Introduction

Assessing for-profit financial performance is relatively straightforward: profit, loss, and margins tell most of the story. Nonprofit financial performance requires a different lens entirely. Unlike businesses driven by shareholder value, nonprofits advance public interest missions—which means a financial "loss" may represent intentional reinvestment in future capacity rather than operational failure.

Without a structured approach, nonprofit boards and executives risk misreading their organization's true health. Restricted grant funds get mistaken for real surplus. Warning signs buried in net asset balances go unnoticed. Funders who expect both transparency and results lose confidence.

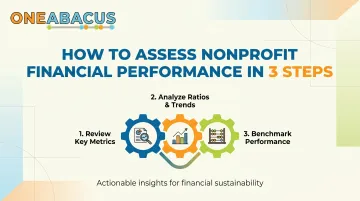

The three-step framework outlined here provides a practical methodology for accurately evaluating nonprofit financial health—showing whether your organization is genuinely sustainable or burning through reserves while appearing stable on paper.

What You Need Before You Begin

To run this assessment, you'll need four core financial documents:

- Statement of Financial Position (Balance Sheet): Reports assets, liabilities, and net assets at a specific point in time, with net assets classified as "with donor restrictions" or "without donor restrictions." Reveals liquidity and solvency.

- Statement of Activities (Income Statement): Reports changes in net assets over a period—revenue, gains, expenses, and losses. Shows operational sustainability and whether the organization generates surpluses.

- Statement of Cash Flows: Tracks cash inflows and outflows through operating, investing, and financing activities. Reveals cash management health and ability to fund operations.

- Budget-to-Actual Reports: Management-level reports comparing planned versus actual performance, essential for identifying variances and course-correcting mid-year.

Accurate, GAAP-compliant records are a prerequisite. Organizations without dedicated financial leadership often lack clean, reliable data to work from. For organizations navigating that gap, fractional CFO services like those offered by One Abacus Advisory ensure the underlying data is trustworthy before any assessment begins. According to the National Council of Nonprofits 2023 Workforce Survey, 74.6% of nonprofits reported job vacancies in financial roles, making access to experienced financial leadership increasingly critical.

Key Takeaways

- Standard profit-focused metrics don't apply to nonprofits — financial health here means sustainability, mission alignment, and liquidity

- The 3-step approach covers separating discretionary from non-discretionary spending, running pro forma scenarios, and building a mission impact narrative

- Key gauges include liquidity (aim for 3–6 months of reserves), unrestricted revenue share, and expense allocation ratios

- Common mistakes include treating all revenue as accessible and ignoring restricted vs. unrestricted fund differences

- Monthly assessments give boards the visibility to act proactively, not just respond to crises

Step 1: Separate Discretionary from Non-Discretionary Spending

Unlike for-profit income statements, a nonprofit's Statement of Activities does not need to show a net surplus every year—which makes it easy to misread whether the organization is truly financially healthy. The core concept: not all expenses are created equal.

Defining Non-Discretionary Expenses

Non-discretionary expenses are costs required to deliver on the current year's mission goals, directly tied to that year's revenue. Examples include:

- Program staff salaries

- Occupancy costs tied to direct services

- Grant-required expenditures

- Essential supplies and materials

Non-discretionary expenses should be lower than revenue—leaving a margin for reinvestment and growth.

Defining Discretionary Expenses

Discretionary expenses are funds deliberately reinvested to strengthen the organization's future capacity. These are choices, not obligations—and they signal organizational health:

- Staff development and training

- Technology upgrades and infrastructure

- New program pilots

- Reserve building and strategic initiatives

With both categories defined, the next step is putting this distinction to work in your actual reporting.

How to Separate These Categories in Practice

Create a modified income statement for management reporting where expenses are explicitly labeled as discretionary or non-discretionary, separate from the standard GAAP presentation.

This format lets you calculate a "core surplus" figure. If non-discretionary revenue reliably exceeds non-discretionary expenses, the organization has genuine economic value creation—even when the bottom line looks break-even or slightly negative due to reinvestment spending.

This distinction prevents strategic reinvestment from being misread as operational distress. For boards evaluating financial stewardship, it's the difference between seeing a healthy organization and a struggling one.

Step 2: Conduct a Pro Forma Financial Analysis

Pro forma ("as-if") financial statements restate your income to show what results would have looked like without discretionary reinvestments—isolating core operational performance from strategic spending choices.

