Introduction

Nonprofit finance leaders juggle an exhausting balancing act: managing multiple grants simultaneously, each with distinct funder requirements, documentation standards, and ironclad deadlines. A single reporting misstep can jeopardize future funding, trigger audits, or force clawbacks that devastate already-thin budgets. According to the Nonprofit Finance Fund, 36% of nonprofits ended 2024 with an operating deficit — the highest rate in a decade — and 84% receiving government funding expect cuts. In this climate, strong grant reporting is a core survival skill, not just a compliance checkbox.

This guide covers the strategies that separate struggling organizations from those that maintain funder confidence:

- Understanding what funders actually require

- Building capable internal teams and reliable systems

- Avoiding the reporting pitfalls most likely to trigger negative audit findings

What Is Grant Financial Reporting and Why Does It Matter?

Grant financial reporting is the formal process of documenting how grant funds were spent, demonstrating program outcomes, and confirming compliance with funder terms. It's not simply a compliance checkbox—it's a trust-building exercise that directly influences whether funders renew or increase support.

Government funding represents 32% of total nonprofit revenue, according to the National Council of Nonprofits, making grant reporting capacity essential for most organizations. When reporting is thorough and accurate, funders see fiscal accountability and clear impact, which translates directly into continued support.

Requirements vary dramatically by funder type. Federal grants governed by 2 CFR 200 Uniform Guidance carry rigorous documentation and audit requirements—far more demanding than private foundation grants. The regulation establishes uniform administrative requirements, cost principles, and audit standards that all federal award recipients must follow.

Understanding each award's compliance tier—and building systems to match—is where reporting capacity either holds or breaks down. Nonprofits that treat federal and private foundation grants interchangeably often find themselves scrambling when audit season arrives.

What Funders Actually Require: The Two Components of a Grant Report

Virtually all grant reports include two core components: a financial report showing how dollars were spent against the approved budget, and a narrative describing program activities, outcomes, and impact. When these two components conflict — numbers that don't match described activities, or activities that lack corresponding line items — funders take notice.

Narrative Requirements

The narrative section must address:

- Project activities completed and key milestones reached

- Changes from the original proposal and reasons for adjustments

- Challenges encountered and how they were addressed

- Human impact of the funded work, with quantified results tied to approved KPIs

Strong narratives cite specific outcomes—not vague descriptions. Cross-reference your original grant proposal when drafting the narrative so every promised deliverable is accounted for. Unaddressed activities are immediate red flags to funders.

Financial Reporting Requirements

Financial reporting entails:

- Budget-versus-actual comparison showing planned vs. actual spending

- Documentation of all expenditures including payroll allocations

- Explanation of budget variances (both over and under spending)

- Audited financial statements when required by funder terms

Grant dollars are typically restricted, meaning they can only be spent on approved activities. Your financial report must clearly show that restricted dollars were not commingled with general operating funds — which requires proper fund accounting in your general ledger.

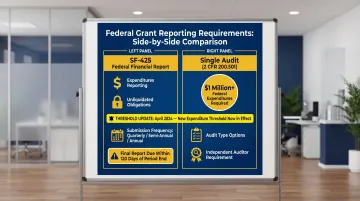

Federal grant recipients also need to know two key reporting requirements:

| Requirement | What It Covers |

|---|---|

| SF-425 (Federal Financial Report) | Reports expenditures, unliquidated obligations, and unobligated balances. Funders typically require quarterly, semi-annual, or annual submissions, with final reports due 120 days after the project period ends. |

| Single Audit (2 CFR 200.501) | Required for organizations with $1 million or more in federal expenditures during their fiscal year (threshold raised from $750,000 in April 2024). Organizations above this line must engage an independent auditor for a program-specific or organization-wide audit. |

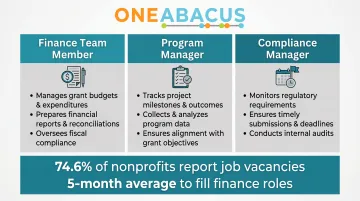

Building the Right Internal Team for Grant Reporting

Grant reporting accuracy depends on having the right people in the right roles:

- Finance team member: owns revenue recognition for restricted contributions and ensures grant funds are coded correctly in the accounting system

- Program manager: captures day-to-day activity data and outcomes that feed directly into narrative and financial reports

- Compliance manager (for significant federal funding): maintains reporting calendars and flags regulatory deadlines before they become emergencies

Aligning Development and Finance Departments

The grant award recorded in your development CRM must reconcile with how it's coded in your accounting system. When these two functions operate in silos, discrepancies accumulate quietly — and by the time a report is due, reconciling them takes hours your team doesn't have. A simple monthly sync between development and finance, with a shared grant tracking spreadsheet as the anchor, eliminates most of this friction before it starts.

Time Tracking as a Team Process

Payroll allocations to specific grants must be documented through structured time tracking connected to the general ledger. This is especially critical for federal grants where salary allocations must be auditable under 2 CFR 200.430. The regulation explicitly states that "budget estimates alone do not qualify as support for charges to federal awards"—periodic after-the-fact reviews must confirm accuracy.

The Staff Education Gap

Program staff who approve or submit expenses need to understand:

- What costs are allowable under each grant

- What documentation is required

- Why proper coding matters to the organization's compliance

When staff lack this context, errors enter the system at the source — the hardest place to catch them. With 74.6% of nonprofits reporting job vacancies and an average 5-month timeline to fill finance roles according to the National Council of Nonprofits, cross-training becomes a practical necessity, not a nice-to-have.

