According to BBB Wise Giving Alliance's 2026 Donor Trust Report, 67.7% of Americans say trusting a charity is essential before donating—yet barely 18.3% report high trust in nonprofits. In this trust-scarce environment, proper restricted fund management isn't just a compliance task; it's a core pillar of your organization's credibility.

This guide walks you through what restricted funds are, the three classifications under FASB standards, the accounting mechanics of recording and releasing restrictions, and the best practices that keep your nonprofit compliant, transparent, and donor-trusted.

Key Takeaways

- Only donors impose restrictions — board-designated funds remain unrestricted in legal and accounting terms

- Three fund types exist: unrestricted (no donor conditions), temporarily restricted (purpose or time-bound), and permanently restricted (endowments)

- Revenue recognition happens immediately when an unconditional contribution is received, not when spent

- Two-column financial statements separate "with donor restrictions" from "without donor restrictions" — clarifying which assets are freely available

- Every restriction release requires documentation: gift instruments, grant agreements, and donor correspondence

What Are Restricted Funds?

Restricted funds are contributions earmarked by a donor for a specific purpose, time period, or both. Unlike unrestricted funds—which your nonprofit can allocate at its own discretion for any mission-aligned use—restricted funds carry legally binding limitations that dictate exactly how and when the money may be spent.

Only donors can legally impose restrictions. This distinction trips up many nonprofits. When your board sets aside $50,000 for a future facility renovation, those dollars remain unrestricted in accounting and legal terms. The board can change its mind at any time. True restrictions are external, donor-imposed, and irrevocable without the donor's consent.

This distinction matters because:

- Net assets with and without donor restrictions appear on IRS Form 990, Part X (Balance Sheet), lines 27 and 28 — misclassification distorts your public financial profile

- State attorneys general enforce restricted fund obligations under UPMIFA, adopted by 49 states and the District of Columbia

- Treating board designations as "restricted" inflates your reported constraints and misleads stakeholders about your actual financial flexibility

Under FASB ASC 958, donor-restricted net assets carry stipulations that are "more specific than the broad limits resulting from the nature of the organization." These restrictions specify purpose, time period, or perpetual maintenance of contributed assets, and they remain binding until the organization satisfies the donor's conditions.

Types of Nonprofit Fund Restrictions

Unrestricted Funds

Unrestricted funds are contributions free from external conditions. Your nonprofit may use them for any mission-aligned purpose: administrative salaries, fundraising expenses, office rent, program gaps, or strategic reserves.

Common sources include:

- Small individual donations without stipulations

- Most corporate matching gifts

- Investment returns on unrestricted endowments

- Fundraising event proceeds (unless specifically designated by attendees)

Unrestricted revenue funds the infrastructure — staff, systems, compliance — that makes program delivery possible. Without it, even a well-funded nonprofit can struggle to keep the lights on. Yet securing unrestricted gifts is notoriously difficult: donors consistently prefer to earmark contributions for specific programs they can point to.

Temporarily Restricted Funds

Temporarily restricted funds carry donor-imposed limitations tied to purpose (a grant for a literacy program), time (funds that must be spent in fiscal year 2027), or both.

Once your organization satisfies the restriction — by spending funds on the designated program or reaching the specified date — the restriction releases and those funds become unrestricted.

Common sources:

- Foundation grants specifying program use

- Government grants with performance milestones

- Major donor gifts earmarked for capital campaigns

- Corporate sponsorships tied to specific events

Temporarily restricted funds vs. deferred revenue: why the distinction matters

Getting this classification wrong affects whether you record revenue or a liability on your books:

- Temporarily restricted funds are recognized as revenue immediately upon receipt. The donor has no right of return; the organization is entitled to the contribution, subject only to spending restrictions

- Deferred revenue (or refundable advance) represents a liability. The nonprofit has not yet earned the contribution because it must first satisfy a conditional barrier (such as completing a service or hitting a performance milestone)

Under FASB ASU 2018-08, a contribution is conditional if it includes both (a) a barrier that must be overcome and (b) a right of return or right of release. Only when the condition is met does the liability convert to revenue.

Permanently Restricted Funds

Permanently restricted funds — most commonly endowments — require that the principal remain invested in perpetuity. Your organization may spend only the investment earnings, and only in accordance with the donor's designated purpose.