Step-by-Step Pro Forma Process

- Start with the actual Statement of Activities

- Identify and remove all discretionary expenses (as categorized in Step 1)

- Calculate the restated net income or surplus — this represents what the organization would have generated from core operations alone

What to Look For

Ideally, the pro forma result shows a financial surplus—confirming that core operations are self-sustaining. If the pro forma also shows a deficit, that signals a more serious structural imbalance requiring immediate attention.

Key Financial Ratios to Calculate

Run these ratios alongside the pro forma to build a complete picture:

Liquidity Ratio (Months of Cash on Hand):

- Formula: Cash and cash equivalents ÷ average monthly expenses

- Target: 3–6 months for standard-risk organizations

- Higher-risk organizations: 6–12 months

Operating Reserve Ratio:

- Formula: Unrestricted net assets (expendable) ÷ average monthly operating expenses

- Target: 3–6 months minimum; higher-risk organizations should target 9–12 months

Program Expense Ratio:

- Formula: Program expenses ÷ total expenses

- Benchmark: At least 65% according to BBB Wise Giving Alliance Standard 8

Debt-to-Assets Ratio:

- Formula: Total liabilities ÷ total assets

- Healthy: Under 0.5 (50%)

- Concerning: Over 1.0 indicates liabilities exceed assets

These benchmarks matter in practice. According to the NFF 2025 State of the Nonprofit Sector Survey, 52% of nonprofits maintain 3 months or less of cash on hand, and 36% ended 2024 with an operating deficit—confirming that falling short of these targets is common, not exceptional.

Using Pro Forma as a Planning Tool

Boards and executives can model future scenarios—such as "What if a major grant doesn't renew?"—to test resilience before problems arise. Running these models regularly means leadership can make informed adjustments while options remain open, rather than scrambling when cash runs low.

Step 3: Connect Financial Results to Mission Impact

Financial statements tell you what happened with money. They don't tell you what that money accomplished. This step asks leaders to translate numbers into narrative—explicitly linking how both non-discretionary and discretionary resources advanced the mission during the reporting period.

What a Strong Mission Impact Narrative Includes

A complete narrative covers three areas:

- Core program funding: Which ongoing services were sustained, how many constituents were served, and what outcomes were achieved

- Discretionary reinvestment: How surplus or flexible funds expanded capacity, launched strategic initiatives, or strengthened infrastructure

- Non-GAAP outputs: Quantifiable metrics—people served, programs delivered, outcomes measured—that bridge financial statements to mission results even when they fall outside standard accounting definitions

Why This Narrative Step Is Not Optional

Donors, board members, and funders cannot connect financial statements directly to mission outcomes on their own. The narrative bridges this gap, making it possible to demonstrate stewardship and justify reinvestment decisions.

Organizations like Charity Navigator evaluate not just financial ratios but also measurement systems, learning processes, and impact demonstration. Similarly, GuideStar's Platinum Seal of Transparency requires organizations to report organizational goals, strategies, and impact metrics beyond basic financials.

Research published in Humanities and Social Sciences Communications (2025) found that perceived financial transparency positively correlates with donor trust and perceived performance.

When the Narrative Breaks Down

External accountability standards like Charity Navigator and GuideStar reward organizations that can connect dollars to outcomes—but the real test is internal. If your team struggles to articulate a compelling mission narrative alongside the financial data, that's a signal that spending decisions may not be strategically aligned. It's worth bringing to the board as a governance conversation, not just a reporting problem.

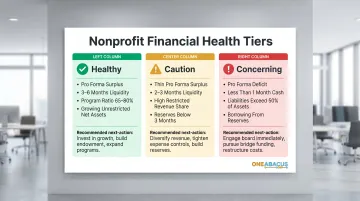

How to Interpret Your Nonprofit Financial Assessment

Healthy Signals

Your organization is in good shape when:

- Pro forma shows a surplus after removing discretionary expenses

- Liquidity covers 3–6 months of expenses

- Program expense ratio is 65–80%

- Restricted revenue does not dominate total income

- Unrestricted net assets are stable or growing year-over-year

Next steps: Reinvest surplus, communicate results to board and donors, plan strategically for growth, and consider building higher reserves if operating in a high-risk environment.

Caution Signals

Your organization needs closer attention when:

- Pro forma shows thin or near-zero surplus

- Liquidity covers fewer than 2–3 months

- Restricted revenue makes up the vast majority of total income

- Operating reserves are below 3 months

Review your revenue diversification strategy. According to GBQ Partners, financially healthy nonprofits generally keep any single revenue stream below 25–30% of total revenue. Also examine whether your expense structure reflects genuine strategic priorities — caution signals are manageable, but they require deliberate action before they become crises.

