Introduction

Grants keep many nonprofits operational — and they come with compliance obligations that can't be ignored. Without a clear system for tracking and reporting how funds are used, your organization risks audit findings, clawbacks, and loss of tax-exempt status.

Government grants alone totaled approximately $303 billion annually across over 100,000 U.S. nonprofits, according to Candid's 2025 analysis. Yet many organizations struggle to manage these funds properly, leading to audit findings, clawbacks, and even automatic IRS revocation of tax-exempt status after three consecutive years of noncompliance.

This guide explains what grant accounting is, how grants are classified and recognized, what compliance frameworks nonprofits must follow, and actionable best practices for managing grant funds with confidence.

Here's what you need to know before diving in.

TLDR: Key Takeaways

- Grant accounting tracks how grant funds are received and spent according to grantor terms and accounting standards

- Grants are classified as exchange transactions or contributions (conditional or unconditional), each requiring different revenue recognition

- Proper grant accounting protects nonprofit status, maintains funder trust, and positions organizations for future funding

- Nonprofits follow GAAP fund accounting; federal grantees must also comply with Uniform Guidance (2 CFR Part 200)

What Is Grant Accounting for Nonprofits?

Grant accounting is the specialized financial practice of tracking all financial activity related to grants — including revenue recognition, expense allocation, compliance monitoring, and funder reporting. It goes beyond general bookkeeping by requiring adherence to both funder-specific grant agreements and formal accounting standards.

Grants come from government agencies, private foundations, corporations, and individuals. Unlike loans, they typically don't require repayment — unless the recipient violates conditions or fails to meet reporting requirements.

How Grant Accounting Differs from For-Profit Accounting

Nonprofits use fund accounting, which separates resources by restriction and purpose rather than tracking profit and loss. Under FASB ASC 958, nonprofits classify net assets into two categories:

- Net assets without donor restrictions (unrestricted funds)

- Net assets with donor restrictions (restricted to specific programs, time periods, or purposes)

This distinction drives every downstream decision — from how expenses get coded to how financial statements are presented to funders.

Why Grant Accounting Matters Strategically

Getting grant accounting right has consequences well beyond compliance. Done well, it:

- Maintains funder relationships — accurate, timely reporting keeps current funders confident

- Qualifies for future grants — a clean compliance record increases likelihood of renewals and new awards

- Supports board decisions — transparent financial records enable informed governance

- Demonstrates mission impact — clear allocation of grant funds proves outcomes to stakeholders

According to the Urban Institute, between 60% and 86% of grant-receiving nonprofits would operate at a loss without government grant funding. For most nonprofits, that makes disciplined grant accounting a core operational function — not an administrative afterthought.

Types of Grants and How They're Classified in Accounting

Restricted vs. Unrestricted Grants

The primary classification axis under GAAP is donor restriction:

- Restricted grants must be spent on designated programs or purposes

- Unrestricted grants give the organization flexibility in how funds are used

Both require thorough tracking and reporting, even if unrestricted.

Three Main Grant Types Under GAAP

Revenue recognition timing depends on grant type:

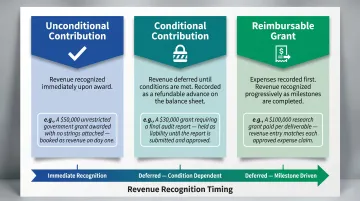

Unconditional contributions:

- Revenue recognized immediately when the grant is awarded

- No barriers or conditions must be met first

- Example: A foundation awards $50,000 to support general operations with no performance requirements

Conditional contributions:

- Revenue deferred until specific barriers or conditions are met

- Must include both a barrier and a "right of return" (grantor can reclaim funds if conditions go unmet)

- Recorded as refundable advance (liability) until conditions are satisfied

- Example: A grant requiring the nonprofit to match $1 from other donors for every $1 received

Reimbursable grants:

- Expenses recorded first as they occur

- Revenue recognized as the nonprofit meets milestones or completes the project

- Example: A government grant reimbursing actual program costs after submission of invoices

Grant Types by Origin

Government grants:

- Come with the heaviest reporting requirements of any grant type

- Federal grants require compliance with Uniform Guidance (2 CFR Part 200)

- Nonprofits expending $1 million or more in federal awards annually must undergo a single audit

- Approximately 40,000 single audits were submitted in fiscal year 2023, covering $1.1 trillion in federal awards

Private foundation grants operate under foundation-specific reporting formats and deadlines. They're generally less complex than federal grants, but compliance expectations still apply.