Key characteristics:

- The original donated principal is never spent

- Investment earnings may be used for donor-specified purposes (scholarships, program support, general operations)

- Term endowments hold principal for a specified period rather than indefinitely

- Most common at universities, hospitals, and cultural institutions, but available to any nonprofit

UPMIFA's prudence-based framework replaced the rigid "historic dollar value" rule of the old Uniform Management of Institutional Funds Act (UMIFA). If an endowment's market value falls below the original gift amount ("underwater endowment"), UPMIFA permits prudent spending — unlike UMIFA, which prohibited any spending below the historic value.

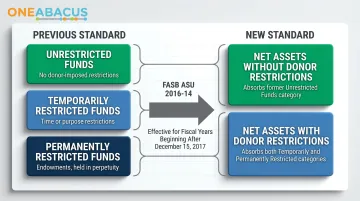

FASB ASU 2016-14: The Two-Class Consolidation

FASB issued ASU 2016-14 in August 2016 — the first major nonprofit reporting overhaul since 1993. It collapsed three net asset categories into two:

- Net assets without donor restrictions (includes board-designated funds)

- Net assets with donor restrictions (includes both time/purpose restrictions and perpetual restrictions)

Effective for fiscal years beginning after December 15, 2017, this change simplified financial statements and improved transparency. The practical implication: your financial statements now present two columns, making it immediately clear which portion of net assets is available for discretionary use.

The Risks of Mismanaging Restricted Funds

Legal Noncompliance

Misappropriating restricted funds is not a paperwork error—it's a breach of fiduciary duty that can trigger serious legal consequences:

- State attorney general enforcement: In April 2022, California's AG secured a $606,000 judgment against ZeroDivide for diverting restricted donations to general operations, resulting in organizational dissolution and a three-year ban on two officers from leading California charities

- IRS penalties: Misuse of restricted funds can jeopardize tax-exempt status and trigger intermediate sanctions (personal penalties) on responsible parties

- Donor lawsuits: Donors retain the legal right to sue if their contributions are used contrary to stated restrictions

Worth noting: state attorneys general, not the IRS, are typically the primary enforcement authority for restricted fund violations under UPMIFA and state charitable trust laws. That distinction matters when assessing where your compliance risk actually lives.

Reputational Risk

A single misuse of restricted funds can signal untrustworthiness to your entire donor community. Independent Sector's 2025 Trust in Nonprofits study found that 57% of Americans report high trust in nonprofits, the highest of any sector, but that trust is fragile and easily damaged by financial mismanagement.

The BBB Wise Giving Alliance puts the stakes in sharper relief: two-thirds of donors say trust is essential to their giving decisions, yet fewer than one in five trust charities highly. When donors feel their intent has been disregarded, they stop giving, and rebuilding that confidence is far harder than protecting it in the first place.

Financial Misassessment

Restricted cash sitting on your balance sheet can create the illusion of financial health. If your organization reports $500,000 in net assets but $400,000 is restricted for a capital campaign, your actual operating reserves are only $100,000, often too thin to cover three months of expenses.

Common pitfalls:

- Board members make strategic decisions assuming all net assets are available

- Leadership budgets using restricted revenue for general operations, creating cash shortfalls when restrictions come due

- Auditors question "going concern" status if restricted funds have been used for unintended purposes

To avoid these traps, maintain three to six months of expenses in unrestricted reserves and project cash flows at least 12 months ahead, keeping restricted and unrestricted funds clearly separated in your projections.

How to Record and Release Restricted Funds

Revenue Recognition Rule

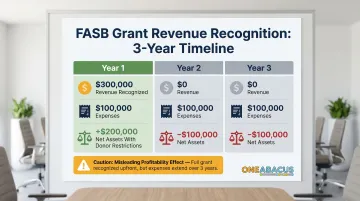

Under FASB ASC 958-605, unconditional contributions with donor restrictions are recognized as revenue when the contribution is received—not when the funds are spent.

