Introduction

Nonprofit CEOs in 2026 are navigating four simultaneous pressures with no sequential relief in sight:

- Federal funding uncertainty and mid-grant termination risk

- Compliance scrutiny at levels that demand dedicated oversight

- Operating costs rising faster than general inflation

- Board accountability expectations that go well beyond quarterly check-ins

The numbers reflect the strain. 36% of nonprofits ended 2024 with an operating deficit — the highest rate in a decade — while 85% expect service demand to increase in 2025. One-third of all U.S. nonprofits reported disruption or loss of government funding in the first months of 2025.

Financial management and governance can no longer operate as separate concerns. When federal grants include termination-for-convenience clauses and payment delays stretch cash flow to breaking, boards need liquidity answers in days — not months.

This guide covers the governance and financial management challenges most likely to create organizational risk in 2026, and what CEOs can do now to get ahead of them.

Key Takeaways

- Federal funding volatility creates direct compliance and documentation risks for government-funded nonprofits

- Revenue concentration exceeding 50% from any single source represents existential exposure when that funding is disrupted

- Reserves below three months — with poor visibility into restricted vs. unrestricted funds — leave organizations exposed to delays and pivots

- Board governance needs active strengthening in 2026: oversight cadence, compliance briefings, and escalation protocols

- Fractional financial leadership delivers CFO-level expertise on reserves strategy, scenario planning, and compliance readiness without full-time costs

The 2026 Operating Environment for Nonprofit CEOs

The nonprofit sector entered 2026 carrying compounding financial pressures, not isolated headwinds. 86% of organizations report that inflation has impacted both their operations and the clients they serve, driving up costs for everything from payroll to supplies. Only 41% can pay all full-time staff a living wage, and just two-thirds offer health insurance — a number that drops to 12% among organizations with budgets under $250,000.

Funding volatility compounds the cost crisis. 33% of all U.S. nonprofits reported a disruption to or loss of government funding during the first four to six months of 2025. Among nonprofits receiving government grants, 84% expect cuts to that funding source. The deficit trajectory tells the story: among repeat survey respondents tracked between 2021 and 2024, the share operating in deficit jumped from 13% to 37%.

The federal policy environment shifted sharply in 2025. The August 7, 2025 Executive Order "Improving Oversight of Federal Grantmaking" imposed three specific burdens on discretionary grantees:

- Termination-for-convenience clauses added to all discretionary grants

- Written explanations required for every drawdown request

- Preferences imposed for lower indirect cost rates

A formal grants "pause" took effect January 28, 2025, followed by a federal government shutdown beginning October 1, 2025 — during which agencies were unable to process reimbursements or payments. For any nonprofit dependent on federal contracts or grants, these are direct operational threats with immediate cash flow consequences.

Most nonprofit CEOs are managing multiple crises at once: rising demand, workforce pressures, funding instability, and compliance expectations that carry reputational and financial consequences. This environment makes structured governance and disciplined financial management systems more important, not less. Organizations without real-time cash flow visibility, formalized compliance escalation pathways, or board-accessible financial dashboards will fall behind those that build these capacities now.

Governance Challenge: Strengthening Board Oversight When Stakes Are High

Meaningful governance in 2026 extends beyond meeting quorum and approving annual budgets. Boards need visibility into funding concentration risk, compliance readiness, and contingency planning before problems emerge. Boards that receive financial reporting reactively — after a grant is frozen, after reserves are exhausted, after an audit finding surfaces — are structurally behind.

