This guide walks through the four core financial statements every nonprofit must review, internal controls that prevent fraud, reporting obligations across four audiences, warning signs that infrastructure is failing, and a practical step-by-step review framework. Whether you're preparing for an audit, navigating growth, or rebuilding after leadership turnover, you'll find the clarity needed to strengthen your financial foundation.

TLDR:

- Nonprofit financial infrastructure encompasses accounting systems, internal controls, reporting tools, and governance structures that manage money and support strategic decisions

- The four GAAP-required statements—Statement of Financial Position, Statement of Activities, Statement of Cash Flows, and Statement of Functional Expenses—form the diagnostic foundation of any infrastructure review

- 35% of nonprofit fraud cases occur due to missing internal controls, with segregation of duties being the most critical safeguard

- 52% of nonprofits hold three months or less of cash reserves, and 36% ended 2024 with operating deficits—the highest rate in 10 years

What Is Nonprofit Financial Infrastructure?

Nonprofit financial infrastructure is the complete system of practices, controls, reporting tools, technology, and governance structures that sustain financial health. It's not just accounting records—it's how money flows through the organization, who oversees transactions, and how decisions get made. The infrastructure includes fund accounting software, written financial policies, board oversight protocols, bank reconciliation procedures, and grant compliance tracking systems.

Why Nonprofits Are Different

Nonprofits operate under financial constraints that set them apart from for-profit businesses. Three core obligations shape every dollar:

- Fund accounting: Donor-restricted funds must be tracked separately from unrestricted resources, categorizing every dollar by purpose and restriction

- Form 990 compliance: Public transparency requirements that go well beyond what corporate filings demand

- Program-expense accountability: Demonstrating to funders, watchdogs, and the IRS that at least 65% of expenses support programs rather than overhead

Unlike businesses measuring profit margins, nonprofits track net asset balances by restriction category (with donor restrictions versus without donor restrictions). Revenue recognition follows specialized GAAP rules (FASB ASC 958) that differ from commercial accounting. These distinctions are embedded in nonprofit law and funder expectations—they're not negotiable.

Infrastructure as Competitive Advantage

Organizations with strong financial infrastructure attract more grant funding, retain key staff, and make faster strategic decisions. Funders conduct due diligence before awarding grants, scrutinizing audited financial statements, Form 990 filings, and internal control documentation. According to Independent Sector research, trust in nonprofits stands at only 57%—meaning 43% of Americans don't fully trust the sector. Clean, transparent financial reporting directly addresses this trust gap.

Weak infrastructure creates hidden vulnerabilities. The ACFE 2020 Report found that 35% of nonprofit fraud cases occur because basic internal controls are absent. These failures typically surface at the worst possible moment: when auditors issue management letters, funders freeze disbursements, or the organization can't make payroll despite showing a surplus on paper.

The Four Core Financial Statements Nonprofits Must Review

FASB ASC 958 requires nonprofits to produce four financial statements that together tell the complete story of organizational health. Each serves a distinct diagnostic purpose, and boards must understand all four, not just the Statement of Activities.

Statement of Financial Position (Balance Sheet)

This snapshot document shows assets, liabilities, and net assets at a specific point in time. The core formula: Assets – Liabilities = Net Assets. Review two critical categories:

- Net assets without donor restrictions: Available for any mission-aligned purpose, including operating expenses and emergency reserves

- Net assets with donor restrictions: Legally bound to specific programs, time periods, or endowment requirements

Organizations must maintain sufficient unrestricted net assets to sustain operations during funding gaps. The NFF 2025 Survey of 2,206 nonprofits found that 52% have three months or less of cash on hand. A healthy balance sheet shows unrestricted reserves equal to 3-6 months of operating expenses—25% or higher as an operating reserve ratio.

Statement of Activities

The nonprofit equivalent of an income statement, this document tracks revenue and expenses over a reporting period (monthly, quarterly, or annually). Revenue sources include donations, grants, program fees, and investment returns. Expenses break into three functional categories: program services, administrative costs, and fundraising.

The resulting surplus or deficit equals the change in net assets, the primary indicator of whether the organization lives within its means. The NFF 2025 Survey revealed that 36% of nonprofits ended 2024 with an operating deficit, the highest rate in 10 years of survey data. Persistent deficits erode net assets and eventually threaten organizational survival.

