Introduction

The harsh reality facing the nonprofit sector: 36% of organizations ended 2024 with an operating deficit—the highest rate in a decade. More concerning, 52% hold three months or less of cash on hand. These aren't signs of mismanagement; they're symptoms of a deeper problem. Most nonprofit leaders understand budgets matter, yet many organizations still approach budgeting reactively: copying last year's spreadsheet, rushing before grant deadlines, or treating it as a compliance exercise rather than a strategic tool.

An effective annual operating budget does more than satisfy board requirements. It serves as your financial roadmap, aligning resources with mission priorities, enabling proactive decisions, and building reserves for long-term sustainability.

This guide covers what a nonprofit annual operating budget includes, proven methods for building one, and how to use it as a living document throughout the fiscal year.

TLDR:

- An annual operating budget projects all expected revenues and expenses for the fiscal year, serving as both resource allocation roadmap and financial benchmark

- Revenue forecasting should be conservative, organized by source (donations, grants, earned income), with restricted funds clearly identified

- Expenses follow functional categories (program, administrative, fundraising) that align with Form 990 and financial reporting standards

- Most nonprofits benefit from hybrid budgeting: incremental for baseline costs, zero-based for high-cost program areas

- Board approval is a fiduciary requirement; monthly budget-to-actual reviews catch variances before they become crises

What Is a Nonprofit Annual Operating Budget (and Why It Matters)

A nonprofit annual operating budget is a fiscal-year financial plan that projects all expected revenues and expenses, serving as both a roadmap for resource allocation and a benchmark for ongoing financial decision-making. Unlike for-profit budgets focused on profit maximization, nonprofit operating budgets center on mission delivery and sustainability.

The annual operating budget differs from other nonprofit budget types:

- Operating budget: The master financial plan covering all organizational activities

- Program budgets: Detailed plans for specific initiatives or departments

- Grant proposal budgets: Project-specific budgets tailored to funder requirements

- Capital budgets: Multi-year plans for major asset purchases or construction

- Campaign budgets: Focused plans for fundraising initiatives

All other budgets should align with and roll up into the operating budget.

The Surplus Myth: Why Breaking Even Isn't the Goal

Many nonprofit leaders assume their budgets must break even. In practice, the IRS permits 501(c)(3) organizations to generate surplus revenue. The restriction applies to distributing net earnings to private individuals (the "nondistribution constraint") — not to earning more than you spend. Surplus funds must be reinvested in the organization's exempt mission.

The National Council of Nonprofits explicitly states that break-even budgeting is actually the "biggest barrier" to building financial reserves. The Nonprofit Finance Fund identifies generating consistent surpluses as the first measure of financial health: "If the organization is not producing surpluses, it will have a difficult time building balance sheet strength (i.e., reserves)."

With 52% of nonprofits holding three months or less of operating cash, budgeting for a surplus is a matter of organizational survival. Two benchmarks worth targeting:

- Annual surplus: 3–5% of total budget to steadily build reserves

- Reserve goal: 3–6 months of operating expenses, with an emergency fund near 10% of total budget

Key Components of a Nonprofit Annual Operating Budget

Revenue Side: Conservative Forecasting by Source

The revenue section projects income from all sources, organized by category. Understanding revenue composition is critical: Giving USA 2025 reports individuals contributed $392.45 billion (66% of total charitable giving), while IRS data shows 71% of public charity revenue actually comes from program service fees—earned income, not donations.

Five primary nonprofit revenue categories:

Individual donations (contributed income)

- Annual fund gifts, recurring donors

- Major gifts and planned giving

- In-kind contributions (goods, services, volunteer time)

Corporate philanthropy

- Corporate sponsorships and underwriting

- Matching gift programs

- Corporate foundation grants

Earned income (program service revenue)

- Fees for service, membership dues

- Tuition, admission fees, patient charges

- Merchandise sales, facility rentals

Investment income

- Endowment interest and dividends

- Bond income, realized gains

- Board-designated investment funds

Grants (government and foundation)

- Federal, state, and local government grants

- Private foundation awards

- Community foundation grants

Conservative revenue forecasting is essential. Estimate each source separately using historical trends and known commitments only. Don't count unconfirmed pledges, speculative grants, or projected growth without solid justification.