Corporate grants:

- May include branding, publicity, or recognition obligations

- Can blur the line between a charitable contribution and a commercial exchange

Grants vs. Loans

One more distinction worth clarifying before moving on: grants and loans are not interchangeable in accounting.

Grants are treated as revenue once conditions are met. Loans are liabilities that must be repaid and recorded on the balance sheet as debt — never as revenue.

The Two Approaches to Nonprofit Grant Revenue Recognition

The distinction between exchange transactions and contributions determines when and how revenue is recognized — and has significant compliance implications.

Contributions vs. Exchange Transactions

Exchange transaction:

- The grantor receives commensurate (roughly equal) value directly in return

- Example: A government agency hires a nonprofit to conduct research the agency will own and use

- Revenue recognized when the performance obligation is fulfilled (under ASC 606)

Contribution (conditional or unconditional):

- A voluntary transfer where the grantor receives no direct equal value in return

- The public or mission beneficiaries receive the value, not the funder

- Most government and foundation grants fall here

- Revenue recognition depends on whether the contribution is conditional or unconditional (under ASC 958-605)

FASB ASU 2018-08 clarifies that the resource provider (funder) is not synonymous with the general public. When a community benefits from a funded program, that indirect benefit does not count as commensurate value to the funder itself.

Conditional contributions must include both:

- A barrier to overcome — such as a measurable performance requirement, limited discretion over fund use, or a specific purpose stipulation

- A right of return (assets must be returned if barrier is not met) or right of release from obligation

Practical Example: Same Grant, Different Classification

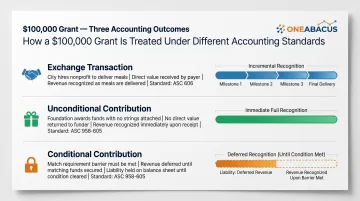

Consider a $100,000 award to provide meal services — the classification shifts entirely based on the grant structure:

Exchange transaction:

- A city hires the nonprofit to deliver 10,000 meals to the city's senior centers

- The city receives direct value (meals for its constituents)

- Revenue recognized as meals are delivered

Unconditional contribution:

- A foundation awards $100,000 to support the nonprofit's meal program

- Foundation receives no direct value; community benefits

- No specific performance barriers or right of return

- Revenue recognized immediately upon award

Conditional contribution:

- A foundation awards $100,000 to provide meals, but only after the nonprofit raises $100,000 in matching funds

- Barrier (match requirement) and right of return exist

- Revenue deferred (recorded as refundable advance) until match is secured

Each scenario uses the same dollar amount — but the accounting treatment is completely different. Getting the classification wrong has real consequences.

Why Classification Matters

Misclassifying a conditional contribution as unconditional leads to premature revenue recognition, which can cause:

- Financial restatements

- Audit findings

- Strained grantor relationships

- IRS scrutiny and potential loss of tax-exempt status

Grant agreements almost never use terms like "conditional contribution" or "exchange transaction" — the classification requires reading the actual terms carefully and applying professional judgment to each award.

Key Components of an Effective Grant Accounting System

Revenue Recognition and Expense Tracking

Revenue recognition must align with the funding agreement type — exchange, conditional, or unconditional — because the timing determines when funds appear on financial statements.

Expense tracking is equally structured:

- Every expense charged to a grant must be traceable to an approved budget line item

- Allocating shared costs (such as staff time across multiple grants) is technically complex

Per 2 CFR 200.413, direct costs are "those costs that can be identified specifically with a particular final cost objective." Indirect costs include facilities and administration expenses.

Nonprofits may use the 15% de minimis indirect cost rate if they lack a negotiated indirect cost rate agreement (NICRA).

Fund Segregation and Separate Tracking

Restricted grant funds must be maintained separately from:

- Unrestricted operating funds

- Other restricted grants

Using unique fund codes or program segments in your accounting software lets you run grant-specific budget-vs-actual reports at any time — a straightforward way to stay ahead of compliance requirements.

Record-Keeping, Documentation, and Internal Controls

Grant accounting depends on a complete paper trail:

- Invoices and receipts

- Timesheets and personnel records

- Contracts and grant agreements

- Correspondence with funders

Per 2 CFR 200.334, financial records must be retained for three years from the date of submission of the final expenditure report.

Strong internal controls are just as critical as the documentation itself. In nonprofits with fewer than 100 employees, the most common fraud schemes include corruption (44%), billing fraud (31%), and payment tampering (23%). Segregation of duties catches errors early and reduces exposure — and organizations with fraud training cut the time to uncover fraud from 24 months to just 9 months, reporting 50% lower losses.