Concerning Signals

Your organization requires immediate board-level attention when:

- Pro forma shows a deficit even after removing discretionary expenses

- Cash on hand covers less than one month of expenses

- Liabilities exceed 50% of total assets

- The organization has been borrowing from reserves to cover operating expenses

Engage expert financial leadership without delay. A fractional CFO — like those at One Abacus Advisory — can assess the full picture, identify root causes, and build a realistic turnaround plan. Speed matters here: the longer concerning signals go unaddressed, the fewer options remain.

Common Mistakes That Distort Nonprofit Financial Assessments

Treating Restricted Funds as Available Surplus

Many nonprofit leaders see a positive net asset balance and assume financial health, without recognizing that restricted grant funds cannot be redirected. A large restricted surplus alongside thin unrestricted reserves is a liquidity risk, not a safety net.

Spending restricted funds outside donor designations forces the organization to replenish them from unrestricted reserves, directly straining operations.

Key practice: Always read restricted and unrestricted balances separately on the Statement of Financial Position.

Skipping the Pro Forma Step

Misreading net asset balances is only part of the problem. Without pro forma adjustments, raw financials routinely mislead — either making the bottom line look worse than it is, or hiding structural deficits behind one-time revenue. Pro forma analysis strips out discretionary reinvestments to reveal what's actually recurring.

Common adjustments include:

- Removing one-time capital expenditures or equipment purchases

- Backing out non-recurring grants that won't repeat next year

- Separating board-designated reserves from operating results

Performing Assessments Only Once Per Year

Annual reviews are insufficient for proactive financial management. Boards and executives who review financial gauges only at year-end miss the ability to course-correct mid-year.

Best practice recommendation:

- Monthly management review of key indicators

- Quarterly board reporting minimum

- Comprehensive annual assessment

The BBB Wise Giving Alliance Standard 3 requires a minimum of 3 evenly spaced board meetings per year with at least 50% average attendance—but more frequent review enables truly proactive decision-making.

Frequently Asked Questions

How much does a financial review cost for a small nonprofit?

Costs vary by review type: a basic compilation is the most affordable, a review is moderately priced, and a full audit is the most expensive. Cost depends on time spent, driven by organization size, budget complexity, federal grant requirements, and regional rates.

What financial statements does a nonprofit need to assess its financial performance?

The four core statements are the Statement of Financial Position, Statement of Activities, Statement of Cash Flows, and Statement of Functional Expenses. Each reveals different aspects: the first shows liquidity and solvency, the second shows operational sustainability, the third reveals cash management health, and the fourth demonstrates mission alignment and overhead efficiency.

How often should a nonprofit assess its financial performance?

Monthly management-level review of key financial indicators is recommended, with quarterly board reporting and a comprehensive annual assessment. More frequent review enables proactive decision-making — allowing organizations to identify trends and course-correct before vulnerabilities compound.

What is a good operating reserve ratio for a nonprofit?

Best practice is to hold 3–6 months of operating expenses in unrestricted reserves. Higher-risk organizations—those relying on periodic grants, fundraising events, or seasonal activities—should target 9–12 months. Less than one month of reserves represents a serious vulnerability that should trigger immediate board attention.

What is the difference between restricted and unrestricted funds in a nonprofit?

Restricted funds are designated by donors or grantors for specific purposes and cannot be freely redirected without violating donor intent. Unrestricted funds give the organization flexibility to cover operations, build reserves, or invest strategically in growth. Reading these categories separately is essential for accurate financial assessment.

When should a nonprofit consider hiring a fractional CFO?

A fractional CFO is most valuable during growth, leadership transition, or financial strain — when strategic financial guidance is needed without the overhead of a full-time hire. Given that financial leadership vacancies affect three-quarters of nonprofits, fractional support delivers senior-level expertise on a flexible, cost-aligned basis.

Nonprofit boards and executives who assess financial performance consistently are better positioned to demonstrate stewardship, plan strategically, and sustain mission impact. The three-step framework outlined here gives leaders the clarity to act on reliable data — whether the organization is on firm ground or navigating uncertainty.

If your organization needs support with financial assessment, reporting, or strategic financial leadership, One Abacus Advisory's fractional CFO services are built for nonprofits — offering senior-level guidance scaled to your budget and mission.