Introduction

Many nonprofits operate on unspoken financial assumptions rather than written policies — and that gap creates real exposure. Without documented standards, organizations risk misuse of funds, compliance failures, and personal legal liability for board members.

This guide covers what nonprofits need to close that gap:

- The core financial accountability policies every organization should have in writing

- Who holds responsibility for financial oversight — and how that's defined

- Practical steps to build and maintain these protections

Key Takeaways

- Financial accountability policies define decision-making authority, fund handling procedures, and compliance safeguards

- Critical policies include conflict of interest, spending authority, internal controls, restricted fund management, gift acceptance, and operating reserves

- Boards hold fiduciary responsibility for oversight; Executive Directors manage day-to-day operations; Treasurers and Finance Committees provide additional checks

- Policies require formal board adoption, staff communication, and annual review; update immediately after any organizational or regulatory changes

What Are Financial Accountability Policies (and Why They Matter)

Financial accountability policies are formal, board-approved documents that clarify how a nonprofit handles financial decisions, transactions, authority, and oversight. Policies define the standards an organization commits to uphold; procedures describe the specific steps staff take to execute them.

Fiduciary Duty and Legal Foundation

Board members carry legal and ethical fiduciary duty to act in the organization's best interest. This duty encompasses three core obligations:

- Duty of care - Making informed decisions with appropriate deliberation

- Duty of loyalty - Placing organizational interests above personal benefit

- Duty of obedience - Ensuring the organization follows its mission and complies with applicable laws

Financial policies serve as the primary mechanism through which boards exercise these duties. The IRS explicitly states that a "well-governed charity is more likely to obey tax laws and safeguard charitable assets," and Form 990 Part VI specifically asks whether organizations have adopted key governance and financial policies.

Real Risks of Operating Without Policies

The consequences of neglecting financial policies are measurable and serious. Research from the Association of Certified Fraud Examiners (ACFE) found that nonprofit organizations represented 10% of occupational fraud cases in 2024, with a median loss of $76,000 per incident. The data shows that organizations typically lose approximately 5% of annual revenue to fraud.

Detection challenges compound the problem: fraud goes undetected for an average of 24 months in organizations without anti-fraud training, compared to just 9 months in organizations with training programs. 68% of nonprofits lack documented cybersecurity policies, exposing them to digital fraud risks on top of internal vulnerabilities.

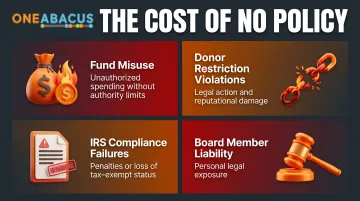

Operating without documented financial policies creates specific vulnerabilities:

- Funds misused or misappropriated without clear authority limits

- Donor restrictions violated, triggering legal action and irreparable reputational damage

- IRS compliance failures resulting in penalties or loss of tax-exempt status

- Personal liability exposure for board members who failed their fiduciary duty

Financial policies address these vulnerabilities directly. They create predictability, reduce friction between staff and board, and give the organization a clear, documented defense when funders, auditors, or regulators ask hard questions. Shared expectations about how money moves — and who authorizes each decision — are the foundation that makes everything else work.

Scaling Policies to Organization Size

A grassroots nonprofit with a $200,000 budget and an all-volunteer board needs different policy depth than a $10 million organization running multiple programs with full-time staff. Every nonprofit still needs written policies — the scope just differs. Smaller organizations can start with a consolidated single document and expand it as complexity grows.

Essential Financial Policies Every Nonprofit Needs

Conflict of Interest Policy

Few governance documents carry more weight than a conflict of interest policy. IRS Form 990 Part VI specifically asks whether the organization has a written policy, requires annual disclosure statements, and monitors compliance — making it one of the few governance items the IRS scrutinizes by name.

