Introduction

Nonprofit finances in 2026 are under pressure from multiple directions at once. 33% of organizations experienced government funding disruptions in early 2025—including funding loss, freezes, and stop-work orders. Meanwhile, the number of individual donors declined 3.6% in 2025, continuing a downward trend that stretches back to 2021. Layer in persistent staff turnover—particularly in finance roles—and financial distress becomes a real operational risk for organizations of all sizes, not just the most vulnerable ones.

What separates nonprofits that recover from those that don't? The three composite case studies below are drawn from real patterns in nonprofit financial turnarounds, each showing how targeted strategies reversed severe decline.

Whether the crisis stems from leadership departures, revenue concentration, or a failed technology transition, the organizations that stabilized shared one trait: they acted before the window closed.

Key Takeaways

- Three root causes drive most nonprofit financial crises: leadership gaps, single-source funding dependence, and failed technology transitions

- Early action on warning signs prevents audit failures and cash insolvency

- Stabilization comes first — close the books, reconcile accounts — then address structural fixes like revenue diversification and tighter controls

- Fractional CFO support delivers senior financial leadership during turnarounds at a fraction of full-time hire costs

Warning Signs a Nonprofit Needs a Financial Turnaround

Understanding the Difference Between Dips and Crises

A temporary cash flow dip is normal. A structural financial crisis is not. The distinction lies in whether the organization can produce reliable financial information and maintain basic compliance. Warning indicators that signal crisis rather than temporary strain include:

- Consistently late financial closes beyond 10 business days

- Mounting accounts payable with aging balances extending beyond normal payment cycles

- Inability to produce a reliable trial balance or reconcile to bank statements

- Failure to meet audit deadlines, risking federal compliance violations

When nonprofits expending $750,000 or more in federal awards miss the 9-month single audit filing deadline, consequences escalate: drawdown restrictions, fund withholding, suspension, or grant termination.

Operational Red Flags That Precede Collapse

Financial statements tell only part of the story. Watch for these operational warning signs:

Leadership instability in finance roles: 72% of nonprofits struggle with finance function turnover. When both a controller and CFO exit within months of each other, finance knowledge doesn't transfer automatically—it walks out the door with departing staff.

Over-dependence on one or two grants: Over 35,000 nonprofits rely on government grants for more than 50% of total revenue, and for human services organizations that figure reaches 40%. A single policy shift or non-renewal creates immediate existential risk.

Consistent budget-to-actual variance: When revenue repeatedly underperforms projections but board meetings proceed without corrective action, the organization is drifting toward crisis. Unchallenged variance reports are a warning sign, not routine business.

The Reserve Crisis Facing the Sector

52% of nonprofits report three months or less of cash on hand, with 18% reporting one month or less. Even more concerning: 36% ended 2024 with an operating deficit—the highest in ten years of survey data.

Thin reserves leave no room for error. A delayed government reimbursement, a sudden program cost increase, or an unplanned leadership departure can each tip an already-strained organization into crisis. Boards should establish a minimum three-month reserve policy as a standing governance requirement, even when building toward that target takes several years.

Case Study 1: Recovering After the Loss of Key Financial Leadership

Background

A mid-size human services nonprofit with a $5.2 million annual budget lost both its controller and CFO within six months. The controller left first, citing burnout and insufficient support. The CFO departed three months later for a higher-paying role at a larger organization. Within weeks, the finance function deteriorated: books went unclosed for over a year, bank reconciliations piled up undone, and grant expenditure reports to federal funders couldn't be completed accurately.

The organization's single audit deadline loomed. Without an unqualified opinion, the nonprofit faced the potential loss of government funding representing 62% of its budget. The remaining finance staff—a part-time bookkeeper and a program accountant unfamiliar with fund accounting—couldn't reconstruct the records alone.

