Fund accounting is the specialized system that makes this possible. Understanding it is foundational to sound nonprofit financial management, donor trust, and long-term organizational health—especially as funding pressures intensify.

Key Takeaways

- Fund accounting separates revenue into distinct "funds," each tracked independently based on donor restrictions or designated purpose

- FASB standards now require just two net asset categories: without donor restrictions and with donor restrictions

- Proper fund accounting supports FASB/GAAP compliance, Form 990 preparation, and grant reporting

- Common mistakes include over-fragmenting funds, commingling restricted and unrestricted money, and under-resourcing the accounting function

- Nonprofits in growth or transition benefit from fractional CFO support to build fund accounting systems that hold up as complexity increases

What Is Fund Accounting—and Why Nonprofits Operate Differently

Fund accounting is a specialized financial management system in which revenues and expenses are segregated into separate "funds," each functioning as its own self-contained ledger for tracking, reporting, and accountability purposes. This differs fundamentally from the single profit-and-loss view used by for-profit companies.

For-profit accounting optimizes for profitability and shareholder return. Nonprofit fund accounting prioritizes stewardship and accountability—demonstrating that every dollar was used in accordance with its intended purpose.

A fund is not a bank account. It's a pool of money classified by its source and purpose. Each fund carries its own revenue and expense report, excess or deficiency calculation, and balance sheet. This structure lets nonprofits show exactly how restricted dollars were spent, when they were spent, and whether spending aligned with donor intent.

Nonprofits are required to follow Generally Accepted Accounting Principles as governed by the Financial Accounting Standards Board (FASB), specifically ASC Topic 958, "Not-for-Profit Entities." Fund accounting is the standard method used to meet these requirements and prepare accurate financial statements.

In 2016, FASB issued ASU 2016-14, which modernized nonprofit financial reporting. It replaced the prior three-category model (unrestricted, temporarily restricted, permanently restricted) with a streamlined two-category model, effective for fiscal years beginning after December 15, 2017.

Who Uses Fund Accounting Beyond Nonprofits?

Fund accounting isn't exclusive to charitable organizations. It's also used by:

- State and local government agencies (governed by GASB standards)

- Public colleges and universities (GASB Statement No. 35)

- Private universities and healthcare systems (FASB ASC 958)

- Churches and religious organizations (FASB ASC 958)

- Foundations and endowed institutions

The common thread across all these entities: financial success is measured by stewardship, not profit. That distinction shapes every reporting decision a nonprofit finance team makes.

Understanding Net Asset Categories Under Current FASB Standards

Under current GAAP, nonprofits must classify all net assets into one of two categories established by FASB ASU 2016-14. Getting this classification right is the foundation of fund accounting — misclassification is one of the most common and costly errors nonprofits make.

Net Assets Without Donor Restrictions

Formerly called "unrestricted funds," these assets can be spent at the organization's discretion to advance its mission. Uses include:

- Operating expenses and overhead

- Staff salaries and benefits

- Program gaps not covered by restricted funding

- General organizational capacity building

Common sources: General donations, fundraising event revenue, membership dues, and earned income. Despite their flexibility, these funds still require disciplined tracking to support sound financial management and board-approved budget adherence.

Net Assets With Donor Restrictions

This category combines what were previously called "temporarily restricted" and "permanently restricted" funds. Assets in this category are subject to donor-imposed conditions that fall into three types:

- Time-based: Must be spent within a specific grant period

- Purpose-based: Designated for a specific program, project, or initiative

- Perpetual: Principal must remain intact indefinitely (endowments)

Example: A $50,000 grant restricted to youth programming. Once spent as intended and the restriction is met, the funds are "released from restriction" and flow into the unrestricted category (assuming no portion remains unspent).

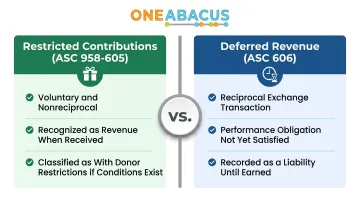

Many nonprofits also confuse restricted contributions with deferred revenue. FASB ASU 2018-08:%20CLARIFYING%20THE%20SCOPE%20AND%20ACCOUNTING%20GUIDANCE%20FOR%20CONTRIBUTIONS%20RECEIVED%20AND%20CONTRIBUTIONS%20MADE) draws a clear line between the two:

- Restricted contributions (ASC 958-605): Voluntary, nonreciprocal transfers recognized as revenue when received. Classified as "with donor restrictions" if conditions exist.