A strong conflict of interest policy should:

- Require board members and senior staff to disclose relationships or financial interests that could influence organizational decisions

- Define what constitutes a conflict (financial interests, family relationships, business connections)

- Establish a clear recusal process when conflicts arise

- Document how disclosed conflicts are reviewed and managed

- Include annual disclosure statement requirements

While the IRS does not legally mandate conflict of interest policies, adopting and enforcing one demonstrates good governance and reduces the risk of board decisions being successfully challenged.

Spending Authority and Check-Signing Policy

Without defined spending authority, unauthorized commitments happen — and confusion about who approved what follows. This policy sets clear dollar thresholds for expenditure approvals and check signing before those situations arise.

A typical tiered structure might look like:

- Under $2,500: Executive Director approval

- $2,500 to $15,000: Executive Director approval with Treasurer notification

- Over $15,000: Board Chair or Treasurer co-signature required

Note: These thresholds are illustrative examples—each organization should set limits appropriate to its budget size and risk tolerance.

Beyond routine expenditures, the policy should explicitly address authority to:

- Enter contracts or multi-year commitments

- Open bank accounts or lines of credit

- Establish or modify payroll arrangements

- Make investment decisions

According to the National Council of Nonprofits, clear financial policies help "clarify roles, authority, and responsibilities," reducing the risk of misunderstandings that can damage organizational relationships.

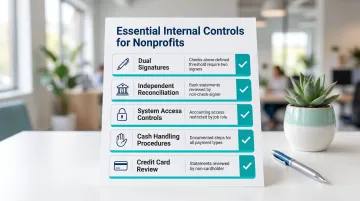

Internal Controls and Segregation of Duties

No single person should have end-to-end control over a financial transaction. The person who receives funds should not be the same person who records them or reconciles bank statements — that's the core of segregation of duties.

Small nonprofits with limited staff often struggle to apply this principle. For them, the AICPA publishes segregation of duties reference charts designed specifically for organizations with two or three staff members — proof that basic controls are achievable at any size.

Essential internal controls include:

- Dual signatures required on checks above a defined threshold

- Regular bank reconciliations performed by someone other than the check signer

- Restricted access to accounting systems based on job function

- Documented procedures for handling cash, checks, and online payments

- Periodic review of credit card statements by someone other than the cardholder

Auditors define a "material weakness" as a control deficiency that creates a reasonable possibility of material misstatement in financial statements. Strong segregation of duties is one of the most direct ways to keep that finding off your audit report.

Restricted Fund Management and Gift Acceptance

Donor-restricted funds must be tracked separately from general operating funds. Using restricted funds outside their designated purpose can trigger legal liability under state charitable solicitation laws and permanently damage donor relationships.

The Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) 958 requires nonprofits to classify net assets into two categories: with donor restrictions and without donor restrictions. This classification isn't just an accounting convention — it reflects a legal obligation to honor donor intent.

Consequences of misusing restricted funds include:

- IRS sanctions and potential loss of tax-exempt status

- State Attorney General enforcement actions

- Donor legal action to recover funds or seek specific performance

- Reputational damage that undermines future fundraising

Gift Acceptance Policy

A gift acceptance policy defines what types of contributions the organization will accept and under what conditions. According to the National Council of Nonprofits, this policy should address:

- Types of acceptable gifts (cash, stock, in-kind goods, real estate, planned gifts)

- How non-cash gifts are valued and recorded

- What gifts require board approval before acceptance (typically high-value or complex gifts)

- Conditions under which gifts may be declined (e.g., restricted in ways that don't align with mission)

The IRS requires Form 8283 for non-cash contributions over $500, with qualified appraisals required for property claimed at values exceeding $5,000. Organizations receiving $25,000 or more in non-cash contributions must also complete Schedule M of Form 990.

Operating Reserves and Investment Policy

An operating reserve policy defines the target level of reserves the organization aims to maintain, who can authorize use of reserves, and how depleted reserves are replenished.

The National Council of Nonprofits notes that while there is no universal standard, many nonprofits target reserves equal to three to six months of operating expenses. This range provides a cushion for cash flow fluctuations, unexpected expenses, or temporary revenue shortfalls.

