Introduction

Nonprofits face a cash flow challenge that for-profit businesses rarely encounter: bills don't pause while grant payments are delayed, donations slow during off-seasons, and restricted funds sit untouchable in the bank.

Unlike businesses with predictable sales cycles, nonprofits depend on irregular income streams — donations that spike in December, government grants that reimburse months after expenses are paid, and foundation awards that arrive on schedules disconnected from operational needs.

That timing mismatch has real consequences. 36% of nonprofits ended 2024 with an operating deficit — the highest rate in 10 years, according to the Nonprofit Finance Fund's 2025 survey. Even organizations with healthy annual budgets can find themselves unable to make payroll when cash doesn't arrive in sync with expenses.

This guide walks through the tools and strategies nonprofit leaders need: reading cash flow statements, building monthly forecasts, smoothing out inflow and outflow timing, managing restricted funds, and recognizing when outside financial expertise can prevent a crisis.

Key Takeaways

- Nonprofits face irregular income cycles, grant timing delays, and restricted fund limitations that create unique cash flow volatility

- Monthly cash flow forecasting — mapping your budget against actual receipt timing — is the most effective tool for avoiding shortfalls

- Diversify revenue, maintain 3-6 months in operating reserves, and track restricted funds separately

- Nonprofits without a full-time CFO can close the gap with fractional financial leadership, gaining strategic oversight without the overhead

Why Nonprofit Cash Flow Is Uniquely Challenging

Unlike businesses that generate predictable sales, nonprofits depend on donations, grants, and program fees — each with unpredictable timing. This creates structural mismatches between when money arrives and when expenses must be paid.

The grant disbursement gap is particularly painful. Grants are often awarded months before funds are released, yet operating costs continue. 27% of nonprofits reported delays, pauses, or freezes in government funding in early 2025, according to the Urban Institute. For organizations experiencing disruptions, government funding represented 42% of their total revenue. Reimbursement-based contracts deepen the gap: expenses must be paid upfront, then documented and submitted for payment weeks or months later.

Restricted vs. unrestricted funds create a hidden trap. Restricted funds can only be used for designated purposes, meaning a nonprofit may technically have cash on hand that it legally cannot use to cover payroll or rent. This is a cash flow challenge unique to the sector. An organization with $200,000 in the bank might have only $15,000 available for operations if the rest is restricted to a capital campaign or specific program.

Seasonal swings add another layer of pressure. Approximately 30% of all annual giving occurs in December, with the average nonprofit raising 40% of annual online revenue in that month alone. December 31 alone accounts for 5% of total annual revenue. That Q4 surge is followed by lean summer months — a predictable cycle that still catches organizations off guard when there's no plan to bridge the gap.

Underneath all of this sits a compliance obligation that intensifies the stakes. Nonprofits must maintain financial transparency for boards, donors, and regulators. Cash flow mismanagement isn't just an operational problem — it triggers governance questions, erodes donor trust, and can jeopardize funding relationships that took years to build.

The Nonprofit Cash Flow Statement Explained

The nonprofit cash flow statement is a financial document required under GAAP that shows all inflows and outflows of cash over a specific period — typically monthly, quarterly, or annually. It differs from the Statement of Activities (the nonprofit equivalent of a P&L), which reports revenues and expenses on an accrual basis regardless of when cash moves.

The statement has three sections:

Operating Activities

Cash inflows from donations, grants, program fees, and membership dues; outflows from salaries, rent, utilities, and program expenses. This section shows whether the organization's core mission activities generate or consume cash.

Investing Activities

Cash flows related to buying or selling assets, property, or equipment; inflows from investment maturities or sales. A nonprofit purchasing new facilities or selling investments would report those transactions here.

Financing Activities

Cash inflows from loans or lines of credit; outflows from debt repayments. Restricted contributions for long-term purposes (like endowment gifts or building funds) are also reported in this section under current GAAP standards.

The Changes in Cash reconciliation at the bottom connects the beginning cash balance to the ending cash balance, helping leadership identify whether the organization is net cash positive or negative for the period.

Statement vs. projection: The cash flow statement is historical and backward-looking; the cash flow projection or forecast is forward-looking and the more actionable management tool. Both are necessary.

