Introduction

The financial reality facing nonprofits today is sobering. According to the Nonprofit Finance Fund's 2025 State of the Nonprofit Sector Survey, 36% of nonprofits ended 2024 with an operating deficit — the highest rate in 10 years of survey data. Even more concerning, 52% of respondents have three months or less cash on hand, with 18% reporting just one month of operating reserves.

For nonprofits, these numbers carry real operational weight. When 84% of government-funded organizations expect funding cuts and 85% anticipate increased demand for services in 2025, sound financial management is what keeps mission delivery intact. There is very little room for error.

This guide covers the essential components of nonprofit financial management: core processes, required documents, protective policies, best practices, and when to bring in dedicated financial leadership to handle complexity and transition.

TLDR

- 36% of nonprofits ended 2024 with operating deficits, highlighting urgent financial challenges

- Fund accounting, restricted fund tracking, and unique reporting standards define nonprofit finance

- Four core statements (Financial Position, Activities, Cash Flows, Functional Expenses) provide complete financial transparency

- Essential policies (gift acceptance, conflict of interest, expense reimbursement) prevent fraud and ensure governance

- Fractional CFOs deliver executive-level financial strategy at a fraction of full-time costs

What Is Nonprofit Financial Management (and Why It's Mission-Critical)

Nonprofit financial management covers how an organization plans, tracks, and reports on its financial resources — from individual donations to complex grant funds. For-profit companies manage finances to maximize profit. Nonprofits manage finances to keep their mission moving forward. Every financial decision should ultimately answer one question: does this advance our mission?

What Makes Nonprofit Financial Management Different

Nonprofit organizations operate under fundamentally different financial rules than their for-profit counterparts:

Multiple and diverse funding sources:

- Individual donations (unrestricted and restricted)

- Government and foundation grants (with specific conditions)

- Earned income from programs and services

- Corporate philanthropy and sponsorships

- Investment income and endowment returns

Fund accounting requirements: The FASB ASC 958 standard mandates that nonprofits track and report net assets in two categories: with donor restrictions and without donor restrictions. This isn't optional — it's a GAAP requirement that ensures donor intent is honored and grant conditions are met.

Public accountability obligations: Unlike private companies, nonprofits must make their Form 990 tax returns available for public inspection and often publish annual reports showing how resources are used.

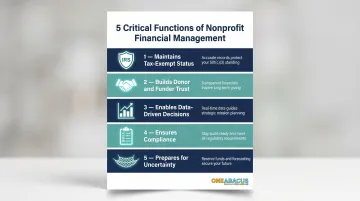

Why Strong Financial Management Matters

Effective financial management serves five critical functions:

Maintains tax-exempt status: The IRS requires annual information returns and exclusive operation for exempt purposes. Failure to file for three consecutive years results in automatic revocation of 501(c)(3) status.

Builds donor and funder trust: Transparent financial reporting demonstrates stewardship and increases giving. Research by Villanova University and University of Wisconsin-Milwaukee found that nonprofits with a GuideStar Seal of Transparency averaged 53% more in total contributions than those without.

Enables data-driven decisions: Accurate budgets, forecasts, and financial statements give leadership the data to allocate resources wisely and catch problems before they escalate.

Ensures compliance: Beyond federal requirements, nonprofits must navigate state charitable registration in approximately 40 states, employment tax filings, and complex grant reporting obligations.

Prepares for uncertainty: With 47% of nonprofits reporting inadequate funds to execute programs in 2025, financial resilience is no longer a nice-to-have — it's what keeps organizations operational when funding gaps hit.

Core Components of Nonprofit Financial Management

Budgeting and Financial Forecasting

The operating budget is your organization's financial blueprint for the year. It breaks down projected revenues by source (individual gifts, grants, earned income) and expenses by functional category (program services, management/general, fundraising). The key word is projected — budgets must be built on realistic historical data and conservative assumptions, not aspirational thinking.

Budget types nonprofits use:

- Operating budgets cover organization-wide annual spending across all departments

- Program budgets isolate financials for specific initiatives, useful for impact reporting

- Grant proposal budgets match funder requirements for individual project awards

- Capital budgets plan multi-year spending on major purchases or facilities

Each budget type must align with strategic priorities. A capital campaign budget that conflicts with operating needs signals deeper planning problems.

Rolling forecasts replace static planning: Static annual budgets become obsolete the moment they're approved. Many nonprofits now use rolling 12-month cash flow forecasts that update monthly or quarterly — spotting funding gaps before they become crises rather than reacting after the fact.