Statement of Cash Flows

Cash flow tracking reveals whether the organization can meet near-term obligations even when the Statement of Activities looks healthy. It categorizes cash movement into three activities:

- Operating activities: Cash from donations, grants, and program revenue minus cash spent on salaries, rent, and supplies

- Investing activities: Purchase or sale of fixed assets and investments

- Financing activities: Loans received or repaid, lines of credit drawn

Timing gaps within each category expose a common risk for grant-dependent organizations. Reimbursement-based grants require nonprofits to front costs and wait 30, 60, or 90 days for reimbursement — a pattern that can produce a cash crisis even when the Statement of Activities shows a surplus. According to The Charity CFO, successful nonprofits aim for at least 50% of total revenue from unrestricted sources to maintain liquidity.

Statement of Functional Expenses

FASB ASU 2016-14, effective for fiscal years beginning after December 15, 2017, extended this statement requirement to all nonprofits (previously only mandatory for voluntary health and welfare organizations). It breaks expenses down two ways:

| Expense Type | Program Services | Administrative | Fundraising |

|---|---|---|---|

| Salaries & Benefits | $X | $X | $X |

| Rent & Occupancy | $X | $X | $X |

| Professional Fees | $X | $X | $X |

| Supplies & Materials | $X | $X | $X |

Watchdog agencies scrutinize this statement closely. BBB Wise Giving Alliance requires at least 65% of expenses on programs and no more than 35% on fundraising. Charity Navigator evaluates the Programs Expense Ratio, Working Capital, and Fundraising Efficiency. Nonprofits that allocate shared costs accurately across functions — rather than dumping everything into administration — consistently score better on these evaluations and present a stronger case to major donors.

Internal Controls and Financial Processes: The Backbone of Accountability

Internal controls are written policies and operational procedures that prevent errors, detect fraud, and ensure financial data integrity. The ACFE 2020 Report identified the top control weaknesses enabling nonprofit fraud: lack of internal controls (35%), lack of management review (19%), and override of existing controls (14%). Insufficient controls are among the most common audit findings and the primary vulnerability exploited in internal fraud cases.

Segregation of Financial Duties

The single most important control is separation of duties. No single person should control a complete financial transaction from start to finish. Basic separations include:

- The person who approves expenses should not sign checks

- The person handling receipts should not reconcile bank statements

- The payroll preparer should not distribute paychecks

- The person logging incoming donations should not deposit them

For small nonprofits with limited staff, the National Council of Nonprofits recommends compensating controls: conduct surprise internal audits, require two signatures on all checks, and have a non-bookkeeper board member review monthly bank statements.

Bank Reconciliation and Disbursement Controls

Monthly bank reconciliation is the foundation of financial accuracy. Review these elements:

- Beginning balances carry forward correctly from month to month without unexplained adjustments

- Deposits on financial reports match bank statements exactly—no timing differences lasting more than 30 days

- All disbursements are supported by invoices and pre-approved against the budget by someone other than the check signer

- At least one non-signatory officer reviews monthly bank statements for unauthorized transactions

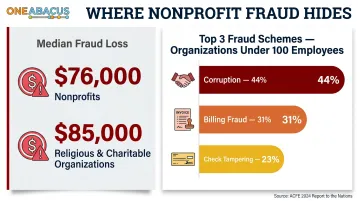

The ACFE 2024 Report found median fraud losses of $76,000 for nonprofits and $85,000 for religious/charitable organizations. For organizations under 100 employees, the most common schemes are corruption (44%), billing fraud (31%), and check tampering (23%). Consistent reconciliation and disbursement controls are what catch these schemes early — before losses compound.

Accounting Systems and Technology

Assess whether accounting software supports fund accounting, multi-program tracking, and grant reporting. Warning signs the system has been outgrown:

- Excessive manual workarounds to produce financial reports

- Delayed reporting—monthly statements arrive 4-6 weeks after month-end

- Inability to generate restricted/unrestricted breakdowns automatically

- Staff frequently working around the system rather than within it

When these warning signs appear, the accounting system is creating risk, not reducing it. Platforms built for nonprofit complexity — such as NetSuite — automate fund accounting, support real-time grant tracking, and eliminate the manual workarounds that introduce errors. That matters most during growth phases or when restricted grant volume increases.

A fractional CFO can assess whether a system change is warranted, manage implementation, and train staff — without the overhead of a full-time hire.

Sound accounting systems also depend on what happens to records after transactions close. Retention policies must specify what to keep, how long, and who's responsible. According to 501 Commons and IRS guidance:

| Retention Period | Document Types |

|---|---|

| 3 years | Bank reconciliations, deposit slips, general correspondence |

| 7 years | Invoices, payroll records, personnel files (terminated), timesheets, contracts |

| Permanently | Audit reports, financial statements, bylaws, IRS determination letter, Form 990s, board minutes |

Financial Reporting: Board Oversight, IRS Compliance, and External Transparency

Nonprofit financial reporting serves four distinct audiences: internal management, the Board of Directors, the IRS, and external stakeholders. Each requires different information at different frequencies.

