Introduction

Most nonprofits don't fail because they lack mission clarity or staff commitment—they struggle because they're missing a deliberate funding strategy. There's a critical difference between reacting to every funding opportunity that crosses your desk (a gala here, a foundation grant there, a government contract when it appears) and building a sustainable, mission-aligned revenue model.

The trap is familiar: you pursue diverse revenue streams without a coherent framework, hoping that more sources mean more security. Instead, it leaves your organization financially fragile. When a major funder shifts priorities or your signature fundraising event underperforms, you're scrambling.

Research from Bridgespan Group reveals that 90% of large nonprofits grew by concentrating on one or two revenue categories and building deep capability there, rather than spreading resources thin across many.

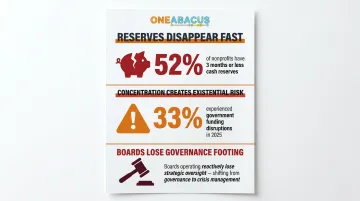

The financial consequences of reactive fundraising show up on the balance sheet. The Nonprofit Finance Fund's 2025 survey found that **52% of nonprofits have three months or less of cash on hand**, with 18% having just one month or less. This isn't just poor planning—it's the predictable outcome of chasing funding without a strategic foundation.

This guide walks you through how to audit your current funding model, identify the right revenue categories for your mission and capabilities, build the financial infrastructure to execute, and measure progress over time.

Whether you're an executive director, development leader, finance officer, or board member, you'll finish with a practical framework — not a wishlist — for building financial sustainability that holds up under pressure.

Key Takeaways

- A funding strategy is a deliberate framework for which revenue sources to pursue, build systems around, and sustain over time — not a list of tactics

- Start with an honest audit: analyze your actual revenue mix over five years and what it cost you to raise that money

- Most successful nonprofits focus on one major and one secondary revenue category, building systems and relationships around those

- Financial infrastructure — reporting, dashboards, compliance tracking — determines whether your strategy holds up in practice, not just on paper

- Expect 18-24 months before the revenue mix stabilizes; track leading indicators (donor retention, grant renewal rates) from month one

What Is a Nonprofit Funding Strategy (and Why It Matters)

A nonprofit funding strategy is a deliberate plan for which revenue categories align with your organization's mission, program model, and internal capabilities—and a roadmap for building the systems needed to pursue those sources sustainably. That's fundamentally different from fundraising tactics—the individual campaigns, appeals, grant proposals, and events you run. Strategy determines which of those activities are actually worth running.

Bridgespan Group defines a funding model as "a methodical and institutionalized approach to building a reliable revenue base that will support an organization's core programs and services." The Nonprofit Finance Fund describes it as "how an organization makes and spends money in service of its mission," covering service delivery, reliable revenue, and full-cost accounting including infrastructure.

Why the Absence of Strategy Creates Fragility

Without a defined funding model, organizations default to opportunism—pursuing whatever grant is available, launching events without knowing if they generate a positive ROI, or depending too heavily on a single donor relationship. This creates three specific vulnerabilities:

- Reserves disappear fast. Organizations with three months or less of operating cash are one unexpected crisis away from program cuts or layoffs, per NFF survey data.

- Concentration creates existential risk. The Urban Institute's 2025 research found 33% of US nonprofits experienced government funding disruptions in early 2025. Disrupted organizations averaged 42% government dependence (vs. 28% sector-wide) and were twice as likely to cut staff.

- Boards lose governance footing. Without revenue tracking by category, restriction management, and ROI analysis, board members can't make informed decisions about risk or sustainability.

Who This Guide Is For

This framework is designed for nonprofit executive directors, development leaders, finance officers, and board members at organizations of any size who are building or revisiting their approach to long-term financial sustainability. Whether you're operating on a $500,000 budget or $50 million, the principles remain consistent.

Step 1: Audit Your Current Funding Model

Analyze Your Revenue Mix

Looking at revenue data across five years—rather than a single annual snapshot—reveals trends that would otherwise remain invisible. You might discover that individual giving is declining as a share of total revenue even as dollars grow, or that a single funder relationship now accounts for an increasingly concentrated percentage of income.

How to pull and disaggregate the data:

- Export revenue data from your accounting system for the past five fiscal years

- Categorize every revenue line into core funding categories (detailed below)

- Calculate each category as both dollar amount and percentage of total revenue

- Map changes year-over-year to identify growth, decline, or volatility patterns

- Calculate fundraising costs by category to determine true net return

Core revenue categories to map:

- Government contracts and grants: Federal, state, and local funding tied to service delivery or constituent support

- Service/program fees (earned income): Revenue from beneficiaries, event tickets, consulting services, or products

- Corporate giving: Sponsorships, matching gifts, and corporate foundation grants

- Private and community foundations: Institutional philanthropy with formal application processes

- High-net-worth individual donors: Major gifts typically $10,000+ per donor annually

- Small individual gifts: Contributions under $10,000, including online giving and direct mail

- Investment or endowment income: Returns from invested reserves or permanent endowment funds

Each category carries a different risk profile and sustainability characteristic. Government grants may offer large dollar amounts but come with compliance burdens and political risk. Individual giving requires intensive relationship management but offers greater flexibility in how funds are deployed.