Challenge

The crisis escalated fast. Without a reliable trial balance, the organization faced three simultaneous gaps:

- No board financial statements could be produced

- True cash position was unknown

- Restricted grant compliance couldn't be verified

No documented accounting procedures existed. Everything had lived in the departed leaders' heads.

The audit firm issued a warning: without closed books and reconciled accounts, they couldn't begin fieldwork. If the audit deadline passed without submission, federal funders would freeze payments. The executive director, skilled in program delivery but not financial management, faced the real possibility of organizational collapse.

Strategy Applied

The board engaged One Abacus Advisory to serve as interim CFO and audit liaison simultaneously. The recovery approach unfolded in three phases:

Phase 1: Account-by-account reconstruction (Weeks 1-8)

- Created action plans for every balance sheet and income statement account with hard deadlines

- Reconciled 14 months of bank statements, identifying and resolving discrepancies

- Rebuilt the chart of accounts to properly segregate restricted and unrestricted funds

- Documented all grant compliance requirements and expenditure tracking procedures

Phase 2: Audit preparation and external reporting (Weeks 9-14)

- Prepared accurate financial statements for the audit period

- Compiled supporting documentation for all material transactions

- Served as primary liaison with auditors, responding to information requests

- Drafted management representation letters and corrective action plans for any findings

Phase 3: Control establishment and team building (Weeks 15-20)

- Documented month-end close procedures with specific task assignments and timelines

- Implemented segregation of duties controls appropriate to team size

- Established a financial reporting calendar aligned with board meeting schedules

- Supported recruitment of permanent controller and onboarding with clear role definitions

Outcome

The organization closed its books within the recovery window. The audit was completed, resulting in an unqualified opinion with no material weaknesses. Government funding was preserved. The nonprofit also came out of the process with documented procedures, clear role definitions, and a permanent accounting team equipped to maintain financial health going forward.

Monthly financial statements reached the board on time. Cash flow visibility improved. Program leaders could finally see reliable reports showing which grants had available balances and which required attention.

Key Takeaway

When financial leadership exits suddenly, replacing personnel isn't enough. The priority sequence matters: first, document what exists and stabilize compliance; second, rebuild controls and procedures; third, add capacity for growth. Organizations that skip directly to hiring often repeat the cycle—because undocumented systems break down again when the next person leaves.

Case Study 2: Reversing a Revenue Concentration and Cash Flow Crisis

Background

A regional food security organization with a $6.8 million annual budget had relied on two large federal nutrition program grants for 68% of its revenue. These grants had renewed predictably for over a decade. In early 2025, a federal policy shift reduced one grant by 40% and eliminated the other entirely. The organization faced a $780,000 budget shortfall within a single fiscal year.

The finance team, experienced in government grant compliance, had never built a diversified fundraising strategy. Individual donor revenue represented less than 12% of the budget. The board, accustomed to stable government funding, received the news with alarm but lacked the financial literacy to guide corrective action.

Challenge

The immediate crisis was cash flow. Payroll risk emerged within 90 days. Program cuts moved from theoretical discussion to active planning. The executive director considered laying off 30% of staff, which would have crippled service delivery in communities already experiencing food insecurity.

Beyond the immediate cash crunch, the organization had no infrastructure for individual giving campaigns, no corporate partnership strategy, and no fee-for-service program models. Staff expertise centered on government compliance, not fundraising.

The board needed real-time financial visibility to make decisions but received only quarterly reports that were already outdated when presented.