What to look for when reviewing: Leadership and boards should flag:

- Months where ending operating cash drops below a defined minimum

- Recurring shortfall patterns in specific months

- Whether restricted fund releases align with actual spending needs

How to Build a Monthly Cash Flow Forecast

The most effective forecasting approach starts during the annual budgeting process. Rather than spreading budget line items evenly across 12 months, nonprofits should assign each income and expense line item to the month when the cash will actually arrive or be spent.

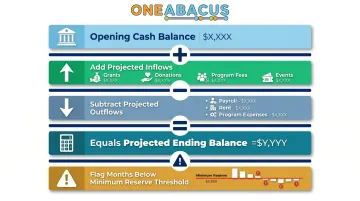

Structure of a monthly cash flow projection:

- Opening cash balance

- Add: Projected inflows by source and timing (grants, individual donations, program fees, events)

- Subtract: Projected outflows (payroll, rent, program expenses, overhead)

- Equals: Projected ending cash balance

- Flag months where balance drops below the organization's defined minimum

Include an "Other Cash Transactions" section to capture non-operating cash events: temporary draws from operating reserves, release of restricted funds from savings to checking, loan principal payments, and planned capital expenditures. When reserves must be temporarily used to cover a gap, show both the draw and the repayment explicitly — so the board can see exactly what happened and when the balance was restored.

Two practices make a forecast genuinely useful rather than just a planning exercise:

- Set a minimum cash balance threshold — typically four weeks of operating expenses — and flag any month where you project dipping below it. Acting in advance beats reacting to a shortfall.

- Update the forecast on a rolling basis. A static annual forecast loses accuracy fast. A 13-week or monthly refresh, paired with a brief flash report on revenue, payroll, and operational spending, keeps leadership current as conditions change.

Free tools are available: Propel Nonprofits offers a cash flow template and primer video, and the Wallace Foundation's StrongNonprofits Toolkit includes spreadsheet templates to translate an operating budget into a detailed cash flow projection.

Strategies to Strengthen Nonprofit Cash Flow

Diversify and Stabilize Revenue Streams

Relying on one or two revenue sources (like a single major grant) creates serious vulnerability. Diversifying across multiple streams smooths out income timing and reduces over-reliance on any single source:

- Individual donations

- Corporate sponsorships

- Program fees

- Recurring giving programs

- Government and private grants

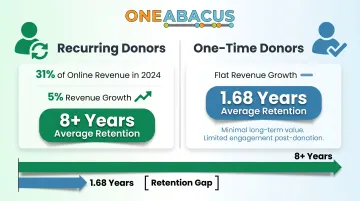

Recurring giving programs are especially powerful. Monthly giving accounted for 31% of all online revenue in 2024, up from 26% the previous year. Revenue from monthly gifts increased 5% while one-time gift revenue remained flat.

The average recurring donor stays active for more than 8 years, compared to just 1.68 years for one-time donors. That retention gap is what makes monthly giving such a reliable cash flow foundation.

Accelerate Inflows and Optimize Expense Timing

On the inflow side:

- Invoice promptly for program fees

- Work with grant funders to align disbursement timing with operational needs — request advance payments or adjusted schedules where possible

- Collect pledges on a set schedule rather than informally

On the expense side:

- Renegotiate vendor payment terms to align with stronger cash months

- Time large purchases using your cash flow forecast as a guide

- Explore shared services or in-kind partnerships with peer nonprofits to reduce overhead

Maintain a Line of Credit as a Liquidity Safety Net

A line of credit secured before a cash crisis occurs allows nonprofits to bridge short-term gaps between grant disbursements or fundraising events without disrupting operations. Treating it as a standard liquidity tool — not a last resort — is the difference between proactive and reactive financial management. Nonprofit Finance Fund and other CDFI lenders offer bridge loans and lines of credit specifically for this purpose.

Managing Restricted Funds and Operating Reserves

Restricted Funds

Keep restricted funds in a separate savings account from unrestricted operating cash. This prevents accidental commingling, ensures compliance with donor or grant conditions, and gives leadership a clear picture of what cash is actually available for day-to-day operations.