That shift from reactive to strategic is exactly where fractional CFO support adds the most value. One Abacus Advisory helps nonprofits design forecasting tools that give leadership clear, current visibility into financial performance throughout the fiscal year.

Fund Accounting and Restricted Fund Management

Fund accounting is the system nonprofits use to track money allocated to various operations and ensure funds are used according to donor and funder restrictions. Under FASB ASC 958, organizations must classify net assets as either "with donor restrictions" or "without donor restrictions" and track changes between these categories on the Statement of Activities.

When a foundation grants $50,000 specifically for youth programming, that money cannot be redirected to cover payroll shortfalls in another department — even temporarily. Misapplying restricted funds is a compliance violation that damages funder relationships and can jeopardize future grants.

Tracking multiple restricted funds simultaneously — while reconciling each against actual expenses — requires either robust accounting software or meticulous manual processes. Most organizations eventually outgrow the manual approach.

Cash Flow Management and Reserves

Cash flow management is distinct from profitability. A nonprofit can show a surplus on its Statement of Activities but still face a cash crisis if grant reimbursements are delayed or major gifts don't arrive when expected. Monthly cash flow statements track actual money moving in and out of the organization — not just accrual-basis accounting entries.

Building an operating reserve:

The National Council of Nonprofits recommends nonprofits maintain 3–6 months of operating expenses in reserve. This cushion covers funding gaps, economic downturns, and unexpected emergencies — the situations that derail organizations without a financial buffer.

The gap between the recommendation and reality is significant. According to the NFF 2025 survey, only 48% of nonprofits have more than three months of cash on hand. Building reserves takes intentional planning, board commitment, and often years of disciplined surplus generation — but it remains the single most important factor in long-term financial resilience.

Key Financial Documents Nonprofits Must Maintain

The Four Core Financial Statements

FASB ASC 958-205-45-4 requires nonprofits to produce four financial statements that together provide a complete picture of financial health:

1. Statement of Financial Position (Balance Sheet) Shows assets, liabilities, and net assets (equity) at a specific point in time. Net assets must be broken into two categories: with donor restrictions and without donor restrictions.

2. Statement of Activities (Income Statement) Reports revenues and expenses over a period (typically monthly, quarterly, or annually). This statement shows whether the organization operated at a surplus or deficit and must display changes in both categories of net assets.

3. Statement of Cash Flows Tracks actual cash movement through three activity types: operating (day-to-day operations), investing (buying/selling assets), and financing (loans, lines of credit). This statement reconciles accrual-basis accounting with cash reality.

4. Statement of Functional Expenses The one statement unique to nonprofits. It presents expenses by both function (program, management/general, fundraising) and nature (salaries, supplies, rent, depreciation). Voluntary health and welfare entities must provide this as a separate statement; other nonprofits can include it within the Statement of Activities or in the notes.

This statement is critical for demonstrating mission alignment and transparency. It shows exactly how much of every dollar reaches programs versus administration and fundraising — the number donors, boards, and watchdog organizations scrutinize most.

Chart of Accounts

The chart of accounts (COA) is the foundational directory of all financial accounts in your accounting system. A well-structured nonprofit COA includes:

- Assets: Cash, receivables, property, investments

- Liabilities: Payables, deferred revenue, loans

- Net Assets: Broken into restricted and unrestricted categories

- Revenue: By source type (contributions, grants, earned income)

- Expenses: By natural classification (salaries, rent, supplies) and functional classification (program, admin, fundraising)

A thoughtfully designed COA makes reporting, auditing, and grant tracking significantly easier — often cutting close-cycle time by days. The mistake many small nonprofits make is using generic chart structures not designed for fund accounting, creating reconciliation headaches that compound at audit time.

Form 990 and Tax Compliance

Form 990 serves as both the nonprofit's annual tax return and its primary public accountability document. The IRS provides four versions based on organizational size:

Filing thresholds:

- 990-N (e-Postcard): Gross receipts normally $50,000 or less

- 990-EZ: Gross receipts less than $200,000 AND total assets less than $500,000

- 990 (full form): Gross receipts $200,000 or more OR total assets $500,000 or more

- 990-PF: All private foundations, regardless of size

Critical deadlines: For calendar-year organizations, Form 990 is due May 15 of the following year. Form 8868 provides an automatic six-month extension to November 15 — no signature or explanation required.