Strategy Applied

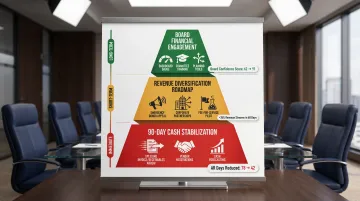

One Abacus Advisory implemented a three-tier turnaround approach:

Tier 1: 90-day cash stabilization

- Accelerated collection of outstanding government receivables, reducing days outstanding from 78 to 42

- Negotiated extended payment terms with key vendors to preserve cash

- Deferred non-essential capital spending and training budgets

- Implemented weekly cash flow forecasting with scenario modeling for different funding outcomes

Tier 2: Revenue diversification roadmap

- Launched an emergency appeal to individual donors, raising $127,000 in 60 days

- Developed corporate partnership proposals targeting food industry companies with aligned priorities

- Piloted a fee-for-service nutrition education program for corporate wellness programs

- Built a donor database and implemented basic CRM functionality for relationship management

Tier 3: Board financial engagement

- Created monthly financial dashboards showing cash position, revenue pipeline, and program profitability

- Trained board finance committee members to interpret variance reports and ask informed questions

- Established monthly financial review sessions replacing quarterly presentations

- Implemented scenario planning tools allowing board members to model different funding mix outcomes

Outcome

The cash position stabilized within 90 days, eliminating immediate layoff risk. New revenue streams generated $340,000 within the first 12 months. That fell short of fully replacing lost government funding, but it bridged the gap while longer-term fundraising infrastructure matured.

The board shift was equally significant. Members moved from passive recipients of quarterly reports to active participants in financial oversight — asking informed questions about funding mix, reserve targets, and resource allocation. That kind of engaged governance is itself a form of organizational resilience.

Key Takeaway

No nonprofit should allow a single revenue source to represent more than 40-50% of total income. When over-concentration exists, financial turnaround requires both immediate cash management and a longer-term structural rethink of the funding model. Revenue diversification realistically takes 18-24 months to generate meaningful income. Organizations that begin building that infrastructure before a crisis hits — rather than during one — preserve the time and stability needed to do it right. One Abacus Advisory's fractional CFO model is specifically designed to support that kind of proactive transition, providing the financial oversight and revenue strategy nonprofits need without the cost of a full-time hire.

Case Study 3: Rebuilding Financial Operations After a Technology Transition

Background

A mid-size performing arts nonprofit with a $4.3 million budget migrated from QuickBooks to NetSuite, seeking better grant tracking and reporting capabilities. The implementation was compressed into four months to meet an audit deadline. Staff received minimal training — two half-day sessions before go-live. Consultants configured the system based on generic nonprofit templates without customizing for the organization's specific fund accounting requirements.

Eighteen months after go-live, the consequences were hard to ignore:

- Grant expenditure tracking was broken; program managers couldn't determine available balances

- Accounts receivable aging climbed from 45 days to 112 days due to misconfigured billing workflows

- The finance team reverted to shadow spreadsheets, creating compliance risk and version control chaos

Challenge

The damage spread quickly across the organization. Grant reports to funders contained errors that required corrections, damaging credibility with major supporters. Board financial statements showed inconsistent numbers month-to-month as staff manually patched system mistakes. External auditors flagged internal control weaknesses tied directly to the accounting system.

Those external pressures took a toll on the team as well. The controller — hired specifically for her NetSuite expertise — spent 60% of her time troubleshooting system issues rather than providing strategic financial analysis. Staff turnover risk increased. Program leaders stopped trusting financial reports and began making resource allocation decisions based on instinct rather than data.

Strategy Applied

One Abacus Advisory led a three-phase recovery:

Phase 1: System configuration audit (Weeks 1-4)

- Conducted a comprehensive review of chart of accounts structure, fund accounting setup, and grant tracking modules

- Identified 23 configuration errors, including incorrect revenue recognition rules and broken allocation logic

- Documented billing workflow gaps causing accounts receivable aging issues

- Assessed reporting templates against both internal management needs and external funder requirements

Phase 2: Reconfiguration and staff retraining (Weeks 5-10)

- Corrected system configurations with proper fund accounting hierarchies

- Rebuilt billing workflows to automate invoicing and payment application

- Retrained all finance staff on correct system use with documented procedures for common tasks

- Created quick-reference guides and video tutorials for month-end close processes

Phase 3: Reporting template restructuring (Weeks 11-16)

- Designed board financial statements that pulled directly from NetSuite without manual adjustments

- Built grant expenditure reports aligned with funder requirements

- Created program profitability dashboards for leadership decision-making

- Established a financial reporting calendar with system-generated deliverables

Outcome

Reliable financial statements were restored. Grant tracking reconciled, giving program managers real-time visibility into available balances. Accounts receivable days dropped from 112 to 38 within four months as proper billing workflows took effect. Shadow spreadsheets were eliminated, removing the compliance and version control risks they created.

