Operating reserves are that cushion — unrestricted funds set aside specifically to stabilize your organization when revenue dips or unexpected expenses hit. Yet 52% of nonprofits have three months or less of cash on hand, with 18% holding just one month. This vulnerability isn't just a statistic — it's a threat to mission continuity.

This guide covers everything you need to build financial resilience: what operating reserves are, how much to hold, practical strategies to build them, how to create a policy that protects them, and how to monitor reserve levels effectively.

TLDR:

- Operating reserves are unrestricted funds controlled by management and the board, distinct from restricted grants

- Most nonprofits should target 3-6 months of operating expenses, with 6-12 months representing stronger stability

- Reserves are built through modest annual surpluses, intentional budget line items, and strategic allocation of unrestricted revenue

- A written reserve policy prevents gradual depletion and creates board accountability for when and how funds are accessed

- Reserves appear as part of "net assets without donor restrictions" on financial statements, not as a separate audited line item

What Are Operating Reserves for Nonprofits?

Operating reserves are unrestricted funds set aside specifically to stabilize a nonprofit's finances during revenue shortfalls or unexpected expenses. Unlike program budgets, restricted grants, or day-to-day working capital, reserves serve one primary purpose: preserving your organization's capacity to deliver on its mission when financial disruptions occur.

The word "unrestricted" is critical here. Donor-restricted funds must be used for designated purposes — you cannot repurpose a program-specific grant to cover payroll during a cash crunch. Operating reserves, by contrast, are controlled entirely by management and the board. They provide the flexibility to respond to emergencies without violating donor intent or grant agreements.

The Restricted Funds vs. Reserves Confusion

Many nonprofits confuse large restricted balances with financial health. Your organization might have $500,000 in net assets, but if $450,000 is tied to specific programs and only $50,000 is unrestricted, your actual financial cushion is far smaller than it appears.

According to the Nonprofit Operating Reserves Initiative (NORI), operating reserves are defined as "the portion of net assets without donor restrictions that nonprofit boards have designated to strengthen financial stability." They are not simply leftover funds — they are a deliberate governance decision to protect organizational sustainability.

The key distinction:

- Restricted funds cannot be repurposed, regardless of financial need

- Operating reserves can be deployed whenever the board authorizes it — making them your true financial safety net

Can a Nonprofit Legally Have a Reserve Fund?

Yes, and it's considered a sign of sound governance. The IRS permits nonprofits to generate surplus funds and maintain reserves, as long as those funds are ultimately reinvested in mission-related activities. There is no specific dollar cap or percentage limit on reserves for 501(c)(3) public charities.

BoardSource confirms: "Nonprofit is a tax status and does not mean that nonprofits cannot generate revenue in excess of their expenses. Being financially successful is the dream of just about every nonprofit."

Funders and auditors view healthy reserves positively — not as evidence of hoarding, but as proof of responsible stewardship. A clearly documented reserve policy signals to grantmakers that your organization plans ahead and can weather disruption without jeopardizing programs.

Types of Nonprofit Reserve Funds

Nonprofits typically maintain three distinct types of reserve funds — each serving a different financial purpose.

Operating Reserves

Operating reserves are the most essential type — designed to cover regular overhead (payroll, rent, utilities, program expenses) if income is disrupted. These are the primary focus of this guide and what most people mean when they use the term "nonprofit reserves."

Operating reserves are not for funding new initiatives or expansion. They exist to buy time when revenue falls short, allowing leadership to adjust strategy, pursue new funding, or make difficult decisions without immediate crisis.

Capital Reserves

Capital reserves are set aside specifically for physical asset needs, including:

- Building maintenance and facility renovations

- Vehicle replacement

- Major equipment upgrades

Organizations that own property or significant equipment should plan separately for these costs rather than drawing on operating reserves when a capital expense hits unexpectedly.

Capital reserves prevent major one-time expenses from destabilizing day-to-day operations. They are particularly important for nonprofits with aging infrastructure or predictable replacement cycles.