Operating Reserves

Operating reserves are unrestricted funds set aside as a financial cushion. Most advisors recommend maintaining 3–6 months of operating expenses in reserve — the right target depends on your revenue volatility, expense predictability, and organizational size.

Most organizations fall short of this benchmark. According to the 2025 State of the Nonprofit Sector Survey, 52% of nonprofits have 3 months or less of cash on hand — and 18% have just one month or less. The Nonprofit Operating Reserves Initiative sets the floor at a minimum reserve ratio of 25% of total annual expenses, roughly 3 months. Organizations with unpredictable revenue or limited expense control should target higher.

Key factors that raise your reserve target:

- High reliance on a single funder or grant cycle

- Seasonal revenue gaps (galas, annual campaigns)

- Government contracts with reimbursement delays

- Rapid growth or pending capital expenditures

When reserves must be temporarily used to cover a cash gap, treat the draw explicitly in your forecast. Both the draw and its planned repayment should appear in the "Other Cash Transactions" section — so the board can see exactly what happened and when the reserve was restored.

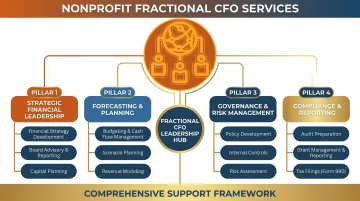

When to Bring In Fractional CFO Support

Many small-to-midsize nonprofits don't have the budget for a full-time CFO but still need senior-level financial leadership. A fractional CFO provides:

- Cash flow forecasting and variance analysis

- Budget development and scenario planning

- Financial policy development (reserve policies, restricted fund policies, cash management policies)

- Board-level reporting and governance support

- Audit preparation and compliance oversight

One Abacus Advisory provides fractional CFO and COO services built specifically for nonprofits. With over 25 years of finance experience and a dedicated nonprofit focus, the team has supported organizations including the San Diego Food Bank, Laguna Playhouse, and Philadelphia Zoo.

Real-World Results

During the Philadelphia Zoo's leadership transition, One Abacus optimized their NetSuite environment, improved month-end close and board reporting, and strengthened financial literacy across the executive team — sustaining continuity despite a lean internal finance staff.

At the San Diego Food Bank, One Abacus stepped in as interim financial leadership after a Finance Director departure, maintaining month-end close processes without disruptions and alleviating pressure during recruitment.

Fractional CFO support gives nonprofits the financial infrastructure to manage cash flow confidently and communicate it clearly to boards and funders. For organizations caught between outgrowing spreadsheets and not yet ready for a full-time hire, it's often the right-sized solution.

Frequently Asked Questions

Do nonprofits have cash flow statements?

Yes. Nonprofits are required under GAAP to include a Statement of Cash Flows in their audited financial statements. It covers operating, investing, and financing activities and follows FASB ASC 958 standards.

How will you manage cash flow and ensure financial sustainability?

Maintain a monthly cash flow forecast, diversify revenue streams, build an operating reserve of 3-6 months of expenses, manage restricted and unrestricted funds separately, and review actuals against projections regularly with leadership and the board.

What is the 33% rule for nonprofits?

The 33% rule refers to the IRS public support test under IRC Section 509(a)(1). To maintain public charity status, a nonprofit must demonstrate that at least one-third of its total support comes from the general public. This is unrelated to cash flow or reserves.

What is the 80/20 rule for nonprofits?

The 80/20 rule (Pareto Principle) in fundraising means that roughly 20% of donors contribute 80% of total revenue. Cultivating major donor relationships and diversifying the donor base helps reduce that concentration risk.

What is a healthy cash reserve for a nonprofit?

Most financial experts recommend 3-6 months of operating expenses as a starting target. The right amount varies based on revenue volatility, the proportion of restricted funds, organizational size, and sector.

How do restricted funds affect nonprofit cash flow?

Restricted funds can only be spent for their designated purpose and are unavailable for general operations. Nonprofits must track them separately and transfer them to operating accounts only when the qualifying activity occurs — creating a gap between reported cash and cash actually available for payroll or bills.