Why this matters:

A three-year, $300,000 grant received in year one is recorded as $300,000 in revenue with donor restrictions in year one. If you spend $100,000 each year, your financial statements will show:

- Year 1: $300,000 revenue, $100,000 expenses, $200,000 increase in net assets with donor restrictions

- Year 2: $0 revenue, $100,000 expenses, $100,000 decrease in net assets with donor restrictions

- Year 3: $0 revenue, $100,000 expenses, $100,000 decrease in net assets with donor restrictions

Without proper tracking, year one can look misleadingly profitable while years two and three appear to run deficits.

Two-Column Financial Statement Approach

ASU 2016-14 requires nonprofits to present net assets in two classes on the face of the statement of activities:

| With Donor Restrictions | Without Donor Restrictions |

|---|---|

| Contributions received with time/purpose stipulations | Unrestricted contributions, earned revenue, board-designated funds |

| Investment earnings on restricted endowments | Investment earnings on unrestricted assets |

| Released upon satisfaction of restrictions | Receives funds released from restrictions |

This format gives leadership and the board a clear, immediate view of which funds are available for discretionary use and which remain obligated.

Triggering a Release from Restriction

A release from restriction occurs when your organization satisfies the donor's time or purpose condition:

- Time restriction: The specified date or fiscal year arrives

- Purpose restriction: The funds are spent on the designated program or project

- Hybrid: Both time and purpose conditions are met

Once those conditions are met, the accounting mechanics follow a straightforward reclassification process.

Journal Entry for Releasing Restricted Funds

When a restriction is satisfied, record the following reclassification entry:

Debit: Net Assets With Donor Restrictions

Credit: Net Assets Without Donor Restrictions

Line item: Release from Restrictions

Key points:

- This is a reclassification entry, not a cash transaction—it does not affect cash flow

- The amount released appears on the statement of activities in both columns, showing the transfer between net asset classes

- No revenue is recorded at the time of release—revenue was already recognized when the contribution was received

To see how this works in practice, consider this scenario:

Example:

Your nonprofit receives a $50,000 grant for after-school tutoring. In month one, you spend $10,000 on tutoring salaries and supplies.

Journal entry:

- Debit: Net Assets With Donor Restrictions — $10,000

- Credit: Net Assets Without Donor Restrictions — $10,000

- Memo: Release from restriction for after-school tutoring expenses incurred in [month/year]

Documentation: The Non-Negotiable Foundation

Every restriction must be captured in writing through:

- Award letters from foundations or government agencies

- Donor correspondence specifying intent

- Signed pledge forms from capital campaigns

- Grant agreements detailing use restrictions

Auditors review these gift instruments to verify that disbursements align with donor stipulations. If a donor dispute arises, or if a state attorney general investigates, your documentation is your only defense. The National Council of Nonprofits recommends adopting a formal gift acceptance policy to govern how your organization receives and restricts contributions.

Best Practices for Managing Restricted Funds

Configure Accounting Software for Fund Tracking

Modern nonprofit accounting platforms support multi-dimensional tracking through class, project, or fund codes:

- QuickBooks Online for Nonprofits: Use class or location categories to segregate restricted funds

- Sage Intacct: Uses a "dimensions" system for multi-dimensional tracking (fund, grant, program, location)

- NetSuite for Nonprofits: Combines fund accounting, grant oversight, and donor tracking in a single cloud platform

Critical setup steps:

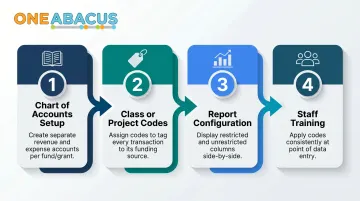

- Create a chart of accounts with separate revenue and expense accounts for each major fund or grant

- Assign class or project codes to tag every transaction to its funding source

- Configure financial reports to display restricted and unrestricted columns side-by-side

- Train staff to apply codes consistently at the point of data entry

Getting the chart of accounts right from the start prevents costly reconciliation later.

Budget Restricted Revenue First

When building your annual operating budget:

- Identify all known restricted contributions (grants, major gifts, capital pledges)

- Allocate those funds to their designated programs or purposes

- Calculate the remaining funding gap

- Assign unrestricted dollars to fill gaps, cover overhead, and build reserves

This sequence makes funding gaps visible early and prevents accidental overspending of unrestricted reserves.

