risk profile

- Board reporting: Clear, actionable financial analysis that supports governance and strategic decision-making

- Compliance oversight: Audit preparation, internal controls assessment, regulatory compliance, and risk management support

One Abacus has supported organizations including the San Diego Food Bank and Philadelphia Zoo through leadership transitions, financial system optimization, and audit preparation. During the Philadelphia Zoo's CFO and Controller transition, One Abacus conducted a comprehensive accounting assessment, optimized their NetSuite environment, improved month-end close processes, and supported executive financial literacy — without disrupting a lean internal finance team.

Whether you're preparing for an audit, navigating a leadership gap, or facing pressure on reserves, One Abacus provides the financial leadership to address those risks before they become crises.

Ready to assess your financial risk profile? Contact One Abacus Advisory for a consultation to identify your highest-priority gaps and build a response plan that protects your mission.

Frequently Asked Questions

What are the main types of financial risk for nonprofits?

The five core categories are funding risk (over-reliance on a narrow revenue base), operational risk (fraud, staffing gaps, weak controls), compliance risk (Form 990 failures, state registration lapses), market risk (economic downturns, donor volatility), and reputational risk (financial mismanagement eroding trust). Funding and compliance risks tend to be most acute for nonprofits.

Is there a nonprofit financial risk rating system and what are the rating levels?

No universal standard exists, but a widely referenced 3-level model rates nonprofits as: Minimal Expected Impact (reserves adequate, risks managed), Significant Areas at Risk (concentration risk, compliance gaps, reserves below benchmark), or Existential Redefinition (structural deficits, immediate funding crisis). Severity is determined by funding disruption potential and reserve strength.

What are common financial challenges faced by nonprofit organizations?

The most common challenges are revenue volatility, narrow funding bases, restricted fund complexity, lean finance staffing, and thin operating reserves. The numbers reflect this: 52% of nonprofits hold 3 months or less of cash on hand, and 36% ended 2024 with operating deficits—the highest rate in a decade.

What are common financial rules of thumb for nonprofits (e.g., 33% rule, 80/20 rule, 5% rule)?

Three benchmarks matter most: maintain 3-6 months of operating expenses in reserves, keep no single funder above 25-30% of total revenue, and direct at least 65-70% of spending to program activities. BBB Wise Giving Alliance sets the floor at 65%; Charity Navigator's preferred threshold of 70%+ signals stronger donor confidence.

What are common 501(c)(3) compliance issues?

The most frequent violations are late or inaccurate Form 990 filing (three consecutive missed years triggers automatic revocation), lapsed state charitable solicitation registrations (required in 38 states plus DC), improper restricted fund handling, unrelated business income issues, and political activity violations. About 275,000 organizations lost tax-exempt status during the 2010-2011 automatic revocation wave alone.

How often should a nonprofit review and update its financial risk assessment?

At least annually—ideally timed to strategic planning or budget cycles. Immediate review is required when major funding changes occur, a key funder exits, leadership transitions happen, or the regulatory environment shifts significantly. Organizations in high-risk categories should review quarterly or semi-annually to monitor emerging threats.