- Deferred revenue (ASC 606): Funds received for reciprocal exchange transactions where performance obligations have not yet been satisfied (e.g., prepaid event tickets). Recorded as a liability until earned.

Endowments and Permanently Restricted Funds

Permanently restricted funds typically take the form of endowments: large contributions where the principal must remain intact in perpetuity, and only the investment income generated may be spent, as directed by the donor agreement.

Real-world context: Universities use endowments for scholarships, hospitals for research, arts organizations for programming continuity. Harvard University's Faculty of Arts and Sciences, for example, manages multiple endowment types:

- Permanent endowments: Principal cannot be spent; only investment income is available

- Quasi-endowments: Principal may be spent, but the organization chooses to invest it for long-term growth

- Restricted vs. unrestricted endowments: Designated for specific purposes vs. general organizational support

Most endowment gifts are pooled and invested together, with each fund receiving "units" (shares). Annual distributions are typically calculated based on the fund's unit balance multiplied by a board-approved distribution rate.

Fund Accounting in Action: Practical Applications

Fund accounting isn't just an internal tracking exercise—it shapes the structure of the organization's core financial documents and operational decision-making.

Chart of Accounts Design

A nonprofit's chart of accounts must reflect fund accounting by including:

- Separate net asset categories for each fund type

- Sub-categories within revenue for different restricted sources (federal grants vs. private foundation grants vs. corporate sponsorships)

- Unique identifiers—fund codes that can include donor, grant, project, location, and program dimensions

This structure allows staff to run queries and generate reports across any of those dimensions: "How much federal grant funding remains for our literacy program?" or "What were total program expenses for our youth services division in Q3?"

Required Financial Statements

FASB ASC 958 requires four core financial statements:

Statement of Financial Position: Assets, liabilities, and net assets organized by restriction category (with and without donor restrictions)

Statement of Activities: Revenues, expenses, and changes in net assets broken out by restriction class

Statement of Cash Flows: Cash inflows and outflows using either the direct or indirect method

Functional Expense Report: Expenses classified by both natural category (salaries, rent, supplies) and function (program services, management and general, fundraising). ASU 2016-14 extended this requirement to all nonprofits—not just voluntary health and welfare organizations.

Liquidity Disclosure: Quantitative disclosure of financial assets available for general expenditures within one year of the balance sheet date, plus a qualitative description of how the organization manages liquidity risk

Grant and Donor Reporting

Those financial statements are the foundation for the reporting funders actually ask for. Fund accounting makes it possible to produce accurate grant reports on demand—showing a funder exactly what was spent, when, and how it aligned with the grant agreement. That level of precision matters for compliance, but it's just as important for donor stewardship and renewal.

Budget and Operational Planning

Fund accounting directly informs annual budgeting. The process typically follows this sequence:

- Identify all restricted funds and their designated purposes

- Allocate restricted funds first to their specified programs

- Use unrestricted funds to fill remaining program and overhead gaps

- Avoid "double-spending" restricted dollars already allocated

This approach gives leadership a true picture of organizational liquidity and prevents the common mistake of assuming all cash on hand is available for discretionary use.

Best Practices and Common Mistakes in Nonprofit Fund Accounting

Best Practices to Follow

Avoid creating a separate fund for every grant or program activity. Sub-codes and unique identifiers within existing fund categories give you the granularity you need without fragmenting the chart of accounts. A simpler fund structure is easier to manage, audit, and explain to board members.

Rather than opening a separate bank account for every fund, maintain a single pooled cash account with sub-allocations tracked in your accounting system. This approach:

- Simplifies bank reconciliation

- Reduces administrative overhead

- Preserves fund-level reporting integrity

- Improves cash flow visibility

Program managers need fund-level visibility, not just senior finance staff. Regularly reconcile fund balances and share fund-level reports with the people running programs — when they understand how much restricted funding remains, they manage resources more carefully and flag issues earlier.

Common Mistakes to Avoid

KLR's audit findings research identifies mismanaging restricted revenue as the #1 costly mistake nonprofits make. Commingling restricted and unrestricted funds — whether by accident or cash flow pressure — violates donor trust, creates audit risk, and can damage future funding relationships. Treat fund boundaries as non-negotiable, even in lean periods.

