Introduction

Most nonprofit boards spend less than 20 minutes reviewing financial statements at quarterly meetings — then file them away until the next audit. That's a costly habit. These reports should be driving decisions about program funding, cash reserves, and whether the organization can survive a slow fundraising quarter.

The four core nonprofit financial statements — Statement of Activities, Statement of Financial Position, Statement of Cash Flows, and Statement of Functional Expenses — each answer a distinct question about organizational health. Understanding what each one tells you (and what warning signs to watch for) is what separates leaders who react to financial problems from those who prevent them.

Key Takeaways

- Nonprofits produce four core financial statements, each serving a different strategic purpose: financial performance, financial position, liquidity, and mission alignment

- Unlike for-profit statements, nonprofit financials reflect fund restrictions and functional expense reporting

- Regular review—not just at audit time—is essential for board oversight and long-term financial health

- You don't need to be an accountant—you need to know what questions each statement should answer

Why Nonprofit Financial Statements Matter Beyond Compliance

Yes, these statements satisfy GAAP requirements and feed into Form 990 filings. But their real value is as management tools—for spotting trends, comparing actuals to budget, and informing strategic decisions. Nearly 75% of nonprofit leaders report dealing with cash flow problems at least occasionally, and 54% must reforecast budgets quarterly or more often. Reliable financial statements are the foundation for identifying these issues before they become crises.

Outside your organization, financial statements directly shape funding decisions. Donors, grant-makers, and lenders all use them to assess stability before committing resources. Strong, readable statements build trust during grant applications, audits, and board transitions. The BBB Wise Giving Alliance Standard 11 requires charities to make complete annual financial statements prepared in accordance with GAAP available to all on request — a baseline that most funders now expect as a matter of course.

Meeting those expectations requires more internal capacity than many nonprofits have. The staffing reality is telling:

- 30% of nonprofits currently outsource finance and accounting functions

- 72% deal with turnover in finance and accounting roles at least occasionally

- Most small to mid-size organizations operate without a dedicated CFO

For these organizations, expert financial leadership — such as fractional CFO services — adds value not just by compiling statements, but by interpreting and presenting them in ways boards can actually act on.

For example, during a leadership transition at the Philadelphia Zoo, One Abacus Advisory provided fractional CFO support that restructured financial systems, accelerated month-end close processes, and enhanced board reporting. The result was continuity through a complex transition, with an executive team better equipped to make financial decisions going forward.

Statement of Activities

What It Includes

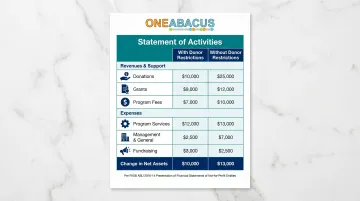

Think of this as the nonprofit equivalent of an income statement. It captures all revenue and support—individual donations, grants, program fees, in-kind contributions, investment returns—and all expenses over a defined period, typically a fiscal year.

Nonprofits organize expenses by function rather than type, unlike for-profit income statements. Under GAAP, the three functional expense categories are:

- Program services – direct mission work

- Management and general – governance and administrative support

- Fundraising – donor cultivation and solicitation

The statement uses a restricted vs. unrestricted column structure. Following FASB ASU 2016-14, the terminology changed to "with donor restrictions" vs. "without donor restrictions." This distinction is critical: it reveals how much of your revenue you can actually direct freely toward mission work versus amounts earmarked by donors for specific purposes.

Why It Matters for Leadership

This statement answers the question: "Are we operating at a surplus or deficit?" Comparing it line-by-line against the operating budget reveals whether revenue assumptions held and where expense categories ran over or under.

A common leadership mistake: viewing a net surplus as "we're fine" without examining whether that surplus is mostly restricted funds. Your organization might show a $200,000 surplus on paper, but if $180,000 is restricted to a specific capital project, you have only $20,000 in unrestricted growth — which tells a very different story about operational health.

Statement of Financial Position

What It Includes

This is the nonprofit balance sheet: a point-in-time snapshot structured as Assets = Liabilities + Net Assets. It lists:

- Current and noncurrent assets (in order of liquidity)

- Current and long-term liabilities (in order of due date)

- Net assets broken into with- and without-donor-restriction categories

Three line items that frequently trip up nonprofit leaders:

- Pledges receivable – promises to give, not yet cash

- Deferred revenue – payments received for services not yet delivered

- Board-designated net assets – unrestricted funds the board has earmarked for specific future uses (distinct from donor-restricted funds, and visible to auditors and grant-makers)

Why It Matters for Leadership

This statement answers key questions: Can we cover next month's obligations? How much of our net assets are actually liquid? Do we have adequate operating reserves?

Consider this scenario: an organization with $500,000 in positive net assets but minimal unrestricted cash. Most of those assets might be tied up in a building, endowment investments, or multi-year pledges not yet collected. Net assets ≠ financial health.

The Nonprofit Finance Fund's 2025 survey found that 52% of respondents have three months or less of cash on hand, and 18% have one month or less.

Grant-makers and lenders typically request the Statement of Financial Position first when evaluating organizational stability, making it one of the most externally scrutinized of the four statements.