The Council of Nonprofits recommends forecasting contributed revenue separately from earned revenue, since contributed income requires active forecasting rather than static budgeting based on contracts or fee schedules.

Expense Side: Functional Categorization

FASB Accounting Standards Codification Topic 958 requires all nonprofits to present expenses by functional category in their financial statements. IRS Form 990 mandates the same structure. Your budget should follow this framework from the start.

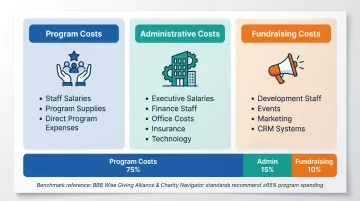

Three functional expense categories:

Program costs (direct mission delivery)

- Salaries and benefits for program staff

- Program supplies and materials

- Direct program expenses (rent, utilities, travel)

- Program-specific consultants and contractors

Administrative/management costs

- Executive leadership salaries

- Finance and accounting staff

- General office rent and utilities

- Insurance, legal, audit fees

- Technology and software subscriptions

- Board expenses

Fundraising costs

- Development staff salaries

- Fundraising event production

- Marketing and communications

- Donor database and CRM systems

- Consulting fees for campaign support

Functional vs. Natural Expenses

Natural expenses describe what was purchased (salaries, rent, supplies, travel). Functional expenses describe why it was purchased — for programs, administration, or fundraising.

During budget planning, you'll naturally think in natural categories: "What will rent cost?" Your final budget document, however, should present expenses by function to align with Form 990 reporting and standard nonprofit financial statements.

Many expenses must be allocated across functions using reasonable methods. For example, if your executive director spends 60% of time on programs, 30% on administration, and 10% on fundraising, split their salary accordingly.

Understanding Overhead Ratios

Overhead (administrative + fundraising costs) is often misunderstood as waste. In reality, some overhead is essential for organizational effectiveness.

Key evaluator benchmarks (not legal mandates):

- BBB Wise Giving Alliance Standard 8: at least 65% of expenses must go to programs

- Charity Navigator: perfect scores at 85% program spending for medium/large donor-funded organizations, 70% for small organizations, and 65% for museums

The right ratio depends on your organization's size, mission, and stage. In 2014, GuideStar, Charity Navigator, and BBB Wise Giving Alliance jointly urged donors to "help crush the false notion that overhead ratios serve as the sole basis for trusting a charity." The 2009 Stanford Social Innovation Review article "The Nonprofit Starvation Cycle" documented how systematically underfunding organizational capacity harms mission delivery.

Budget adequate capacity. Underfunding overhead doesn't protect your mission — it quietly erodes your ability to deliver it.

Commonly Underestimated Budget Lines

Nonprofits frequently omit or underbudget:

- Capacity building: Staff training, professional development, strategic planning

- Technology: Software subscriptions, CRM systems, cybersecurity

- Contracted services: Accounting, legal, HR consulting, IT support

- Insurance: D&O, general liability, cyber liability

- Contingency reserve: 3-5% of total budget for unexpected costs

A contingency line signals financial maturity, not imprecision. Unplanned costs will arise every year — the only variable is whether you planned for them.

Fund Accounting Considerations

FASB ASU 2016-14 simplified net asset classifications from three categories to two:

- Net assets without donor restrictions (formerly "unrestricted")

- Net assets with donor restrictions (formerly "temporarily" and "permanently" restricted)

Your operating budget should clearly identify which revenues carry donor restrictions. Restricted funds cannot be used for general operations unless the restrictions are satisfied.