The federal oversight environment demands proactive governance. When agencies emphasize program integrity and documentation standards, audit and finance committees must be briefed on compliance hot spots, single audit exposure, and documentation completeness. This briefing should include:

- Percentage of revenue tied to federal or state funding by program

- Status of internal controls documentation (procurement files, timekeeping, eligibility verification)

- Known compliance gaps or single audit findings from prior periods

- Contingency plans if a major grant is delayed, reduced, or terminated

BoardSource's Recommended Board Practices specify that financial statements must not be included in a consent agenda — they require dedicated discussion. Yet governance gaps persist across the sector. The most common include:

- Infrequent or overly summarized reporting — quarterly summaries without cash-on-hand metrics, funding concentration percentages, or restricted vs. unrestricted balances leave boards unable to assess real risk

- No compliance escalation pathway — when documentation deficiencies or audit triggers surface, there's often no protocol for getting that information to the board fast enough to act

- Outdated risk registers — organizations still tracking risks identified in 2022 or 2023 haven't adjusted for federal funding freezes, increased audit scrutiny, or the current cost environment

Each gap creates real organizational risk. Boards without timely financial data can't approve mid-year budget adjustments or authorize reserve drawdowns when timing matters most.

Without compliance escalation protocols, problems often reach the board only after a funder or auditor has already flagged them — at which point the response window is narrow. Outdated risk registers compound this by giving boards false assurance that identified risks remain contained.

Translating Financial Risk Into Board-Visible Reporting

The CEO's role is translating complex financial and compliance data into reporting that enables informed oversight without creating information overload. Clarity and decision-readiness are the standard.

Key metrics that matter most:

- Months of cash on hand (total cash divided by average monthly operating expenses)

- LUNA (Liquid Unrestricted Net Assets) — unrestricted net assets minus non-liquid assets like buildings, equipment, and board-restricted endowments

- Revenue concentration by source — percentage of total revenue from each major funding stream

- Restricted vs. unrestricted balances — what funds are available for operating needs vs. locked to specific programs

- Known funding risks — grants up for renewal, contracts under review, anticipated reductions

Reporting cadence should match organizational risk. For organizations with three months or less of cash on hand or significant federal funding exposure, monthly board dashboards are appropriate. Quarterly reporting is acceptable for organizations with stronger reserves and diversified revenue. Format matters: one-page dashboards with clear visuals outperform 20-page financial packets.

Questions a nonprofit CEO should be prepared to answer for any audit or finance committee in 2026:

- What percentage of our revenue is tied to federal or state funding?

- How mature are our documentation controls for government grants (procurement, timekeeping, eligibility)?

- What is our contingency plan if a major grant is delayed or restructured?

- How many months of liquid unrestricted net assets do we currently hold?

- What single audit findings or compliance gaps exist from prior periods?

CEOs who can answer these questions with current, data-backed specifics demonstrate genuine governance readiness — and give boards the footing to make sound decisions before a funding disruption forces the issue.

Financial Management Challenge: Revenue Volatility and Funding Concentration Risk

Revenue concentration risk means an organization derives the majority of its revenue from a single source — whether a federal grant, one major foundation, or a single earned revenue stream. When that source is reduced or eliminated, the organization faces existential disruption. The current federal funding environment makes this risk concrete, not theoretical.

Approximately 35,000 nonprofits rely on government grants for more than 50% of their total revenue. Among larger nonprofits with budgets exceeding $5 million, 55% receive government grants. In the human services subsector, 40% report government funding as their primary revenue stream. When federal agencies freeze grants, delay reimbursements, or exercise termination-for-convenience clauses, these organizations have no financial cushion.

Nonprofits generally operate under one of five revenue models: individual donors, foundation grants, government contracts, fee-for-service, or membership. Each carries distinct risk sensitivities in 2026:

- Government contracts: Direct exposure to federal policy changes, payment delays during continuing resolutions or shutdowns, and heightened compliance requirements. Organizations in this model need immediate scenario planning for 20–30% funding reductions.

- Foundation grants: Concentration risk when a small number of large grants dominate revenue. Grantmaking cycles slow during economic uncertainty — and private foundations would need to increase grantmaking by 282% to offset a total loss of government grants across the sector, an impossible lift.

- Individual donors, fee-for-service, and membership: Generally more stable but require significant infrastructure investment to scale — especially for organizations pivoting away from government dependency.