Key elements of a reserve policy include:

- Target reserve level (typically expressed as months of operating expenses)

- Purpose of reserves (operating continuity, specific contingencies, capital needs)

- Conditions under which reserves may be used

- Board approval requirements for reserve use

- Timeline and method for replenishing reserves

Organizations holding investment assets need a formal investment policy that covers:

- Acceptable risk parameters and return expectations

- Asset allocation guidelines

- Who oversees the investment portfolio (often an Investment Committee)

- Spending policy for endowment funds

- Rebalancing procedures

Roles and Responsibilities in Nonprofit Financial Accountability

Board of Directors

The board holds ultimate fiduciary responsibility for financial oversight. BoardSource defines board financial responsibilities to include:

- Approving the annual budget and ensuring it aligns with strategic priorities

- Reviewing financial reports at each board meeting

- Adopting and enforcing financial policies

- Ensuring organizational assets are protected and used according to mission

- Providing oversight during audits and acting on audit findings

The board acts collectively to establish financial parameters and monitor organizational financial health. Individual board members cannot direct financial decisions outside the board's established authority structure.

Executive Director

The Executive Director carries responsibility for day-to-day financial management within the parameters established by board policy. Typical ED financial responsibilities include:

- Executing the approved budget

- Maintaining accurate financial records

- Ensuring staff follow established financial procedures

- Reporting financial results to the board on the schedule established by the Finance Committee

- Identifying financial issues that require board attention

- Recommending budget adjustments when circumstances change

The ED translates board policy into operational practice and serves as the primary financial communication link between staff operations and board oversight.

Treasurer and Finance Committee

The Treasurer serves as the board's financial watchdog, typically chairing the Finance Committee and providing more detailed oversight between board meetings. Treasurer responsibilities include:

- Reviewing financial statements before board meetings to identify questions or concerns

- Working closely with the ED or CFO to understand financial trends

- Acting on the board's behalf on time-sensitive financial matters between meetings

- Leading the budget development process

- Coordinating the annual audit

The Finance Committee provides detailed financial oversight that would be impractical for the full board. This committee typically reviews monthly financials, monitors cash flow, oversees investment management, and recommends financial policies to the full board for adoption.

Bridging the Gap with Fractional Financial Leadership

Many nonprofits—particularly mid-sized organizations without a full-time CFO—need to fill the space between an ED's operational focus and the board's oversight role. These situations—growth phases, leadership transitions, audit preparation—call for senior financial expertise that a full-time hire can't always justify.

One Abacus Advisory's fractional CFO services give nonprofits access to senior financial leadership on a right-sized basis. For organizations like the San Diego Food Bank or Laguna Playhouse, that has meant:

- Establishing financial reporting structure aligned with board oversight needs

- Supporting compliance and audit readiness without disrupting operations

- Providing strategic financial guidance during leadership transitions

The result is a cleaner connection between day-to-day management and board fiduciary responsibility—without the overhead of a permanent executive hire.

How to Develop and Implement Financial Accountability Policies

Development Process

Creating effective financial policies requires a structured approach:

1. Assess current practices and identify gaps Convene the Treasurer and Finance Committee to document how financial decisions are currently made, who has authority at different levels, and where gaps or ambiguities exist.

**2. Conduct an informal risk assessment** Surface the highest-priority policy needs by considering:

- Where have conflicts or confusion occurred in the past?

- What financial decisions lack clear authority?

- What would happen if a key financial person left tomorrow?

- What questions do auditors or funders typically raise?

3. Draft policies with appropriate detail Create policy drafts that are specific enough to provide clear guidance but flexible enough to accommodate reasonable operational needs. Circulate drafts to staff and leadership for review before board presentation.

4. Present to the full board for formal adoption The Finance Committee should present recommended policies to the full board with rationale for each provision. Policies become official only when formally adopted by board vote and documented in meeting minutes.

Implementation and Communication

Adopting a policy is only half the work—it still has to function in practice. Three steps make that happen:

Train the right people. Every staff member who handles financial transactions or makes financial decisions must understand the relevant policies. A financial procedures manual helps by documenting how each policy commitment plays out day-to-day.

