Introduction

IRS Form 990 is more than a compliance checkbox for nonprofits — it's a public document that donors, grantmakers, and watchdog organizations actively review before making funding decisions. Filing accurately and on time protects your tax-exempt status and signals financial credibility to everyone watching.

Donors, foundations, and journalists regularly pull 990 filings through platforms like ProPublica's Nonprofit Explorer and Candid's GuideStar. What they find shapes their trust in your organization.

Miss three consecutive filings, and the IRS automatically revokes your tax-exempt status — triggering federal income tax liability and stripping donors of their deduction eligibility.

Key Takeaways

- Miss three consecutive filings and the IRS automatically revokes your exempt status — Form 990 compliance isn't optional

- Four versions exist (990-N, 990-EZ, 990, 990-PF), each determined by your organization's annual gross receipts and total assets

- Filing deadline is the 15th day of the 5th month after fiscal year-end; request extensions via Form 8868

- Your 990 is public record — use it as a transparency tool that builds donor and stakeholder trust, not just a compliance checkbox

What Is IRS Form 990 and Why Does It Matter?

Form 990 is an annual information return — not a tax return in the traditional sense — that the IRS uses to verify whether a tax-exempt organization still qualifies for its exemption. It requires disclosure across three areas:

- Financial activity: income, expenses, and assets

- Governance practices: board structure, policies, and conflicts of interest

- Program accomplishments: what your organization actually did to advance its mission

Unlike standard business filings, nonprofits generally don't pay income tax on revenue tied to their exempt purpose. They must still report income, expenses, and executive compensation annually. Tax exemption is a substantial public benefit, and the government expects transparency in return.

Form 990 is publicly available by law. The IRS requires organizations to make their three most recent returns available for public inspection, and platforms like ProPublica's Nonprofit Explorer and Candid publish them online. That public visibility turns the 990 into more than a compliance document — donors, foundations, and journalists use it to evaluate your organization's health and credibility.

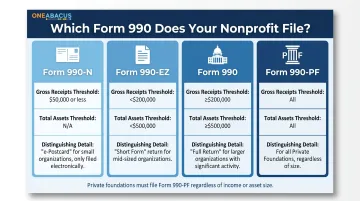

Which Form 990 Does Your Nonprofit Need to File?

Four main versions of Form 990 exist, and which one applies depends on your organization's annual gross receipts and total assets—not organization type alone.

| Form Version | Gross Receipts | Total Assets | Key Details |

|---|---|---|---|

| 990-N | ≤$50,000 | N/A | Electronic-only; no paper option |

| 990-EZ | <$200,000 | <$500,000 | Both thresholds must be met |

| 990 | ≥$200,000 | ≥$500,000 | Required if either threshold met |

| 990-PF | Any amount | Any amount | All private foundations must file |

Gross Receipts Under $50,000: Form 990-N (e-Postcard)

Organizations with annual gross receipts of $50,000 or less satisfy their filing requirement through the 990-N (e-Postcard), an electronic-only notice. It requires just eight basic items:

- EIN and tax year

- Legal name and mailing address

- Principal officer information

- Website URL (if applicable)

- Confirmation of gross receipts

- Confirmation of termination (if applicable)

The $50,000 threshold uses a rolling average: organizations in existence three or more years average gross receipts over the immediately preceding three tax years.

Not every small organization qualifies, however. The following types cannot file 990-N even if they meet the threshold:

- Private foundations

- Section 509(a)(3) supporting organizations

- Section 527 political organizations

Gross Receipts Under $200,000 and Assets Under $500,000: Form 990-EZ

Organizations meeting both thresholds may file the 990-EZ, a simplified version of the full form. Some organizations in this range voluntarily file the full Form 990 instead—a useful strategy when seeking grants or major donations, since funders often review 990s to evaluate financial health and program impact.