The controller shifted from firefighting to strategic analysis. External auditors removed the internal control finding in the next audit cycle. Board members received consistent, accurate financial information that supported informed governance.

Key Takeaway

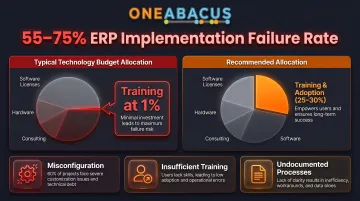

A new system only delivers on its promise when it's configured for your fund structure, your staff knows how to use it, and documented processes hold it together. Without those elements, the software becomes the source of financial risk rather than the solution to it. ERP implementation failure rates range from 55% to 75%, with only 1% of nonprofit technology budgets allocated to training. The lesson: budget for change management with the same seriousness as software procurement.

Proven Turnaround Strategies and the Role of Fractional CFO Support

Three Common Threads Across All Turnarounds

The case studies reveal consistent patterns:

Early action matters more than intervention size: Organizations that responded to warning signs—delayed closes, turnover in finance roles, concentration risk—recovered faster than those that waited until audit failure or cash insolvency forced action. Acting at the first sign of trouble—even with limited resources—consistently outperforms delayed, larger interventions.

Financial controls and documentation are the foundation: Before pursuing growth, diversification, or innovation, nonprofits must stabilize basic financial operations. Closed books, reconciled accounts, documented procedures, and reliable reporting are the platform on which all other strategies rest. Without them, growth efforts collapse.

Board engagement in financial oversight isn't optional during turnaround: The board provides the steering mechanism. Monthly financial reviews, informed questions about variance and cash flow, and active participation in scenario planning transform governance from passive approval to active oversight. 84% of nonprofits with government funding reported financial concerns in 2025—boards must engage with that reality.

Why Fractional CFO Support Fits Nonprofit Turnarounds

Fractional CFO and COO services are especially suited to turnaround situations for three reasons.

Senior-Level Leadership Without Full-Time Cost

Nonprofit CFO salaries for organizations with $2–10 million budgets range from $135,000 to $159,000 depending on region. Fractional CFO engagements cost $3,000–$15,000 per month, delivering strategic finance capacity at 30–50% of full-time cost.

For organizations under $10 million in revenue, fractional leadership offers the right expertise without the hiring timeline or compensation burden of a full-time executive.

Immediate Availability During Crisis

Recruiting a full-time CFO takes 4–6 months on average. During a turnaround, that delay can be catastrophic. Fractional providers like One Abacus Advisory step in within weeks, stabilizing operations while permanent leadership is recruited.

They bring cross-sector nonprofit expertise that internal staff rarely have—having navigated similar turnarounds across multiple organizations.

Tailored Scope Matching Turnaround Needs

Not every turnaround requires the same intervention. Fractional engagements flex to the specific challenge:

- Interim CFO support during leadership transitions

- Accounting stabilization and month-end close recovery

- System optimization (including NetSuite implementation)

- Board-level financial reporting improvements

This flexibility delivers the right expertise at the right moment without overbuilding infrastructure.

One Abacus Advisory provides fractional financial leadership specifically designed for nonprofits—including interim CFO support, accounting stabilization, and board-level financial reporting tailored to turnaround situations.

Immediate Turnaround Priorities: A Checklist

Any nonprofit leader can act on these short-term priorities immediately:

- Close your books monthly — reconciled, documented, and delivered to leadership within 15 business days of month-end