Many nonprofits try to manage fund accounting with general-purpose software — or with staff who lack nonprofit-specific experience. QuickBooks Online has real limitations in this context:

- Uses a "Classes" workaround to simulate fund tracking (not true self-balancing fund accounting)

- Cannot properly generate fund-level balance sheets

- No native Statement of Functional Expenses

- Managing more than 20 funds becomes unwieldy and error-prone

- Requires external spreadsheets for grant budgets and fund balance tracking

These workarounds create compliance risk and reporting gaps that become harder and more expensive to untangle as the organization grows.

Other frequent errors include:

- Weak internal controls and documentation

- Misclassifying revenue and expenses

- Failing to track and honor donor-imposed conditions

- Improper worker classification (employees vs. contractors)

When Your Nonprofit Needs Expert Fund Accounting Support

Nonprofits typically outgrow their current financial infrastructure at predictable inflection points:

- Rapid growth in program revenue or service delivery

- New grant sources with complex reporting requirements

- Leadership transitions (CFO, finance director, or controller departures)

- Audit preparation and compliance pressure

- Board demands for better financial visibility and strategic insight

Each of these moments strains existing systems and staff — and often signals that outside expertise is the more practical path forward. A Citrin Cooperman analysis confirms that fractional CFO engagements deliver the most impact precisely at these inflection points. A fractional CFO can establish or overhaul the fund accounting system without the cost of a full-time hire, covering:

- Budgeting, forecasting, and financial reporting

- Compliance with nonprofit accounting standards

- Audit preparation and grant reporting support

- Staff financial literacy training

- Technology system optimization

One Abacus Advisory provides fractional CFO and senior finance team support specifically for nonprofits navigating these transitions. With over 25 years of finance and accounting experience and a dedicated focus on nonprofit financial leadership, the firm helps organizations build fund accounting systems that serve both compliance requirements and strategic decision-making.

Case in point: Philadelphia Zoo

When the Philadelphia Zoo faced a simultaneous CFO and Controller departure, One Abacus stepped in to optimize their NetSuite environment, improve month-end close processes, and strengthen board reporting. The outcome was greater confidence in financial results and measurably stronger financial literacy across the executive team. The firm's client roster also includes the San Diego Food Bank and Laguna Playhouse.

Frequently Asked Questions

What is fund accounting in nonprofits?

Fund accounting is a financial management system that separates revenue and expenses into distinct funds based on donor restrictions or designated purpose. Unlike for-profit accounting, which optimizes for profitability, fund accounting prioritizes accountability and stewardship, ensuring resources are used as donors intended.

What is a fund in nonprofit accounting?

A fund is not a bank account but a pool of money classified by its source and intended use. Each fund carries its own revenue and expense tracking, balance sheet, and reporting requirements. Funds allow nonprofits to demonstrate compliance with donor restrictions and grant agreements.

How do nonprofits use fund accounting?

Nonprofits use fund accounting to manage financial obligations across several areas:

- Track restricted vs. unrestricted revenue

- Prepare FASB-compliant financial statements (Statement of Financial Position, Statement of Activities, functional expense reporting)

- Manage grant compliance and inform annual budgets

- Report transparently to donors and boards

What are the golden rules of fund accounting?

The core rules every nonprofit should follow:

- Use each fund only for its designated purpose

- Never commingle restricted and unrestricted dollars

- Maintain a clear audit trail for every fund

- Report on each fund separately and transparently to stakeholders

- Ensure the chart of accounts supports fund-level visibility without unnecessary fragmentation

What is the best accounting system for a nonprofit organization?

The best system is purpose-built for nonprofits and supports true fund accounting with restricted fund tracking, FASB-compliant reporting, grant management, and functional expense allocation. Platforms like Sage Intacct, Blackbaud Financial Edge NXT, and Aplos are all designed with nonprofit needs in mind.

Are non-profit financial records public?

Yes. Most 501(c)(3) organizations are required to file Form 990 with the IRS, available via the IRS Tax Exempt Organization Search, GuideStar/Candid, and ProPublica Nonprofit Explorer. Form 990 discloses revenue, expenses, net assets, executive compensation, and program accomplishments. Many nonprofits also voluntarily publish audited financial statements to build donor trust.