Gross Receipts of $200,000 or More, or Assets of $500,000 or More: Form 990

The full Form 990 is required once an organization crosses either threshold. This comprehensive return includes detailed schedules covering governance, compensation, functional expenses, program service accomplishments, and more—up to 16 possible supplemental schedules depending on organizational activities.

Which schedules apply depends on what your organization does. A nonprofit that conducts lobbying, holds foreign assets, or runs a hospital facility will trigger schedules that a straightforward public charity may never need.

Private Foundations: Form 990-PF and Form 990-T

Private foundations, regardless of size, must file Form 990-PF, which has different disclosure requirements than the standard 990 series. Any nonprofit with $1,000 or more of gross income from an unrelated business must also file Form 990-T (Exempt Organization Business Income Tax Return) in addition to their 990 series form.

What Goes Into a Form 990 Filing?

The full Form 990 captures far more than basic financial data. The main form requires disclosure of revenue, expenses, net assets, and functional expense allocations across program services, management and general expenses, and fundraising. Executive and key employee compensation—defined as those receiving $150,000 or more in reportable compensation—ranks among the most scrutinized sections.

Supplemental Schedules: The Hidden Complexity

Supplemental schedules create much of Form 990's complexity. Missing or incomplete schedules represent one of the most common reasons the IRS rejects filings:

- Schedule A documents public charity status and public support calculations

- Schedule B lists contributors (names are kept confidential by the IRS)

- Schedule O provides narrative explanations for flagged items

- Schedule J details executive compensation arrangements

Organizations must carefully determine which schedules apply to their specific activities and financial structure.

Program Service Accomplishments: Your Public Story

Part III of Form 990 gives nonprofits the opportunity to describe their mission impact in their own words. Many fundraisers and advisors treat this section as a marketing document visible to potential donors and grantmakers.

A fractional CFO, like those at One Abacus Advisory, helps ensure these narratives are accurate and compelling, translating program outcomes into language that connects with donors and grantmakers.

Board Review: A Governance Best Practice

Form 990 Part VI, Question 11 asks whether the full board of directors reviewed the return before filing. While not legally required, the IRS treats this as a governance best practice, and skipping this step raises red flags for sophisticated donors and foundations. Boards should establish a formal pre-filing review process to catch errors and ensure the narrative accurately represents organizational activities.

Form 990 Deadlines, Extensions, and Electronic Filing Requirements

Standard Deadline and Extension Process

Form 990 (all versions except 990-N) is due on the 15th day of the 5th month after the close of the fiscal year. For calendar-year organizations, this means May 15. If the due date falls on a weekend or federal holiday, the deadline shifts to the next business day.

Nonprofits can request an automatic 6-month extension by filing Form 8868 before the original deadline. Organizations must file proactively; the extension cannot be requested after the due date has passed.

Form 990-N cannot be extended, though no financial penalty applies for late submission of the e-Postcard. Note that automatic revocation rules still apply after three consecutive years of non-filing.

Electronic Filing Mandate

Under the Taxpayer First Act enacted July 1, 2019, electronic filing is now mandatory for all 990-series forms:

- Form 990 and 990-PF: Required for tax years beginning after July 1, 2019

- Form 990-EZ: Required for tax years ending July 31, 2021 and later

- Form 990-N: Always electronic-only since inception

Paper filing is no longer permitted for any of these forms.

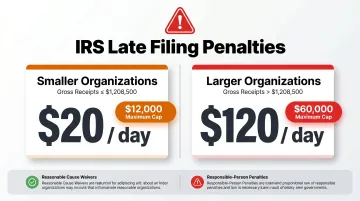

Late Filing Penalties

Penalty amounts are inflation-adjusted annually. Current figures (2026):

| Organization Size | Daily Penalty | Maximum Penalty |

|---|---|---|

| Gross receipts ≤$1,208,500 | $20/day | $12,000 or 5% of gross receipts (whichever is less) |

| Gross receipts >$1,208,500 | $120/day | $60,000 |

The IRS may waive penalties if the organization demonstrates reasonable cause for the delay. If the IRS sends a written demand and the organization fails to comply, responsible persons—such as officers or directors—may face an additional $10/day penalty, up to $5,000 aggregate.