Diversification is the standard response — but it's operationally complex. Shifting from government contracts to individual donors requires new infrastructure: donor databases, fundraising staff, stewardship systems, and brand recognition.

Organizations starting this work in 2026 should set realistic timelines (18–36 months for meaningful traction) and budget for the transition explicitly. Diversification doesn't happen on a shoestring.

Rolling Forecasts and Scenario Planning as Management Tools

Static annual budgets are insufficient when federal payments are delayed, grant terms change, or a major donor reduces support. Annual budgets offer no visibility into how long the organization can sustain operations under stress. Rolling forecasts and scenario planning address this gap.

Rolling forecasts update monthly or quarterly, projecting 12–18 months forward based on actual revenue and expense patterns. They answer a direct question: "If current trends continue, when will we run out of cash?" That's a different lens entirely from a variance report comparing actuals to a budget approved nine months ago.

Scenario planning models best case, base case, and stress case futures. A stress case might assume:

- 25% reduction in federal funding beginning in Q3

- 60-day delays in government reimbursements

- 10% increase in program demand without corresponding revenue growth

Leadership uses scenario results to identify decision points: At what cash balance do we freeze hiring? When do we draw on a line of credit? What programs can be scaled back if a grant is terminated?

A 2026-ready financial planning process requires clear ownership across leadership:

- The CFO or senior finance lead owns forecast updates on a rolling basis

- The CEO triggers scenario plan reviews when external developments shift — policy changes, funding announcements, grant terminations

- The board receives scenario results with enough lead time to act, not after options have narrowed to crisis management

Building Liquidity Discipline and Cash Flow Visibility

The operating reserve benchmark most commonly cited is three to six months of operating expenses, a standard recommended by the Nonprofit Operating Reserves Initiative (NORI) Workgroup. Yet 52% of nonprofits have three months or less of cash on hand, and 18% have one month or less. Among organizations surveyed in both 2022 and 2025, the share with six or more months of cash fell 10 percentage points — from 36% to 26%. This gap creates direct operational risk in 2026 when payment delays, grant freezes, and funding gaps are more likely, not less.

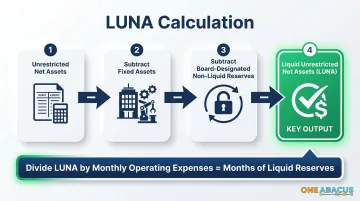

LUNA (Liquid Unrestricted Net Assets) is the most actionable liquidity metric for nonprofit leaders. It's calculated by taking total unrestricted net assets and subtracting non-liquid assets: buildings, equipment, long-term receivables, and board-restricted endowments. The result is the organization's flexible financial cushion: reserves that can be accessed without restriction.

Total net assets on a balance sheet may look healthy, but if most are tied up in property or restricted funds, LUNA reveals the true operating runway.

CEOs can calculate LUNA from existing financial statements:

- Start with unrestricted net assets (from the Statement of Financial Position)

- Subtract fixed assets (buildings, equipment)

- Subtract any board-designated reserves that aren't truly liquid

- The result is liquid unrestricted net assets

Divide LUNA by average monthly operating expenses to get months of liquid reserves available.

Specific Cash Flow Risks to Model in 2026

Delayed government reimbursements — Federal agencies operating under continuing resolutions or during shutdowns cannot process payments. Nonprofits operating on cost-reimbursement contracts must cover payroll and program costs using reserves or credit while waiting for reimbursement.

Continuing resolution funding gaps — When Congress operates under continuing resolutions instead of full appropriations, some grant programs face temporary freezes or reduced allocations. Organizations need to model 30-60 day gaps in expected revenue.

Slower grant-making cycles — Foundation and corporate grantmaking often slows during economic uncertainty or leadership transitions. Organizations should model 90-120 day delays in expected foundation grants.