Focus operational planning on revenue without restrictions: unrestricted gifts, earned income, and released restricted funds available for current-year spending.

Approximately 77% of nonprofits manage restricted funds. Don't mix restricted and unrestricted revenue in your budget projections—it creates false confidence in available resources.

Nonprofit Budgeting Methods: Which Approach Fits Your Organization

The budgeting method you choose affects accuracy, staff buy-in, and how well your budget reflects actual organizational priorities. The right approach depends on your size, financial capacity, and where you are in your growth cycle.

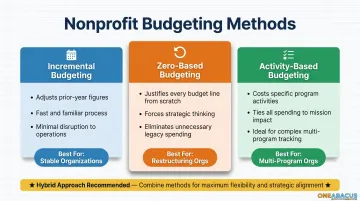

Incremental Budgeting

This method uses the prior year's budget as a baseline, then adjusts line items by a percentage or fixed amount.

Pros:

- Fast and familiar

- Low staff resistance

- Minimal documentation required

- Easy board understanding

Cons:

- Perpetuates historical inefficiencies

- Doesn't challenge whether spending aligns with current priorities

- Can lead to "use it or lose it" mentality

- Misses opportunities to reallocate resources

Best for: Stable organizations with predictable revenue and established programs.

Zero-Based Budgeting (ZBB)

Every expense line must be justified from zero each cycle, regardless of what was approved the year before.

Pros:

- Forces strategic thinking about every dollar

- Eliminates legacy spending that no longer serves mission

- Aligns resources directly with current priorities

- Reveals hidden inefficiencies

Cons:

- Can take 2–3x longer than incremental budgeting

- Can create staff anxiety and political friction

- Requires strong financial leadership

- May be impractical for small teams

Best for: Organizational restructuring, new leadership taking over, cost-reduction initiatives, or when prior budgets clearly misalign with strategy.

Activity-Based Budgeting (ABB)

This approach builds the budget by estimating the cost of each specific program activity or organizational output.

Pros:

- Ties spending directly to mission delivery

- Supports program cost analysis and ROI measurement

- Particularly useful for multiple programs or grant-funded work

- Enables clear communication about program costs

Cons:

- Requires detailed activity tracking

- Can be complex for organizations with overlapping activities

- Needs strong program-finance collaboration

Best for: Nonprofits with multiple distinct programs, significant grant funding requiring project-level budgets, or organizations seeking to evaluate program efficiency.

Choosing Your Method

Most nonprofits benefit from a hybrid approach: use incremental budgeting as a starting point for administrative functions and stable programs, then apply zero-based principles selectively to high-cost areas, underperforming programs, or new initiatives. If your team is small or your finance function is lean, start with incremental budgeting — then layer in zero-based or activity-based analysis for the programs where resources are most contested or outcomes are hardest to justify.

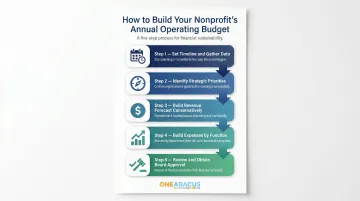

How to Build Your Nonprofit's Annual Operating Budget Step by Step

Step 1: Set Timeline and Gather Historical Data

Begin the budgeting process 2-3 months before the fiscal year starts. Propel Nonprofits recommends at least three months to ensure board approval before the new year begins.

Pull this historical data:

- Prior-year actual revenues and expenses

- Most recent budget-to-actual comparison report

- Financial statements (statement of activities, balance sheet)

- Program performance data

- Grant commitments and pipeline

Identify significant variances between budget and actuals. Understand what drove them—one-time events, overly optimistic projections, program changes, or external factors. These insights form the foundation for realistic projections.

Step 2: Identify Strategic Priorities and Programmatic Changes

Before projecting numbers, confirm organizational goals for the coming year with leadership and program staff. Strategy should drive the numbers — not the other way around.

Key questions to address:

- What are our programmatic priorities?