Project or Opportunity Reserves

Some organizations maintain a separate project reserve to fund a future initiative or campaign before it officially launches, or an opportunity reserve to act quickly on a strategic opening — such as acquiring a facility lease, launching a pilot program, or responding to an urgent community need.

Unlike the other two types, there is no standard target — the amount depends entirely on specific organizational goals. Project reserves are optional and should only be established once core operating reserves are in place.

How Much Should a Nonprofit Have in Operating Reserves?

The most widely cited standard: three to six months of operating expenses, with six to twelve months representing a stronger position. The right target varies by organization — income type, risk profile, and growth stage all shape what's appropriate.

Income Stability Affects Your Target

Your income mix is the biggest factor in sizing your reserve target:

- Stable income sources (multi-year government contracts, fee-for-service revenue, endowment distributions) support lower reserves — three months may suffice

- Volatile income sources (annual galas, periodic grants, seasonal campaigns) demand a larger buffer — if one event drives 30% of your budget, a cancellation creates a real crisis

- Blended models typically land in the middle, with four to six months as a reasonable target

The Nonprofit Operating Reserves Initiative (NORI) recommends that "the minimum operating reserve ratio at the lowest point during the year be 25%, or about 3 months of the annual operating expense budget." This baseline was established in 2008 and remains the sector standard.

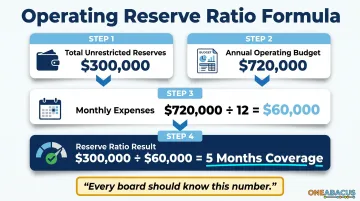

Calculating Your Operating Reserve Ratio

The operating reserve ratio is a useful internal benchmark:

Operating Reserve Ratio = Total Unrestricted Reserves ÷ Average Monthly Operating Expenses

Example calculation:

- Total unrestricted reserves: $300,000

- Annual operating budget: $720,000

- Average monthly expenses: $720,000 ÷ 12 = $60,000

- Reserve ratio: $300,000 ÷ $60,000 = 5 months of coverage

This metric tells you how long your organization could sustain operations if all revenue stopped tomorrow. Every board should know this number.

The Floor and the Ceiling

| Threshold | Guideline | Implication |

|---|---|---|

| Minimum floor | At least 2–4 weeks of operating expenses (one full payroll cycle) | Below this, you risk immediate operational disruption |

| Target range | 3–6 months of operating expenses | Sector standard; adjust based on income stability |

| Strong position | 6–12 months | Appropriate for high-volatility or high-risk organizations |

| Maximum ceiling | No more than 3× the prior year's expenses (BBB Wise Giving Alliance) | Excess funds should be deployed toward mission expansion, endowment building, or capital improvements |

When to Revisit Your Target

Your reserve target should be revisited whenever significant changes occur:

- Major shifts in income reliability (new multi-year contract, loss of anchor funder)

- Organizational growth or downsizing

- External environment changes (economic downturns, regulatory shifts, funding landscape changes)

- New strategic initiatives that alter risk profile

Build a formal reserve review into your strategic planning cycle — at minimum, every three years.

How to Build and Replenish Operating Reserves

Most nonprofits build reserves the same way: through small, consistent annual surpluses — not dramatic fundraising moments or lucky year-end windfalls.

Generate Operating Surpluses

The most common way reserves are built: generating a modest annual operating surplus and intentionally designating a portion as reserves rather than spending it all down.

Some nonprofits include a reserve-building line item directly in their annual budget to formalize this intention. For example, a $1 million budget might include a $25,000 allocation to reserves (2.5% of budget), treating it as a non-negotiable expense rather than hoping for leftover funds at year-end.

A 2024 nonprofit accounting guide notes: "A nonprofit that is not budgeting to have a surplus at their fiscal year end is failing to plan for its long-term sustainability or growth."