Penalties for non-compliance:

- Small organizations (gross receipts under $1,208,500): $20 per day late, maximum $12,000

- Large organizations ($1,208,500+): $120 per day, maximum $60,000

- Automatic revocation after three consecutive years of non-filing

Form 990 is only one piece of the compliance picture. Nonprofits also need to manage:

- Employment tax filings: W-2s, 1099s, and quarterly payroll returns

- State charitable registration: Required in approximately 40 states for organizations soliciting donations

- Unrelated Business Income Tax (UBIT): UBIT applies when income comes from a trade or business that's regularly carried on and not substantially related to the organization's exempt purpose

Essential Financial Policies That Protect Your Organization

Written financial policies form the governance layer that prevents fraud, resolves ambiguity, and ensures consistent decision-making. The National Council of Nonprofits identifies several core policies every nonprofit should maintain.

Four Critical Policies

Gift Acceptance Policy — Defines which gift types the organization will accept (cash, stock, real estate, planned gifts) and how they'll be recorded. This protects the nonprofit from donations that create legal liability or conflict with its mission.

Conflict of Interest Policy — The most scrutinized financial policy. It defines what constitutes a conflict, sets disclosure procedures, and outlines recusal rules. The IRS asks directly on Form 990 whether your organization has a written policy and how it's enforced. New York legally requires one, and other states are moving in the same direction.

Expense Reimbursement Policy — Specifies what's reimbursable (travel, meals, supplies), documentation requirements, and approval thresholds. Clear rules prevent disputes and ensure staff are treated consistently.

Compensation Policy — Documents how pay is determined, who approves it, and when it's reviewed. This demonstrates that compensation decisions are deliberate and transparent — not made on the fly.

Policy Maintenance

Financial policies shouldn't be filed and forgotten. Boards should review the full policy handbook at least annually. Beyond the calendar, certain events should trigger an immediate review: a leadership change, a significant new funding source, or a major program expansion. Policies that haven't kept pace with organizational growth create gaps that auditors — and fraudsters — notice quickly.

Best Practices for Stronger Nonprofit Financial Health

Diversify Revenue Streams

Over-reliance on a single funding source creates existential risk. When that grant ends or that major donor moves, organizations without diversification face immediate crisis. Nonprofits should aim to blend:

- Individual donations (major gifts, annual fund, planned giving)

- Government and foundation grants

- Corporate philanthropy and sponsorships

- Earned income (membership fees, program fees, social enterprise)

- Investment income

Equally important: balance restricted and unrestricted revenue. While restricted grants fund specific programs, unrestricted dollars provide the operational flexibility to respond to opportunities and challenges.

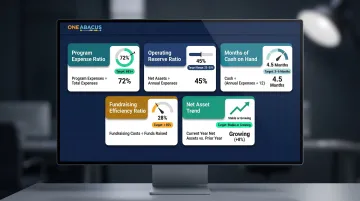

Track Key Financial Health Metrics

Nonprofit leaders should monitor these metrics regularly:

Program Expense Ratio BBB Wise Giving Alliance Standard 8 recommends spending at least 65% of total expenses on program activities. This demonstrates mission focus and efficient resource allocation.

Operating Reserve Ratio Unrestricted net assets divided by annual operating expenses. Target: 25%–50% of annual budget (3–6 months of operations). A declining ratio over time signals growing financial fragility.

Months of Cash on Hand Cash and cash equivalents divided by average monthly expenses. Shows liquidity and ability to weather short-term disruptions.

Fundraising Efficiency Ratio Fundraising expenses divided by total contributions raised. BBB Standard 9 recommends spending no more than 35% of related contributions on fundraising.

Net Asset Trend Track whether net assets are growing, stable, or declining over time. Consistent deficits signal unsustainable operations and warrant immediate board attention.

These metrics provide early warning signals and help boards make informed strategic decisions.

Practice Transparent Stakeholder Communication

Strong transparency practices include:

- Publishing annual reports accessible to the public

- Sharing financial dashboards directly with board members

- Providing narrative context alongside raw numbers — not just figures, but what they mean

This combination builds donor trust and strengthens fundraising outcomes. A 2025 study published in Humanities and Social Sciences Communications found that donor perception of nonprofit financial transparency was positively associated with donor trust (beta = 0.35, p < 0.001).

The fundraising case is equally clear: nonprofits with GuideStar Seals of Transparency raise significantly more than those without.

Maintain Audit Readiness Year-Round

Don't wait until audit season to scramble. Implement a monthly close checklist that includes:

- Reconciling all bank and credit card accounts

- Reviewing accounts receivable and payable aging

- Tracking restricted fund balances against actual expenses

- Documenting grant deliverables and compliance requirements

- Filing supporting documentation systematically

Year-round discipline prevents audit stress and catches errors when they're still fixable.