Setting Up Processes and Systems That Work

The Foundation: Fund-Level Reporting in Real Time

Your financial management platform must be configured to track each grant separately, with fund-level reporting that shows budget versus actuals in real time—not through spreadsheets or manual reconciliations. According to research from NonProfit PRO, 61% of nonprofits still rely on generic spreadsheets for financial management, while only 35% generate automated reports. Manual processes dramatically increase error risk.

Designing a Grant Coding Structure

Group grants by fund type (federal, foundation, corporate, individual) and assign unique project or grant codes in your general ledger. This structure makes it far easier to:

- Generate accurate reports on demand

- Respond quickly to funder inquiries

- Track compliance obligations by grant tier

Integrating Time Tracking with Payroll

Integrate time tracking directly with payroll and accounting systems so salary and benefit allocations flow automatically to correct grant codes. This reduces manual entry errors and creates an audit trail that satisfies federal requirements. This reduces manual entry errors and creates a clean audit trail. Each entry captures the employee, hours worked, grant code, and approval date—exactly what federal auditors expect to see.

Purpose-Built Accounting Tools

Tools like NetSuite can be configured specifically for nonprofit grant tracking, with capabilities that include:

- Automated budget-to-actual reports

- Flagging of reimbursable costs at the point of entry

- Centralized grant documentation across all funds

One Abacus Advisory specializes in NetSuite optimization for nonprofits, helping organizations configure these systems correctly from day one. During a leadership transition at Philadelphia Zoo, One Abacus optimized their NetSuite environment—strengthening reporting accuracy and giving leadership renewed confidence in their financial results.

Documentation Discipline Throughout the Grant Period

Strong systems only work when paired with consistent documentation habits. Maintain discipline throughout the grant period—not just at reporting deadlines—by retaining the following in an organized digital system:

- Invoices and receipts

- Timesheets and payroll records

- Approval records and sign-offs

- Contracts and grant agreements

This keeps you audit-ready year-round and makes report preparation a quick pull from your system, not a last-minute scramble.

Common Grant Reporting Mistakes (and How to Avoid Them)

Mistake #1: Waiting Until the Report Is Due

The most damaging mistake is waiting until the report deadline to compile financial data. This leads to errors, missing documentation, and budget variances that cannot be explained. Grant tracking should begin the day the award is received.

Mistake #2: Failing to Explain Variances Proactively

Funders expect transparency when actual spending deviates from the approved budget. According to The Charity CFO, failing to explain variances—both over and under—signals poor financial management. Document variance reasons in real time — not when the report deadline arrives.

Mistake #3: Inadequate Audit Trails

Missing documentation, unapproved budget reallocations, and vague expense coding are the most common triggers for funder audits or clawbacks. Poor grant reporting can result in:

- Withheld payments from funders

- Repayment obligations (forced returns of funds)

- Reduced eligibility for future grants

- Negative audit findings

The Chronicle of Philanthropy notes that recovering from these failures — through repayments, audits, and lost funder relationships — consistently costs more than building the right systems upfront. A well-maintained accounting system with role-based access and change logs prevents most of these outcomes before they start.

How a Fractional CFO Can Strengthen Your Grant Reporting

Many nonprofits lack a full-time CFO but still carry significant grant portfolios requiring sophisticated financial oversight. A fractional CFO provides the strategic financial leadership needed to:

- Design compliant reporting systems

- Train staff on grant accounting best practices

- Serve as the knowledgeable reviewer sign-off before reports go out

- Ensure alignment between development, finance, and program teams

Research from BTQ Financial found that 30% of nonprofits outsource finance and accounting, with 65% citing grant management and reporting as the second most commonly outsourced financial service. Nonprofits with a finance partner are 6x less likely to struggle scaling their finance functions to support growth.

That gap between needing financial leadership and affording it full-time is exactly where a fractional CFO earns its value. One Abacus Advisory works with nonprofits — including the San Diego Food Bank and Laguna Playhouse — to build the infrastructure needed to manage grants confidently. Their work covers federal, state, and local grant portfolios, with a focus on compliance, drawdown accuracy, and timely reporting to maintain funder confidence.

Frequently Asked Questions

What is a grant financial report?

A grant financial report is a formal document submitted to funders showing how grant dollars were spent against the approved budget. It typically includes a budget-versus-actual comparison, expense documentation, and a written explanation of any variances between planned and actual spending.

What are the reporting requirements for a grant?

Requirements vary by funder but commonly include a financial report on fund use, a narrative describing program activities and outcomes, documentation of expenses, and (for federal grants) adherence to forms and timelines specified under the award agreement.

What is a SF 425 report?

The SF-425 is the standard Federal Financial Report form used by recipients of federal grants to report expenditures, unliquidated obligations, and cash status for each award period, typically submitted quarterly or at closeout.

What is 2 CFR 200 Uniform Guidance?

2 CFR 200 (Uniform Guidance) is the federal regulation governing the administration of federal awards. It establishes requirements for accounting, financial reporting, procurement, internal controls, and audit standards that all recipients of federal funds must follow.

Is grant accounting difficult?

Grant accounting is more complex than general accounting because it requires tracking restricted funds separately, allocating shared costs (like salaries) across multiple grants, and meeting funder-specific documentation standards. Organizations that invest in purpose-built accounting systems and experienced financial leadership tend to navigate these demands with far fewer compliance gaps.

Are government grants public record?

Federal grant awards are publicly disclosed on USASpending.gov as required by the Federal Funding Accountability and Transparency Act (FFATA), meaning the recipient name, award amount, funding agency, and location are publicly accessible.