- Are we launching new programs or sunsetting old ones?

- Do we anticipate staffing changes?

- Are capital purchases or technology investments planned?

- What revenue diversification efforts are underway?

Document these priorities before opening a spreadsheet. Budget allocations made without strategic context often misrepresent where resources are actually needed.

Step 3: Build Revenue Forecast Conservatively

Estimate each revenue source separately using realistic growth assumptions based on historical trends and known commitments only.

For individual donations:

- Analyze donor retention rates and average gift size

- Count only confirmed major gifts

- Apply conservative growth rates (3-5% for established programs)

For grants:

- Include only awarded grants or those with formal commitments

- Don't budget speculative grant applications

- Note restrictions and release schedules

For earned income:

- Base projections on signed contracts or historical utilization rates

- Factor in seasonality and capacity constraints

For special events:

- Use conservative attendance and sponsorship projections

- Account for all direct costs

Note that 84% of nonprofits receiving government funding expected cuts in 2025. Don't assume government grants will renew at prior levels without confirmation. Build a contingency scenario with reduced government funding to stress-test your revenue assumptions before finalizing projections.

Step 4: Build Expenses by Function and Department

Allocate costs at the department or program level first, then roll up into functional categories (program, administrative, fundraising).

Key considerations:

- Inflation: Factor 3-5% increases for vendor contracts

- Salaries: Include cost-of-living adjustments and planned merit increases

- Benefits: Budget 25-35% of salaries for benefits and payroll taxes

- New tools or services: Add specific line items for planned investments

- Contingency: Include 3-5% reserve line

For shared costs (rent, utilities, technology), use reasonable allocation methods based on staff time, square footage, or usage metrics.

Step 5: Review, Reconcile, and Obtain Board Approval

Present a draft to the finance committee before full board review. The finance committee should scrutinize:

- Revenue-to-expense gap (surplus or deficit position)

- Program-to-overhead ratio relative to organizational benchmarks

- Alignment with strategic plan

- Major variances from prior year

- Contingency adequacy

- Cash flow implications

BoardSource identifies board budget approval as a core fiduciary responsibility. BBB Wise Giving Alliance Standard 14 and Charity Navigator both require annual board approval of the operating budget as a governance indicator.

This isn't a formality—it's a legal duty of care. For nonprofits without a dedicated CFO, this is also where gaps in financial leadership become most visible. Fractional CFO support — like the kind One Abacus Advisory has provided to organizations such as the Philadelphia Zoo during leadership transitions — can help ensure the board receives clear, complete financial analysis rather than a draft budget that raises more questions than it answers.

How to Monitor and Manage Your Budget Throughout the Year

A budget is a living document, not a one-time exercise. Establish a regular review cadence:

- Finance staff: Monthly budget-to-actual review

- Finance committee: Quarterly detailed review

- Full board: Quarterly summary reporting

Key Reporting Tools

Three reports form the core of ongoing budget oversight:

- Budget-to-actual comparisons — show projected versus actual revenue and expenses line by line, with variance columns in both dollar and percentage terms

- Cash flow statements — track timing of cash in and out, revealing liquidity issues that budget-to-actual reports miss

- Treasurer reports — should highlight significant variances, year-to-date performance, and any concerns requiring board attention

The New York State Attorney General recommends comparing actual receipts and expenditures to budget at least quarterly, preferably monthly, with timely explanations of variances.

That consistent monitoring is what makes the next step possible: knowing when the numbers have shifted enough to warrant a formal change.

When to Amend the Budget

Significant variances (typically 10% or more) should trigger a formal conversation about whether to amend the budget or adjust operations.

Appropriate reasons to amend include:

- Major revenue loss (large grant declined, government funding cut)

- Unexpected capital expense or emergency cost

- Board-approved program expansion or new initiative

- Windfall gift that changes organizational capacity

Budget amendments should go through the same approval process as the original budget—finance committee review followed by full board approval. Document the reasons and update the budget accordingly.