Make policies easy to find. Maintain policies in a central location accessible to board members, staff, and relevant volunteers. Include key policies in board orientation materials and staff handbooks so they're encountered early, not after a problem surfaces.

Update your systems. Accounting software, approval workflows, and financial reporting templates all need to reflect policy requirements. If a policy requires dual signatures above $10,000, the check printing process should enforce that—not rely on memory.

Avoid Template Traps

While policy templates provide a starting point, adopting templates without customization creates false security. Every template should be reviewed against:

- The organization's actual operations and staffing structure

- Specific risk profile (funding sources, program complexity, geographic scope)

- Governance structure and decision-making culture

- Applicable state laws and funder requirements

Before finalizing any template-based policy, test it against a recent real decision: would this policy have provided clear guidance? If the answer is no, revise until it does.

How to Maintain and Review Your Policies Over Time

Annual Review Cycle

Financial policies should be formally reviewed at least annually, ideally as a standing Finance Committee agenda item. The review should assess:

- Whether policies still reflect current operations and organizational structure

- Whether policies align with current IRS requirements and state laws

- Whether any policy violations or ambiguities occurred during the year

- Whether policy thresholds need adjustment (e.g., spending authority limits may need updating as the budget grows)

Immediate Review Triggers

Certain organizational changes should prompt immediate policy review outside the annual cycle:

- Staff turnover in financial roles (CFO, Controller, Finance Director, ED)

- Discovery of a financial irregularity or policy violation

- Significant new funding source with specific compliance requirements

- Major change in organizational size or complexity (e.g., doubling the budget, adding new programs)

- Changes in banking relationships or accounting systems

- New state or federal regulatory requirements

The Audit as Accountability Mechanism

The annual audit (or financial review for smaller organizations) acts as a formal accountability check. Auditors evaluate whether the organization has adequate policies and internal controls, and audit reports often flag policy gaps or control weaknesses.

Key audit thresholds nonprofits should know:

- $750,000+ in federal expenditures triggers a Single Audit requirement under federal law

- 39 states plus the District of Columbia require charitable registration, many with their own audit thresholds

- State requirements vary widely — check your state's specific rules if you receive state funding

Audit findings should directly inform policy updates — treat each finding as a specific action item, not just a compliance checkbox. Organizations that consistently receive clean audit opinions also tend to have an easier time securing major grants, since many funders review audit reports before committing significant dollars.

Frequently Asked Questions

What financial policies should a nonprofit have?

Every nonprofit needs core policies covering conflict of interest, spending authority, internal controls and segregation of duties, restricted fund management, gift acceptance, and operating reserves. Complexity should scale with organizational size and risk, but even small organizations require these fundamentals in place.

Who is legally accountable for a nonprofit organization's actions?

The board of directors holds ultimate legal and fiduciary accountability for nonprofit actions. Day-to-day financial responsibility rests with the Executive Director. Both board members and executives can face personal liability when policies are neglected or financial misconduct is ignored.

What is the difference between a financial policy and a financial procedure?

A policy defines what the organization commits to—for example, requiring dual signatures on checks above $10,000. A procedure describes how that commitment is carried out in practice—the specific steps for preparing a check, routing it for signatures, and recording the transaction.

How often should nonprofit financial policies be reviewed?

Review policies formally at least once a year, with immediate reviews triggered by organizational changes, regulatory updates, staff turnover in financial roles, or any discovered financial irregularity. The annual review should be a standing Finance Committee agenda item.

What is the role of the board treasurer in financial accountability?

The Treasurer serves as the board's financial watchdog, reviewing statements before meetings and acting on the board's behalf when a full vote isn't practical between sessions. This includes working closely with the ED or CFO on day-to-day financial oversight. The Treasurer typically chairs the Finance Committee.

Do small nonprofits need formal financial accountability policies?

Yes, all nonprofits regardless of size need written financial policies. Smaller organizations can start with a consolidated single-document policy covering the essential areas, then add detail and specificity as the organization grows.