Statement of Cash Flows

This statement classifies cash flows into three sections:

- Operating activities – day-to-day cash in and out

- Investing activities – long-term asset purchases/sales

- Financing activities – loan proceeds, debt repayments, donor-restricted endowment contributions

Why Cash Flow Is a Separate Statement

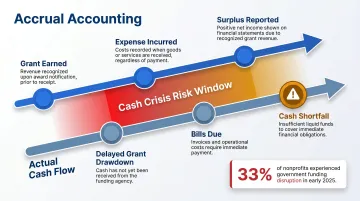

Accrual accounting records revenue when earned and expenses when incurred — but the Statement of Cash Flows tells you when actual dollars move. A nonprofit can show a surplus on its Statement of Activities and still face a cash crisis if large restricted grants haven't been drawn down or major expenses come due before pledges are collected.

That gap between accrual-based reporting and real cash on hand is one of the most common — and painful — surprises for nonprofit leadership.

In early 2025, 33% of all nonprofits experienced at least one type of government funding disruption, with 27% reporting delays, pauses, or freezes in government funding. For organizations relying on reimbursement-based grants, that timing gap isn't theoretical — it's a cash flow crisis waiting to happen.

Review this statement monthly, not just annually. Tracking the ending unrestricted cash balance as a trend line gives leadership an early warning system for liquidity problems before they become urgent.

Statement of Functional Expenses

This statement uses a matrix structure:

- Rows: Natural expense categories (salaries, occupancy, professional fees, depreciation)

- Columns: Functional categories (program services, management and general, fundraising)

This layout shows not just what was spent but why, making it unique among financial statements. Following FASB ASU 2016-14, all nonprofits—not just voluntary health and welfare organizations—must now provide this analysis in one location: on the face of the statement of activities, as a separate statement, or in the notes.

The Allocation Challenge

Some expenses fall entirely in one column (a grant writer's salary goes to fundraising). But many—an executive director's time, occupancy costs—must be allocated across multiple functional categories using a documented, consistently applied methodology. Auditors and sophisticated funders will scrutinize that methodology.

Common accepted methodologies under GAAP include:

- Time-and-effort studies

- Square footage allocation

- Headcount

- Direct identification

- Other reasonable bases

The Overhead Ratio Conversation

The BBB Wise Giving Alliance Standard 8 recommends charities spend at least 65% of total expenses on program activities and no more than 35% on fundraising. These benchmarks are widely cited but increasingly questioned by sector leaders.

In October 2014, the CEOs of GuideStar, Charity Navigator, and BBB Wise Giving Alliance issued a joint letter urging nonprofits to "crush the overhead myth" and help move past the false notion that overhead ratios alone determine charity trustworthiness. The takeaway for nonprofit finance leaders: no universal right ratio exists. What auditors and informed funders actually want to see is a documented allocation methodology, consistent application year over year, and a clear narrative explaining how resource decisions serve the organization's mission.

How the 4 Statements Work Together — and What Leaders Should Do Next

The four reports are interconnected and must be read as a set:

- The change in net assets on the Statement of Activities ties directly to the net asset balances on the Statement of Financial Position

- Cash flows explain why the cash line on the balance sheet changed

- The functional expense breakdown feeds both Form 990 Part IX and the expense totals on the Statement of Activities

A Practical Framework for Board Review

At each quarterly board meeting, present all four statements alongside a short narrative that addresses:

- Are we on track versus budget?

- Are we liquid enough to meet near-term obligations?

- Is our program spending ratio trending in the right direction?

- Are there any trends in restricted fund balances that require attention?

For most nonprofit leaders, the challenge isn't producing these statements — it's knowing what questions to ask when reviewing them. During a crisis period, One Abacus Advisory partnered with Laguna Playhouse to manage day-to-day accounting operations and complex audit preparation. That hands-on support gave both staff and the board a clearer picture of where the organization stood and what needed to change.

Fractional CFO support helps bridge that gap — contextualizing the numbers, flagging trends before they become problems, and connecting financial data to the decisions boards actually need to make.

Frequently Asked Questions

What financial statements do nonprofit organizations prepare?

Nonprofits produce four statements under GAAP: the Statement of Activities, Statement of Financial Position, Statement of Cash Flows, and Statement of Functional Expenses. The functional expense analysis can appear on the face of the Statement of Activities, as a separate statement, or in the notes.

What is a P&L called for a nonprofit organization?

The nonprofit equivalent of a profit and loss statement is the Statement of Activities. It summarizes revenues, expenses, and the change in net assets for a given period, organized by functional expense categories and net asset class.

What financial reporting is required for 501(c)(3) organizations?

501(c)(3) organizations must file Form 990 annually with the IRS (with different versions based on gross receipts thresholds), provide GAAP-compliant financial statements for audits and many grant agreements, and comply with state-level reporting requirements that vary by jurisdiction.

Are nonprofits required to have audited financial statements?

There is no universal federal requirement, but many states require audits above certain revenue thresholds. Nonprofits that expend $1,000,000 or more in federal awards must have a single audit conducted. Many funders and lenders contractually require audited statements regardless of legal mandates.

What should be included in notes to nonprofit financial statements?

Notes are required GAAP disclosures that accompany the financial statements. They typically cover accounting policies, donor restrictions, pledges and grants receivable, debt terms, liquidity, expense allocation methodology, and significant estimates.

Why are nonprofit financial statements important?

Externally, they demonstrate accountability to donors, funders, and the public. Internally, they give nonprofit leaders the data they need for budgeting, strategic planning, and risk management—supporting sound decisions at every level of the organization.