Report Restricted vs. Unrestricted Funds Separately in All Board Reports

Board members need to understand which portion of net assets is truly available for strategic decisions. Don't wait for the annual audit—provide monthly or quarterly financial reports that present:

- Unrestricted net assets: Available for any mission-aligned use

- Board-designated net assets: Internally set aside but legally unrestricted

- Temporarily restricted net assets: Earmarked by donors for specific purposes or time periods

- Permanently restricted net assets: Endowment principal that must remain intact

This transparency ensures boards make informed decisions about hiring, program expansion, or reserve spending.

Schedule Regular Grant and Gift Compliance Reviews

At least quarterly, match actual spending against each restriction's terms:

- Flag unspent balances nearing grant deadlines

- Verify that expenses charged to restricted funds meet donor stipulations

- Document the rationale for each release from restriction before recording the journal entry

- Communicate with grantors proactively if spending timelines or purposes need adjustment

Regular reviews prevent year-end scrambles and ensure auditors find clean, well-documented records.

Partner with a Fractional CFO for Expert Financial Leadership

According to the National Council of Nonprofits' 2023 Workforce Survey, 74.6% of nonprofits reported job vacancies, and 72% struggle with turnover in finance and accounting roles.

For organizations without a full-time CFO, managing restricted funds correctly—while also handling budgeting, audit preparation, and board reporting—can overwhelm lean finance teams.

One Abacus Advisory provides the fractional CFO leadership nonprofits need to manage restricted funds correctly—without the cost of a full-time hire. Services include:

- Fund tracking, budgeting, and cash flow management

- Compliance documentation and audit preparation for restricted fund releases

- Accounting system configuration across NetSuite, Sage Intacct, and QuickBooks Online

- Board-ready reporting that clearly separates restricted from unrestricted assets

For example, One Abacus Advisory optimized the NetSuite environment for the Philadelphia Zoo during a leadership transition, improving month-end close processes and board reporting while ensuring compliance and accuracy. Similarly, they supported the San Diego Food Bank as interim financial leaders, maintaining stability and continuity during a finance director transition.

Both engagements demonstrate how right-sized financial leadership helps nonprofits stay compliant, audit-ready, and financially transparent—regardless of internal capacity.

Frequently Asked Questions

What is a restricted fund in accounting?

A restricted fund is a donor-imposed contribution earmarked for a specific purpose, time period, or both. Unlike unrestricted funds, which the organization can allocate at its discretion, restricted funds carry legally binding limitations. They appear on the balance sheet as "net assets with donor restrictions."

What are the three types of restrictions on funds?

The three types are unrestricted funds (no donor conditions), temporarily restricted funds (tied to a purpose or time period), and permanently restricted funds (endowments where the principal stays intact). FASB consolidates the last two categories under "net assets with donor restrictions."

How do you account for restricted funds in a nonprofit?

Restricted contributions are recorded as revenue when the unconditional promise or gift is received, not when spent. They are tracked in a separate "with donor restrictions" column on financial statements. Once the donor's time or purpose condition is satisfied, a reclassification entry moves the funds to "without donor restrictions."

What is the journal entry for releasing restricted funds?

When a restriction is satisfied, debit Net Assets With Donor Restrictions and credit Net Assets Without Donor Restrictions via a "Release from Restrictions" line item. This transfer between net asset classes does not affect cash flow.

Can a nonprofit invest or borrow from restricted funds?

Restricted funds cannot be borrowed or redirected without explicit donor consent. Endowment principal must remain intact under UPMIFA, which also requires donor consent, court approval, or a statutory notification process before any restriction can be modified.

Are grants considered restricted funds?

Most foundation and government grants carry programmatic or time conditions, making them temporarily restricted funds. If a grant also includes a performance barrier and a right of return, it is conditional and recorded as deferred revenue until that barrier is cleared.

Final Takeaway: Restricted fund management is a legal obligation and a governance imperative — not an optional best practice. Nonprofits that pair the right internal controls with experienced financial leadership are better positioned to honor donor intent, pass audits cleanly, and allocate resources where they matter most. If your organization is navigating complex funding environments, fractional CFO support from a firm like One Abacus Advisory can provide the oversight and documentation discipline to keep you on solid ground.