Internal Budget-to-Actual Reporting

Management should compare actual revenue and expenses against the approved annual budget monthly, investigating significant variances and course-correcting in real time. Key questions:

- Which revenue sources are underperforming?

- Where are expenses trending over budget?

- Are financial assumptions from the budget still valid?

Budget-to-actual reports keep leadership ahead of problems. Waiting until quarter-end or year-end to review performance eliminates any real opportunity to adjust course.

Board Financial Reporting

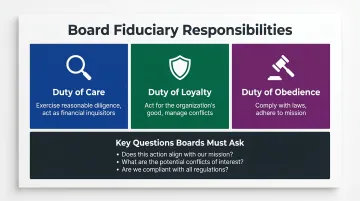

Boards must review the Statement of Financial Position, Statement of Activities (with budget-to-actual comparison), and cash position at every meeting. Annually, the board should also review audited financial statements and Form 990 before filing. This is a fiduciary obligation, not optional.

According to BoardSource, board members exercise three fiduciary duties:

- Duty of Care: Exercise reasonable care and due diligence, act as "financial inquisitors"

- Duty of Loyalty: Act for the organization's good, manage conflicts of interest

- Duty of Obedience: Comply with laws and adhere to mission

Board members need not be financial experts, but they must ask informed questions:

- Why did cash decrease while net assets increased?

- How many months of operating reserves do we hold?

- Are restricted funds being spent according to donor agreements?

IRS Form 990 and External Stakeholder Reporting

Form 990 serves two purposes: regulatory compliance and public transparency. Foundation program officers read Part III (Program Service Accomplishments), Part VI (Governance), and Part IX (Functional Expenses) before funding decisions. With nonprofit trust at only 57%, the 990 functions as a credibility document.

Filing requirements based on gross receipts and assets:

| Form | Gross Receipts | Total Assets | Filing Deadline |

|---|---|---|---|

| 990-N (e-Postcard) | ≤ $50,000 | N/A | 15th day of 5th month after fiscal year-end |

| 990-EZ | < $200,000 | < $500,000 | 15th day of 5th month after fiscal year-end |

| 990 (Full) | ≥ $200,000 | ≥ $500,000 | 15th day of 5th month after fiscal year-end |

Organizations that fail to file for three consecutive years automatically lose tax-exempt status and must reapply, paying applicable fees. Inaccurate or incomplete 990s damage credibility and disqualify organizations from major funding.

External reporting obligations extend beyond the IRS. Most large funders require audited financial statements, annual impact reports, and grant compliance documentation. Nonprofits with revenue over $2 million require audited financial statements; those between $1–2 million generally need reviews or compilations.

Warning Signs Your Financial Infrastructure Is Falling Behind

Financial infrastructure deteriorates gradually, then fails suddenly. Watch for these indicators.

Operational Warning Signs

These internal warning signs suggest your systems, processes, or staffing no longer match your organization's complexity:

- Financial reports arrive 30+ days after month-end, consistently

- Staff spend significant manual effort just to produce financial statements

- Leadership can't quickly answer basic questions: How much cash on hand? What's the restricted fund balance? How is each program performing financially?

- Staff regularly work around accounting systems rather than within them

Governance and Compliance Warning Signs

Boards and executive directors should monitor:

- Growing debt balances or continued declines in cash reserves

- Borrowing from operating reserves to cover payroll or vendor payments

- Continued budget overruns with no corrective action

- Inability to produce clean financial statements for auditors or funders on deadline

- Increasing audit findings or management letter comments year over year

The NFF 2025 Survey found that 52% of nonprofits have three months or less of cash on hand and 18% have one month or less. Falling below the 3-6 month benchmark leaves almost no buffer when a major funder is late or an unexpected expense hits.

Growth-Trigger Warning Signs

Growth is the most common reason infrastructure falls out of alignment. When nonprofits expand programs, add staff, or win significant new grants, systems that worked well enough before start breaking down:

- More staff means more complex payroll and cost allocation requirements

- More grants mean more restricted fund tracking and compliance reporting

- More programs mean more detailed functional expense reporting

The NFF 2025 data shows 63% of organizations expanded programs in 2024 despite financial pressures. Reimbursement-based grants create an immediate problem: staff, facilities, and supplies are paid up front while grant reimbursements arrive weeks or months later.

Those timing gaps drain working capital repeatedly — even when the Statement of Activities (your income statement) shows a surplus on paper. Revenue recognized doesn't mean cash received.

How to Conduct Your Annual Financial Infrastructure Review

An annual infrastructure review ensures controls remain effective, compliance obligations are met, and systems match organizational needs. Follow this three-phase framework.