Understand Funder Motivations

Knowing what drives each funder type helps you identify where realistic growth exists — and where pursuing new revenue would require more effort than return.

- Government agencies: Motivated by policy priorities and service gaps. Strong fit if your program serves a defined population (veterans, seniors, low-income communities)

- High-net-worth donors and philanthropists: Drawn to personal mission connection, innovation, and legacy — often willing to fund early-stage work others won't

- Corporations: Seek visibility and community goodwill; fund causes aligned with brand identity or employee engagement goals

- Private foundations: Operate within defined program areas and geographic priorities; favor organizations that demonstrate capacity for scale or systems change

How to gather funder motivation data:

- Conduct outreach calls with existing donors and foundation program officers

- Ask how your organization fits within their broader portfolio

- Inquire whether their funding interests are shifting in coming years

- Review their annual reports and IRS Form 990-PF filings (available via ProPublica's Nonprofit Explorer)

These conversations often surface shifts in funder priorities before they show up in your revenue data — giving you time to adjust.

Assess Your Fundraising Capabilities

An honest internal capabilities audit answers:

- Does your executive director drive most fundraising, or is there a distributed team?

- Do you have a strong grants team with government contracting experience?

- Does your annual gala generate meaningful net revenue after costs, or is it breaking even?

- Is there a major gifts officer, or does that function not exist?

- How sophisticated is your donor database and CRM infrastructure?

- Does your board actively open doors and make introductions?

This assessment reveals which revenue categories you can realistically pursue versus which would require significant new investment in staff, systems, or board engagement. Bloomerang's research found that 58.87% of nonprofits lack a major gift strategy, with 75.32% citing lack of investment in manpower, expertise, or strategy as the reason.

Including a revenue category in your strategy without a plan to build the capability behind it sets up your team for failure. Either invest in the capacity or don't count on the revenue.

Step 2: Identify Your Optimal Revenue Mix

The Case for Focus Over Diversification

This is where conventional wisdom gets challenged. Most boards push for diversification, reasoning that more revenue streams reduce risk. But Bridgespan's research tells a different story.

Bridgespan studied nearly 300 US-based nonprofits that reached $50 million in annual revenue within 30 years of founding—and found that 90% grew by concentrating on a single primary funding source. On average, that dominant source accounted for just over 90% of total funding. Large organizations often maintained a secondary revenue source (often philanthropy) accounting for 20-30% of total funding.

The "major and minor" category framework:

- Primary revenue category: Build your core organizational capability here—staff expertise, funder relationships, and specialized systems

- Secondary revenue category: Plays a meaningful but supporting role, providing flexibility and risk mitigation without diluting your primary focus

This doesn't mean you'll have zero income from other categories. It means deliberately choosing where to build institutional capability rather than maintaining shallow competence across many areas.

When to concentrate vs. when to diversify:

- Concentrate when you're building a new organization, have limited staff capacity, or have identified a high-potential revenue category with strong mission alignment

- Diversify when a single funder or category exceeds 40-50% of total revenue (per Blackbaud's financial resilience framework), government funding is at political risk, or you've fully maximized one category's potential

- Consider organizational stage: Early-stage nonprofits benefit from focus; mature organizations with robust infrastructure can manage more complexity

Develop and Test Your Revenue Hypothesis

Form your hypothesis by aligning three factors:

Natural match between program model and funder motivation: If you deliver direct services to low-income families, government contracts and community foundations are natural matches. Advocacy or systems change work fits better with philanthropists and private foundations.

Existing internal capabilities: Where do you already have expertise, relationships, or systems in place that can be put to use?

Market conditions and growth potential: Is this funding category expanding or contracting? Are new funders entering the space?

How to validate your hypothesis through peer benchmarking:

Use ProPublica's Nonprofit Explorer or Candid to review Form 990 data for similar organizations. Look specifically at:

- Part VIII, Revenue section: See their income sources and proportions

- Schedule A: Public support test details

- Part IX, Expenses: Understand their cost structure

- Five-year trends: Are they growing a particular category?

Follow the data with direct conversations. Ask peer organizations about timeline to results, upfront investment required, and lessons learned. The goal isn't to copy what they did—it's to test feasibility before committing resources.