Restricted funds that cannot be deployed for operating needs — A nonprofit may hold significant cash balances, but if those funds are restricted to specific programs or capital projects, they cannot be used to cover payroll during a cash shortfall.

A detailed monthly cash flow projection (distinct from an income statement) addresses these risks directly. It should:

- Track actual cash in and cash out by week or month

- Flag periods where cash dips below minimum operating thresholds

- Identify decision points when leadership needs to act

When to Consider Debt Strategically

For organizations with a functioning board, documented financial policies, and a clear revenue bridge, short-term debt instruments or lines of credit can preserve program continuity during funding gaps. Borrowing makes sense when:

- The organization has documented revenue commitments (signed grant agreements, contracts) that will replenish cash within 6-12 months

- The board has approved a debt policy and specific borrowing authority

- Leadership has modeled repayment scenarios and confirmed capacity to service the debt

- The alternative to borrowing is program cuts or layoffs that would damage mission delivery

Avoid debt when revenue is uncertain, reserves are already depleted, or the board hasn't approved specific borrowing authority. Used strategically, short-term credit preserves mission delivery during temporary gaps — but it cannot substitute for the reserves discipline the organization should be building in parallel.

Workforce, Talent, and the True Cost of Leadership Gaps

Nonprofit compensation lags the private sector, creating talent competition challenges. The wage gap for transferable roles like finance director or marketing manager narrowed from approximately 40% pre-pandemic to approximately 20% currently, but funding has not kept pace with wage growth. According to Candid's 2024 Nonprofit Compensation Report, the median compensation for a top finance position is approximately $125,000, while top operations roles exceed $150,000 — figures that many mid-size nonprofits cannot sustain.

Leadership gaps in finance and operations create downstream risks. When a CFO or Controller position is vacant or under-resourced, the effects ripple quickly:

- Financial reporting accuracy deteriorates

- Grant compliance and drawdown oversight falls through the cracks

- Board-level financial visibility weakens at exactly the wrong moment

Executive searches typically take 12-14 weeks — and that's after an organization decides to fill the role. During that gap, who is preparing board financials, overseeing grant drawdowns, and ensuring single audit compliance?

That gap underscores why compensation benchmarking is a governance function, not just an HR task. Boards and CEOs should regularly review whether pay for senior finance and operations roles is competitive enough to retain talent. When turnover is driven by below-market compensation, the organization pays in other ways: lost institutional knowledge, disrupted financial operations, and compliance exposure during transitions.

Fractional CFO and COO models offer a practical alternative. Most nonprofits need senior-level financial and operational thinking for 8-20 hours per week, not 40. Fractional leadership pairs lean internal staff with specialists who step in at critical moments:

- Audit preparation and single audit compliance

- Board reporting cycles and financial narrative

- Scenario planning and cash flow forecasting

- Grant compliance readiness and system optimization

Heading into 2026, this model is gaining real traction — driven by wage pressures, ongoing leadership vacancies, and boards unwilling to leave critical functions exposed while a full-time search drags on for months.

What Nonprofit CEOs Should Prioritize Before Year-End 2026

Three immediate actions can reduce risk and strengthen organizational readiness:

1. Brief the audit/finance committee on funding concentration risk and compliance readiness with specific data. Provide a one-page summary showing percentage of revenue by source, months of liquid reserves, and status of documentation controls for major federal grants. Identify any known compliance gaps or single audit exposure.

2. Conduct a documentation stress test on one or two major grants. Pull procurement files, timekeeping records, and eligibility documentation for a major federal grant. Are files complete? Are processes documented? Are personnel costs allocated correctly? Common single audit findings include incomplete procurement documentation, missing timekeeping support, and failure to monitor subrecipients. The single audit threshold increased from $750,000 to $1,000,000 in federal expenditures under 2024 Uniform Guidance revisions, meaning some organizations may exit the requirement — but those remaining face heightened scrutiny.