Who Owns the Nonprofit Budget: Roles and Governance

Internal Roles and Responsibilities

Budget creation is typically led by a cross-functional team:

- CFO or Controller (or fractional CFO) — overall budget development and coordination

- Program directors — department-level expense planning and revenue projections

- Development staff — fundraising revenue forecasting

- Executive director — strategic oversight and final internal approval

The executive director coordinates inputs but doesn't create the budget alone. Effective budgeting requires cross-functional collaboration.

Board Fiduciary Duty

Board members have a legal duty of care that includes reviewing and approving the annual budget. They're not responsible for creating it, but they're accountable for ensuring it aligns with mission and fiscal responsibilities.

Board members should ask substantive questions during review:

- How conservative are revenue assumptions?

- What happens if key funding doesn't materialize?

- Are program costs adequately supported?

- Does overhead support organizational effectiveness?

- What reserves are we building?

Approximately 54% of nonprofits have independent audit committees that often take lead responsibility for budget review before full board consideration.

The Growing Role of Fractional Financial Leadership

Small-to-mid-size nonprofits typically lack capacity for full-time CFOs. Organizations with revenue under $500K rely 62% on volunteer or part-time finance staff, and even those up to $3 million often have just one or two finance staff handling all functions.

The budgeting process demands CFO-level expertise: strategic thinking, financial modeling, board communication, and technical accounting knowledge. That gap creates real risk — budgets built without adequate financial leadership often contain unrealistic assumptions, misclassified expenses, or compliance issues.

One Abacus Advisory works with nonprofits to fill exactly this gap. A fractional CFO can lead the entire annual budget process, bring strategic financial perspective, and support board-level reporting — without the cost of a full-time hire.

For example, during the Philadelphia Zoo's leadership transition when both their CFO and Controller departed, One Abacus Advisory provided fractional CFO support that stabilized operations, improved budgeting and reporting systems, and ensured the board maintained confidence in financial results throughout a critical period.

Frequently Asked Questions

Who is responsible for creating a nonprofit's annual operating budget?

Budget creation is typically led by the CFO, controller, or fractional CFO, with input from program directors and development staff. The finance committee reviews the draft before the full board formally approves it as part of their fiduciary oversight responsibility.

What are the main components of an annual operating budget for a nonprofit?

The budget has two primary sides: revenue and expenses. Revenue is organized by source — individual donations, grants, earned income, corporate philanthropy, and investment income. Expenses are organized by function: program costs, administrative costs, and fundraising costs.

What financial models and budgeting methods do nonprofits use?

The three core methods are:

- Incremental budgeting — adjusting prior-year figures by a set percentage

- Zero-based budgeting — justifying every expense from scratch

- Activity-based budgeting — costing specific program activities

Most nonprofits use a hybrid approach, applying incremental methods to stable areas and zero-based principles to high-cost or strategic functions.

Is a 501(c)(3) nonprofit required to have an annual budget?

No federal law explicitly requires it. However, most state governance guidance, grant funders, and board best practices treat an approved annual budget as a fundamental fiduciary requirement. Evaluators like BBB Wise Giving Alliance and Charity Navigator include budget approval in their governance standards, and grantmakers routinely request it.

What are common budget allocation rules for nonprofits (e.g., 80/20, 33%, 50/30/20)?

Common benchmarks suggest allocating at least 65-80% of spending to programs and no more than 20-35% to overhead (admin + fundraising). However, these are evaluator guidelines, not legal mandates. The appropriate allocation depends on your organization's mission, size, and developmental stage—and evaluator standards vary significantly based on these factors.

What does capacity building mean for nonprofits and what can their capacity-building budget be used for?

Capacity building refers to investments that strengthen long-term organizational infrastructure and effectiveness. Common uses include staff training, technology upgrades, strategic planning processes, leadership development, and outcomes measurement systems.