Factor in external environment shifts:

- New legislation affecting nonprofit funding priorities (such as changes to government social service budgets)

- Economic conditions affecting individual giving capacity

- Foundation sector trends toward specific issue areas

- Corporate giving patterns tied to business cycles

The NFF's 2025 survey found that 84% of nonprofits with government funding expect cuts—an external factor that should directly influence whether government contracts remain a primary revenue hypothesis or need to be de-emphasized.

Revisit your revenue hypothesis annually as part of strategic planning. What works in year two may not hold in year five—building in that review point is how you stay ahead of shifts rather than react to them.

Step 3: Build the Financial Infrastructure to Support Your Strategy

Financial Reporting and Revenue Tracking

Financial infrastructure is the missing link between a strategy document and actual execution. Without systems that track revenue by category, distinguish restricted from unrestricted funds, and project cash flow against fundraising timelines, even a well-designed strategy stalls.

The good news: the right reporting setup removes the guesswork.

Essential reports and dashboards:

- Revenue by category dashboard: Monthly tracking of actual vs. budget by each revenue category with year-over-year comparison

- Restricted vs. unrestricted fund tracking: Clear accounting of donor-imposed restrictions and how they're being satisfied

- Cash flow forecast: Rolling 12-month projection showing expected revenue timing and expense obligations

- Fundraising ROI analysis: Cost to raise a dollar by category (staff time, direct costs, overhead allocation)

- Grant deliverables tracker: Status of all grant-funded obligations and reporting deadlines

- Donor retention metrics: Retention rate, attrition rate, and average gift trends by donor segment

Blackbaud's 2026 framework recommends boards monitor six core financial health metrics monthly: revenue diversity, burn rate, operating margin (target 10-15%), expense ratios (65-75% to programs), months of cash on hand (target 3-6 months), and asset composition.

Selecting the right accounting system:

Your accounting platform must be configured to track revenue by the categories and restrictions relevant to your funding strategy, not just by general ledger line.

| Platform | Best For | Key Nonprofit Features |

|---|---|---|

| NetSuite for Nonprofits | Mid-to-large organizations with complex grant portfolios | GAAP/FASB-compliant fund accounting, donor and grant restriction reporting, customizable segmentation, integrated CRM |

| QuickBooks Nonprofit | Smaller organizations with simpler needs | Fund accounting, donation and grant tracking, class and location tracking for restricted funds |

One Abacus Advisory has done this kind of configuration work for organizations like the Philadelphia Zoo, restructuring NetSuite to support grant restriction tracking, board-level reporting, and multi-segment financial analysis — not just standard bookkeeping.

Compliance and Restricted Fund Management

Different revenue categories carry significantly different compliance requirements:

Government Grants

- Contract deliverable tracking with documentation

- Separate audit trails for federal funds (Single Audit required at $750,000+ in federal funding)

- Timely drawdown and expenditure reporting

- Compliance with Federal Acquisition Regulation (FAR) or Uniform Guidance (2 CFR 200)

Foundation Grants

- Restricted use provisions that must be documented and reported

- Interim and final reporting requirements with specific formats and deadlines

- Site visit preparation and funder relationship management

Earned Income

- Tax implications under Unrelated Business Income Tax (UBIT) rules

- IRS Publication 598 governs when earned income is taxable (regularly carried on, not substantially related to exempt purpose)

Public Charity Status

- The IRS public support test under IRC Section 509(a)(1) requires at least one-third (33⅓%) of support from public sources

- Support from any single donor counts toward "public support" only up to 2% of total support

- Measured over a five-year rolling period on Schedule A of Form 990

- Failure for two consecutive years triggers reclassification as a private foundation

Each time you add a new revenue category, you're also adding compliance obligations. Building the infrastructure before you need it is far easier than retrofitting it after a missed deadline or audit finding.

When to Bring in Financial Leadership Support

Many nonprofits in growth or transition don't have the internal capacity to build and maintain the financial infrastructure a funding strategy requires.

Warning signs you need external financial leadership:

- Revenue not clearly tracked by category or restriction

- Difficulty forecasting cash flow beyond 30-60 days

- Board lacking confidence in financial reports

- No clear sense of return on fundraising investment

- Grant reporting deadlines frequently missed

- Audit findings related to internal controls or fund accounting

In these situations, fractional CFO services provide the financial leadership needed to build reporting systems, manage compliance across funding categories, and guide strategic financial decisions—without the cost and commitment of a full-time hire.

One Abacus Advisory works with nonprofits in exactly these situations — providing fractional CFO support during audits, leadership transitions, and funding growth phases. The engagement model is flexible by design, giving organizations access to senior-level financial expertise at a cost that fits their budget and stage.