3. Update the organization's risk register to reflect current conditions. Federal oversight tone, payment timing risks, and reserve adequacy have all shifted since 2023. A current risk register should document:

- Federal funding concentration and exposure to policy changes

- Liquidity risk (months of cash, LUNA, restricted vs. unrestricted balances)

- Compliance hot spots (audit findings, documentation gaps, grant reporting deadlines)

- Workforce risks (key vacancies, retention challenges, compensation competitiveness)

Strategic Financial Infrastructure Investment

Organizations that invest now in stronger financial systems, more frequent reporting cadences, and formalized scenario planning processes will have a structural advantage. This investment looks like:

- Monthly rolling forecasts integrated into management reporting

- Board dashboards with key liquidity and concentration metrics updated quarterly or monthly

- Documented internal controls for federal grants (procurement, timekeeping, allowability)

- Scenario planning protocols triggered by funding announcements or policy changes

- Fractional financial leadership engaged during high-risk transitions or capacity gaps

These are near-term priorities. Organizations that build this infrastructure now will be positioned to respond to funding shifts and compliance demands with confidence rather than improvisation.

When to Engage Fractional Financial Leadership

For many nonprofits, the gap between what internal staff can handle and what the organization actually needs becomes most visible during high-stakes moments. Consider fractional CFO support when:

- A CFO or Controller vacancy exists and the search timeline is uncertain

- The organization is preparing for a single audit, major grant application, or significant funding decision

- The board is asking financial questions that internal staff cannot answer with confidence

- Revenue concentration exceeds 50% and leadership needs scenario planning and diversification strategy

- Documentation or compliance gaps exist and the organization lacks internal capacity to address

Fractional CFOs deliver targeted expertise at moments of highest need — reserves strategy, board-ready financial dashboards, compliance readiness assessments, scenario modeling, and accounting system upgrades.

One Abacus Advisory provides this kind of fractional CFO and COO support for nonprofits navigating financial transitions, leadership gaps, and governance strengthening. Organizations receive senior-level guidance without the cost or timeline of a full-time hire, ensuring financial stability and mission continuity during critical periods.

Frequently Asked Questions

What are the biggest financial management challenges for nonprofit CEOs in 2026?

Federal funding volatility, rising costs above inflation, widespread reserve deficits, and heightened compliance scrutiny are all arriving at once. The real difficulty is managing these pressures simultaneously rather than in isolation.

How can a nonprofit CEO strengthen board governance without overwhelming board members?

Focus on disciplined, structured financial reporting: clear dashboards showing LUNA, funding concentration, and months of cash; a consistent reporting cadence (monthly or quarterly based on risk); and briefing protocols that prioritize decisions over data. Use one-page summaries, not 20-page packets.

What operating reserve target should nonprofits aim for in 2026?

The commonly cited benchmark is three to six months of operating expenses. The right target depends on the organization's revenue model, payment timing risks, and current funding environment. Government-funded nonprofits facing reimbursement delays should aim toward six months; diversified earned-revenue models may operate safely at three months.

How should nonprofit CEOs respond to federal funding uncertainty?

Conduct scenario planning for 20-30% funding reductions, strengthen documentation discipline for all federal grants, accelerate revenue diversification with realistic timelines and dedicated funding, and brief boards proactively on exposure and contingency plans. Organizations that plan ahead have more options when funding shifts.

When should a nonprofit CEO consider hiring a fractional CFO?

Common triggers include:

- Finance leadership vacancies or gaps in internal capacity

- Board requests for financial guidance the organization can't answer internally

- Audit preparation or major grant applications requiring CFO-level oversight

- Inadequate financial reporting infrastructure

- Need for expertise on reserves strategy, compliance, or scenario planning without a full-time hire

What financial metrics should a nonprofit CEO report to the board?

The essential dashboard includes months of cash on hand, LUNA (liquid unrestricted net assets), revenue by funding source with concentration percentages, restricted vs. unrestricted balances, and any known funding risks or compliance flags. These metrics enable informed oversight and timely decisions.