Invest in Purpose-Built Financial Systems

Generic accounting tools often fall short for nonprofits. Fund accounting, grant tracking, multi-program reporting, and donor restrictions require nonprofit-specific functionality. According to the Sage 2024 Nonprofit Technology Trends Survey, 85% of nonprofits use financial management and accounting software — but the right platform matters.

Platforms like NetSuite (with proper nonprofit configuration), Sage Intacct, and QuickBooks Online (for smaller organizations) can handle complex nonprofit needs when implemented correctly. The right system reduces manual workarounds, improves reporting accuracy, and frees your finance team to focus on strategy rather than spreadsheets.

When to Bring in Dedicated Financial Leadership

Warning Signs You've Outgrown Current Capacity

Several signals indicate a nonprofit needs stronger financial leadership:

- Cash flow surprises or frequent budget overruns

- Inability to produce timely reports for board meetings

- Difficulty managing multiple restricted grants simultaneously

- Preparing for your first independent audit

- Entering a period of rapid growth or program expansion

- Navigating a leadership transition (executive director, finance director, or board treasurer)

When any of these scenarios arise, the gap between your financial needs and current capacity has become a strategic risk.

The Fractional CFO Model

For many nonprofits, hiring a full-time CFO isn't financially feasible or operationally necessary. The fractional CFO model provides senior-level financial strategy at a fraction of the cost — typically 60–80% savings compared to a full-time hire, according to The Charity CFO.

What fractional CFOs deliver:

- Budget creation and rolling cash flow forecasts

- Board-ready financial reporting and analysis

- Audit preparation and compliance oversight

- Grant management and restricted fund tracking

- Strategic financial planning aligned with mission

- Accounting systems and process improvements

This model is particularly well-suited for nonprofits with revenue under $10 million, where current staff handles day-to-day operations but no one is steering big-picture financial strategy.

One Abacus Advisory's Approach

Lorin Port, Founder and Consulting CFO of One Abacus Advisory, brings over 25 years of finance and accounting experience — with the past nine years focused exclusively on nonprofits. Their fractional CFO and COO services provide executive-level financial and operational leadership tailored to each organization's size, stage, and mission needs.

Their client roster includes the San Diego Food Bank, Philadelphia Zoo, and Laguna Playhouse. When the Philadelphia Zoo faced simultaneous departures of their CFO and Controller, One Abacus stepped in to:

- Provide interim fractional CFO and Controller services

- Improve month-end close and board reporting processes

- Optimize their NetSuite environment for stronger reporting

- Support recruitment and onboarding of permanent financial leaders

That kind of rapid, targeted support is what makes the fractional model practical for nonprofits navigating transitions — you get the expertise when you need it, scaled back when you don't.

Frequently Asked Questions

How to manage finances for a nonprofit organization?

Strong nonprofit financial management combines accurate systems with consistent governance. Start with these foundations:

- Establish written financial policies

- Implement fund accounting to track restricted and unrestricted funds separately

- Produce regular financial statements and monitor cash flow closely

- Ensure board-level financial oversight

How to prepare a budget for a nonprofit organization?

Begin with prior-year actuals and current strategic goals, then break revenue by source (donations, grants, earned income) and expenses by functional category (program, administrative, fundraising). Build in realistic assumptions and schedule regular budget-to-actuals reviews throughout the year.

Are there non-profit financial advisors?

Yes. Nonprofit financial advisors include fractional CFOs who provide executive-level financial strategy, outsourced accounting firms that handle bookkeeping and reporting, and investment advisors who manage endowments. Organizations like One Abacus Advisory specialize in mission-focused financial leadership tailored specifically to nonprofit needs and compliance requirements.

What is the 33% rule for nonprofits?

The 33% rule relates to IRS public support requirements under Section 509(a)(1). Public charities must demonstrate that at least one-third of their support comes from the general public to maintain public charity status rather than being classified as a private foundation. Organizations receiving between 10%–33% may still qualify under a facts and circumstances test.

What is the 80 20 rule for nonprofits?

The 80/20 rule describes the pattern where roughly 80% of donations come from 20% of donors — a concentration that makes diversifying your donor base and revenue sources critical for long-term resilience. Some sector experts suggest the ratio has shifted closer to 90/10 as donor retention declines.

What are the 4 C's of financial management?

The 4 C's offer a practical (if informal) framework for nonprofit financial governance:

- Compliance — adhering to IRS and GAAP standards

- Control — internal controls to prevent fraud

- Commitment — organizational dedication to financial stewardship

- Communication — clear, transparent reporting to stakeholders