What Happens If You Don't File—and Mistakes to Avoid

Automatic Revocation Rule

A nonprofit that fails to file a required Form 990, 990-EZ, 990-PF, or 990-N for three consecutive years automatically loses its tax-exempt status on the filing due date of the third missed year. This automatic revocation under IRC Section 6033(j) creates immediate consequences:

- Federal income tax liability begins

- Donors can no longer claim tax deductions for contributions

- The IRS adds the organization's name to the Auto-Revocation List

- No appeal process is available

Reinstatement requires reapplying for tax-exempt status. The IRS cannot simply "undo" a revocation.

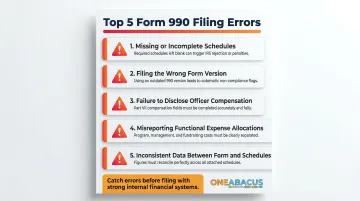

Common Filing Errors

The most frequent errors that lead to rejection or IRS scrutiny include:

- Incomplete or missing schedules required based on financial activities

- Filing the wrong form version for the organization's size

- Failure to disclose compensation for officers above reporting thresholds

- Misreporting functional expense allocations across program, management, and fundraising categories

- Inconsistent financial data between the main form and schedules

Catching these errors before filing starts with strong internal financial systems. One Abacus Advisory's accounting optimization services help nonprofits build those systems—so issues surface during review, not after submission.

Filing Is Required Even If You're Tax-Exempt

Nonprofit status does not exempt an organization from filing requirements. Even very small nonprofits must file at minimum the 990-N each year. Organizations incorporated in a state face additional state-level filing requirements separate from the federal Form 990. These vary by state and often include charitable solicitation registrations.

Frequently Asked Questions

What is a 990 form used for for nonprofits?

Form 990 serves as the IRS's annual accountability check on tax-exempt organizations, documenting financial activity, governance practices, and program accomplishments. It's also a public document that donors and grantmakers review to assess organizational health and determine funding decisions.

What are the four different types of Form 990?

There are four versions, each tied to organization size or type:

- Form 990-N — e-Postcard for organizations with gross receipts under $50,000

- Form 990-EZ — For organizations under $200,000 in revenue and $500,000 in assets

- Form 990 — Full return required once either EZ threshold is exceeded

- Form 990-PF — Required of all private foundations regardless of size

Do I file 990 or 990-EZ?

If annual gross receipts are under $200,000 AND total assets are under $500,000, the 990-EZ is an option, but organizations may choose to file the full Form 990 voluntarily. Once either threshold is exceeded, the full Form 990 is required.

Does a 501(c)(3) have to file a 990 every year?

Yes, almost all 501(c)(3) organizations must file annually. Narrow exceptions include churches and certain subordinate organizations covered by a group return. Failure to file for three consecutive years results in automatic loss of exempt status.

Is a 990 form public record?

Form 990 is a public document. Organizations must make their three most recent returns available for public inspection, and filed returns are accessible through IRS tools, ProPublica's Nonprofit Explorer, and Candid's search platform.

Does the IRS require electronic filing?

Yes. Under the Taxpayer First Act, e-filing is mandatory for most tax-exempt organizations:

- Form 990 and 990-PF — Electronic filing required

- Form 990-EZ — E-filing required for tax years ending July 31, 2021 and later

- Form 990-N — Has always been electronic-only; no paper option exists

Form 990 compliance goes well beyond checking boxes — it requires financial leadership that keeps your organization accurate, credible, and mission-focused. One Abacus Advisory provides fractional CFO services tailored to nonprofits, delivering the executive-level oversight needed to maintain compliance, prepare compelling narratives, and build systems that prevent costly errors. Contact Lorin Port at lorin@oneabacusadvisory.com or call 760-845-3808 to discuss how stronger financial leadership can improve your organization's reporting and governance.