Accelerate Reserve Growth

Additional strategies to build reserves faster:

- Designate 5–10% of unrestricted revenue annually as a reserve contribution, built into the budget

- Set a reserve-building goal within capital campaigns rather than directing all proceeds to program expansion

- Deposit proceeds from property or equipment sales into the reserve fund instead of general operations

- Pursue capacity-building grants — some funders specifically support organizations working toward financial sustainability

Financial experts recommend starting with 5% of annual unrestricted revenue designated to reserves. Even at that modest rate, the cumulative effect over 3–5 years is significant.

Replenishing Reserves After Use

Building the fund is only half the work. Once reserves are drawn down, a realistic replenishment plan keeps them from quietly disappearing. Reserves used to address temporary shortfalls should be rebuilt within a defined timeframe — typically 12–24 months for significant drawdowns.

The NORI Toolkit establishes 90 days as a common threshold: if reserve funds are drawn and cannot be repaid within 90 days, a formal repayment schedule should be approved by the board.

Without a replenishment plan, one-time use gradually depletes reserves permanently. The fund becomes a checking account rather than a strategic safety net.

What Reserves Should NOT Be Used For

Reserves buy time to implement new strategies — they do not substitute for strategy itself. Avoid using reserves to:

- Cover ongoing structural deficits

- Fund recurring programs that have lost their base revenue

- Mask chronic budget imbalances

- Delay difficult decisions about program viability

If you find yourself dipping into reserves repeatedly for the same issue, you have a structural problem that requires programmatic or strategic change, not just more cash.

Creating a Nonprofit Operating Reserve Policy

Without documented rules, reserves tend to be gradually depleted over time and are unavailable when truly needed. A written policy creates board accountability, clarity about when funds can be accessed, and governance structure around something that could otherwise be ambiguous.

Why a Written Policy Matters

A reserve policy serves three critical functions:

- Protects the reserve from gradual depletion by requiring formal authorization before funds are accessed

- Provides clarity to staff and board about acceptable use cases and approval processes

- Demonstrates financial stewardship to funders and auditors, building confidence in organizational stability

BoardSource includes "Has the board adopted a formal policy for the establishment of reserves?" as a key financial oversight question every board should be able to answer affirmatively.

Five Essential Policy Elements

Every reserve policy should address:

- Purpose and rationale — Define the specific risks or scenarios the reserve protects against, so the board has a shared understanding of why it exists.

- Target amount and calculation method — Set your target (for example, 6 months of operating expenses) and specify whether non-cash items like depreciation are excluded.

- Authorization requirements — Clarify who can approve a drawdown and under what conditions. Many policies allow the Executive Director to access smaller amounts (up to $10,000) with board notification, while larger draws require Executive Committee or full board approval.

- Replenishment plan — Establish a timeline and funding sources for rebuilding reserves after any drawdown.

- Investment and management guidelines — Specify how reserves are held (separate bank account, money market fund, etc.) and how interest income is treated.

Policy Development Process

Follow these steps to create a reserve policy:

- Board conversation — Begin with a board discussion about the need for reserves and appropriate target levels

- Gather staff input — Finance staff should provide data on cash flow patterns, revenue volatility, and historical shortfalls

- Draft the policy — The finance committee or treasurer drafts the policy, ideally reviewing sample policies from similar organizations

- Present to full board — Share the draft with the full board for feedback and discussion

- Revise and adopt — Incorporate feedback, revise the draft, and formally adopt via board resolution

- Communicate — Share the policy with staff, include it in board orientation materials, and reference it in annual reports to funders

The policy can be a standalone document or embedded within broader financial policies.

Common Policy Mistakes

Too rigid: Authorization thresholds that make reserves inaccessible in genuine emergencies defeat the purpose. If only the full board can approve use and the board meets quarterly, you may not be able to respond to urgent needs.

Too loose: Allowing gradual depletion without board visibility is equally problematic. If the Executive Director can access reserves without reporting requirements, the fund may disappear without the board noticing.