Step 4: Build Your Roadmap and Measure What Matters

Consolidate your work into a written funding strategy roadmap containing:

1. Current-state summary: Your existing revenue mix with five-year trends, fundraising costs by category, and identified vulnerabilities

2. Target revenue mix and rationale: Your chosen primary and secondary revenue categories with specific percentage targets and the strategic reasoning behind each choice

3. Capability development plan: What needs to be hired (staff roles and timeline), built (systems and infrastructure), or invested in (technology, training, board development) to execute the strategy

4. Timeline with milestones: 18-24 month implementation roadmap with quarterly checkpoints and decision points

5. Defined KPIs for each revenue category: Both revenue targets and leading indicators (detailed below)

This document gives leadership, board members, and development staff a shared reference point when priorities compete or resources run tight.

Set Leading Indicators, Not Just Revenue Targets

Bridgespan's guidance is clear: it can take 18-24 months—or longer—for a fundraising strategy to pay off. If you're investing in new capabilities (hiring staff, purchasing technology), it could take several years for added revenue to cover those initial investments.

Early indicators matter more than early dollars:

Leading indicators to track:

- Number of qualified funder conversations held

- Grant proposals submitted (and to new vs. existing funders)

- Donor discovery meetings completed

- Board members actively engaged in cultivation activities

- New contracts in negotiation pipeline

- Prospect identification and research completed

- Donor retention rate by segment

- Average gift size trends

The AFP Fundraising Effectiveness Project reported that average donor retention stood at just 42.9% in 2024, marking the fifth consecutive year of decline. If your strategy depends on individual giving growth, donor retention is a leading indicator that predicts future revenue trajectory.

Establish Regular Review Cycles

Quarterly financial reviews should include:

- Revenue actual vs. budget by category

- Cash flow and reserve status

- Fundraising ROI analysis

- Grant pipeline and deliverable status

- Leading indicator dashboard review

Biannual strategy check-ins should assess:

- Whether capability investments are paying off

- If external environment shifts require hypothesis adjustments

- Whether concentration risk thresholds are being breached

- Board confidence in financial oversight and strategic direction

These reviews exist precisely because the funding landscape changes. Giving USA 2025 reported total US charitable giving reached $592.50 billion in 2024, up 6.3%. Yet individual giving patterns, foundation priorities, and government funding landscapes shift constantly. Adjusting your approach in response to new data is disciplined strategy, not a sign that the original plan was wrong.

Frequently Asked Questions

How do nonprofits get funded and what funding strategies can they use?

Nonprofits are funded through six main categories: government grants and contracts, earned income from services or products, private foundations, high-net-worth individual donors, small individual gifts, and corporate partnerships. The most sustainable funding strategies focus on 1-2 well-matched categories built around the organization's mission and internal capabilities, rather than pursuing every source simultaneously.

What is the 80/20 rule for nonprofit fundraising?

The 80/20 rule suggests that roughly 80% of fundraising revenue comes from just 20% of donors. Recent data suggests the concentration is even more extreme — Bloomerang found that 88% of dollars raised comes from just 12% of donors, which is why major gift cultivation and stewarding top funders is disproportionately important.

What is the 33% rule for nonprofits?

The 33% rule refers to the IRS public support test for 501(c)(3) public charities, which requires at least one-third of support come from the general public or government sources. Broad donor base development isn't just a fundraising goal — it's a compliance requirement tied directly to maintaining public charity status.

What is the 5% rule for nonprofits?

The 5% rule applies to private foundations, which must distribute at least 5% of their assets annually for charitable purposes under IRC Section 4942. For nonprofits seeking foundation grants, this rule directly affects grant availability, timing, and how program officers allocate their giving each year.

What should be included in a nonprofit strategic plan?

A nonprofit strategic plan should include the organization's mission and programmatic priorities, a funding strategy (target revenue mix and capability roadmap), operational goals, financial sustainability targets, and key performance indicators. The funding strategy should be developed in direct alignment with—not separately from—the overall strategic plan to ensure financial resources support mission delivery.

What are the 7 pillars of fundraising?

While definitions vary across the sector, core fundraising pillars commonly include prospect identification, cultivation, solicitation, stewardship, case for support, leadership engagement, and systems and infrastructure. A sound funding strategy provides the framework that makes each of these pillars work together toward sustainable revenue growth rather than functioning as disconnected activities.

The nonprofits that weather funding disruptions and scale impact are those that match opportunities to their mission and capabilities, then build the systems to pursue them consistently. The nonprofits that weather funding disruptions, scale impact, and maintain board confidence are those that have moved from reactive fundraising to deliberate, infrastructure-backed funding strategies.

If your organization is navigating this transition—whether you're revisiting an outdated funding model, preparing for growth, or working to strengthen financial oversight—expert financial leadership can accelerate the process. One Abacus Advisory specializes in helping nonprofits build the financial infrastructure, reporting systems, and strategic clarity needed to execute funding strategies effectively. Schedule a consultation to discuss how fractional CFO services can support your organization's path to sustainable funding.