Phase 1: Document Gathering

Collect these materials before beginning the review:

- All written financial policies (expense reimbursement, authorization limits, disbursement approval, conflict of interest)

- Most recent Form 990 and audited financial statements

- Budget-to-actual reports for the full fiscal year

- Bank reconciliations for all accounts (checking, savings, investment)

- List of authorized check signatories and online banking access

- Documentation of all donor-restricted fund balances and spending requirements

- Grant award letters and compliance requirements for all active grants

This document set forms the review foundation. Missing documents themselves indicate infrastructure gaps.

Phase 2: Core Review Process

Work through these verification steps systematically:

EIN Consistency: Verify the Employer Identification Number matches across all bank accounts, tax filings, and donor communications. According to the IRS, the EIN must be used consistently for all employment tax returns and statements.

Segregation of Duties Test: Confirm separation of duties is practiced, not just written in policy. Map who approves purchases, who signs checks, who enters transactions, who reconciles accounts, and who reviews reports. Identify any person controlling more than one step in a transaction cycle.

Bank Reconciliation Spot-Check: Pull three random months of bank reconciliations. Verify beginning balances carry forward, all deposits clear within 30 days, outstanding checks are followed up, and a non-signatory reviews the reconciliation.

Disbursement Documentation: Select 15-20 disbursements at random. Confirm each is supported by an invoice, approved against the budget in writing, and authorized by someone other than the check signer.

Restricted Fund Compliance: List all donor-restricted funds. Verify spending matches donor agreements—no restricted education grant dollars paying for general operating expenses.

Reporting Timeline Compliance: Assess whether financial reports are generated and distributed per board policy timelines. Monthly reports should reach leadership within 15-20 days of month-end; board packets should arrive 5-7 days before meetings.

Phase 3: Translate Findings Into Action

Categorize issues by severity:

- Immediate compliance risk: Missing segregation of duties, inaccurate Form 990 data, restricted funds spent incorrectly—address within 30 days

- Governance gap: Late financial reports, incomplete board review, unclear authorization policies—address within 90 days

- Operational inefficiency: Manual workarounds, outdated software, delayed reconciliations—address within 6-12 months

Assign responsibility for each corrective action, set resolution timelines, and document findings in a formal report for board review.

Some findings—persistent infrastructure gaps, systemic reporting failures, or unclear financial leadership—go beyond what internal staff can resolve alone. In those cases, fractional CFO support provides the strategic oversight needed to rebuild financial infrastructure that fits the organization's actual size and stage.

Fractional CFO engagements typically range from $3,000 to $12,000 per month according to Kyle David Group, a fraction of the salary-plus-benefits cost of a full-time CFO. For nonprofits under $15 million in revenue, firms like One Abacus Advisory offer that executive-level financial leadership without the full-time overhead.

Frequently Asked Questions

What is nonprofit financial infrastructure?

Nonprofit financial infrastructure is the complete framework of systems, processes, controls, and reporting structures that manage an organization's financial resources—covering accounting software, internal controls, financial statements, budgeting, and governance oversight. It ensures money flows correctly and that decisions are grounded in accurate data.

How often should a nonprofit conduct a financial infrastructure review?

An internal financial review should occur at least annually, ideally aligned with fiscal year-end. Key components like budget-to-actual tracking should be reviewed monthly, and board-level financial statements should be reviewed at every board meeting to maintain oversight and catch problems early.

What are the warning signs that a nonprofit's financial infrastructure is inadequate?

The most common indicators are late or inaccurate financial reports, inability to track restricted versus unrestricted funds accurately, repeated audit findings, and leadership making decisions without timely financial data. If staff regularly work around systems or reports require weeks of manual effort, infrastructure has fallen behind organizational needs.

What internal controls are most critical for small nonprofits?

Segregation of duties is the most essential control—specifically ensuring no single person controls both transaction approval and check signing. Pair this with monthly bank reconciliation reviewed by a non-signatory and annual review by an independent audit committee. Even small organizations can implement compensating controls when staff size limits full separation.

Does a nonprofit need a full-time CFO to maintain strong financial infrastructure?

Most small to mid-sized nonprofits can maintain strong financial infrastructure through a fractional CFO arrangement—senior-level financial leadership and strategic oversight at a fraction of the cost of a full-time hire. This model works well for organizations that are growing, preparing for audits, or navigating leadership transitions.

How does financial infrastructure affect a nonprofit's ability to secure grants?

Most major funders require audited financial statements, accurate Form 990 filings, and demonstrated grant compliance capacity before awarding funds. Organizations with weak infrastructure are frequently disqualified during due diligence or required to return funds after grant audits.