Staying Compliant: GAAP, Uniform Guidance, and Grantor Requirements

GAAP Compliance for Nonprofits

U.S. nonprofits must follow GAAP as set by FASB, which requires:

- Accrual-basis accounting — revenue and expenses recognized when earned or incurred, not when cash changes hands

- Fund accounting methodology — resources separated by restriction and purpose

- ASC 958 revenue recognition rules — specific treatment for contributions and exchange transactions

Federal Grant Compliance — Uniform Guidance (2 CFR Part 200)

Nonprofits receiving federal funding face additional requirements under Uniform Guidance, including:

- Cost principles — expenses must be reasonable, allowable, and allocable; each cost must be treated consistently as direct or indirect

- Administrative requirements — financial management systems must identify all federal awards, produce accurate financial results, and maintain effective internal controls

Single audit threshold:

- Nonprofits expending $1 million or more in federal awards during their fiscal year must undergo a single audit

- This threshold increased from $750,000 in April 2024, effective for fiscal years ending on or after September 30, 2025

Grantor-Specific Reporting Requirements

Meeting GAAP and Uniform Guidance is the baseline — but each grantor typically layers on its own conditions as well. These can include:

- Custom reporting formats

- Specific deadlines

- Performance metrics and narrative requirements

Failing to meet these requirements carries real consequences:

- Clawbacks (returning grant funds)

- Financial penalties

- Loss of future funding eligibility

- Automatic IRS revocation of tax-exempt status after three consecutive years of failing to file Form 990

Best Practices for Nonprofit Grant Accounting Management

Implement a Dedicated Tracking and Accounting System

Manual spreadsheets become untenable as grant portfolios grow. Nonprofits should use accounting software that:

- Supports fund accounting with multiple restricted funds

- Enables grant-specific reporting

- Generates funder-required financial statements on demand

- Sets budget alerts to prevent overspending

NetSuite, for example, can be configured to manage complex grant portfolios, produce customizable reports, and automate compliance tracking. One Abacus Advisory specializes in setting up these environments specifically for nonprofits.

Conduct Regular Reconciliations and Internal Reviews

Monthly or quarterly reviews:

- Compare grant budgets to actual spending

- Identify variances early, before they become audit findings

- Verify expense allocations across multiple grants

Milestone reviews:

- Align internal reviews with grant reporting deadlines

- Ensure all documentation is complete and accurate

- Prepare for funder site visits or audits

Know When to Bring in Fractional Financial Leadership

Many small and mid-size nonprofits lack dedicated CFO or senior finance staff to manage complex grant portfolios. 92% of nonprofits operate on less than $1 million annually, making a full-time hire out of reach for most.

Fractional CFO services, such as those offered by One Abacus Advisory, provide nonprofit-specific financial expertise scaled to what an organization actually needs. These engagements help nonprofits:

- Build strong grant accounting systems

- Prepare for audits

- Maintain funder confidence

- Navigate leadership transitions without disruption

Demand for fractional CFOs has increased 103% year-over-year, with businesses saving 30-40% compared to full-time hires. For nonprofits under audit pressure or navigating a leadership gap, that cost difference can be redirected directly into mission delivery.

Frequently Asked Questions

How do nonprofits account for grant revenue?

Revenue recognition depends on grant type. Unconditional grants are recognized when awarded. Conditional grants are recognized when conditions or barriers are met. Reimbursable grants are recognized as milestones are completed and expenses incurred.

What are the two approaches to nonprofit grant accounting?

The two core approaches are exchange transactions (where the grantor receives direct equal value) and contributions (where no equal value is returned). Within contributions, conditional and unconditional grants each carry different revenue recognition timing under GAAP.

What is federal grant accounting for nonprofits?

Federal grant accounting involves following Uniform Guidance (2 CFR Part 200), which sets cost principles, administrative requirements, and audit standards. Organizations expending $1 million or more in federal awards annually must undergo an independent single audit.

Are grants considered revenue or liabilities for nonprofits?

Grants are recognized as revenue once eligibility conditions are met. However, conditional grants are recorded as a liability (refundable advance or deferred revenue) until those conditions are satisfied, since the nonprofit has an obligation to return funds if conditions go unmet.

Is grant accounting difficult?

Grant accounting is complex, particularly when managing multiple restricted grants with different compliance requirements. Clear policies, proper accounting systems, and the right financial expertise make it manageable over time.

What type of accounting do nonprofits use?

Nonprofits use fund accounting, which separates resources into designated funds based on donor restrictions and program purposes. GAAP also requires accrual-basis accounting, meaning revenue and expenses are recognized when earned or incurred — not just when cash changes hands.