The right policy is accessible enough to work in a real emergency and structured enough to prevent casual depletion. Both extremes create problems; the goal is a policy the board will actually follow.

How One Abacus Advisory Can Help

For nonprofits without deep internal finance capacity, a fractional CFO can move this process from conversation to adopted policy. One Abacus Advisory conducts cash flow analysis, assesses reserve adequacy for your specific risk profile, and translates the findings into board-ready recommendations — all without the overhead of a full-time hire.

This is particularly useful for small to mid-sized nonprofits that need executive-level financial thinking but aren't ready to staff a permanent CFO role.

How Reserves Appear in Nonprofit Financial Statements

Operating reserves are a subset of net assets (formerly called fund balance) and appear on the Statement of Financial Position (balance sheet) under the "net assets without donor restrictions" category. They are not a separate line item by default.

Board-Designated vs. Donor-Restricted

Board-designated reserves remain classified as "without donor restrictions" in audited financial statements, because they are internally designated rather than externally restricted:

- Donor-restricted funds: Cannot be unrestricted without donor permission or fulfilling grant terms

- Board-designated reserves: Can be undesignated at any time by board action

Boards can un-designate reserves whenever financial conditions require it, which is why proper policy and governance discipline matters. The accounting classification alone does not protect the funds — only board commitment to the policy does.

How FASB Standards Changed Reserve Reporting

FASB ASU 2016-14 (effective for fiscal years beginning after December 15, 2017) changed net asset terminology:

- "Unrestricted net assets" became "net assets without donor restrictions"

- "Temporarily restricted" and "permanently restricted" were consolidated into "net assets with donor restrictions"

The update also requires nonprofits to provide qualitative and quantitative information about liquidity — specifically, how the organization manages liquid resources and the availability of financial assets to meet cash needs within one year.

Reserve Disclosure in Reports

That liquidity disclosure requirement makes it practical — and expected — for organizations to label reserves clearly in footnotes and board reports. For example:

Net Assets Without Donor Restrictions:

- Undesignated: $150,000

- Board-designated operating reserves: $300,000

- Board-designated capital reserves: $50,000

- Total net assets without donor restrictions: $500,000

Funders and auditors specifically review the operating reserve ratio (reserves divided by monthly expenses) when assessing organizational financial health. A clearly labeled reserve disclosure — even as a footnote — gives funders the context they need to interpret that ratio accurately, rather than leaving them to guess what portion of net assets is actually available.

Frequently Asked Questions

What are nonprofit reserves?

Nonprofit reserves are unrestricted funds set aside to provide a financial cushion for unexpected expenses or income shortfalls. They are distinct from restricted grants or day-to-day operating budgets and are controlled by management and the board.

Can a nonprofit have a reserve fund?

Yes — and they should. Holding reserves is a best practice for financial health and responsible governance, not evidence of excess funds. The IRS permits reserves as long as they ultimately support mission-aligned activities.

How much reserve funds should a nonprofit have?

The general guideline is three to six months of operating expenses, with six to twelve months indicating stronger financial health. The right amount depends on the organization's income stability, risk profile, and size. Organizations with volatile revenue need larger reserves than those with predictable contracts.

Where in financial statements do reserves appear?

Reserves appear as part of "net assets without donor restrictions" on the Statement of Financial Position. They may be separately labeled in internal board reports or footnote disclosures, but they are not a distinct audited line item on the audited statements.

What is the difference between restricted funds and operating reserves?

Restricted funds must be used per donor or grant requirements, while operating reserves are unrestricted and controlled by management and the board. That distinction gives reserves the flexibility to cover emergencies or revenue shortfalls that restricted dollars cannot.

How do you replenish operating reserves after using them?

A written replenishment plan should be part of the reserve policy, outlining a timeline (typically 12–24 months) and specific funding sources — budget surpluses, fundraising allocations, or unrestricted donations — to rebuild after a drawdown. The board should approve this plan at the same time it authorizes reserve use.