Introduction

Every nonprofit board faces an essential tension: cooperating closely with executive leadership to advance the mission while simultaneously controlling and overseeing that same leadership to protect the organization. This dual mandate—cooperation and control—is what makes nonprofit governance uniquely demanding and why so many organizations struggle to get it right.

Unlike for-profit companies with shareholders scrutinizing quarterly earnings, nonprofits must be self-correcting. Attorneys general are the primary regulators of nonprofits, but enforcement powers vary widely by state, and the IRS notes it cannot directly sanction governance failures under the Internal Revenue Code. This makes internal governance mechanisms more critical. When boards fail to understand this responsibility, charitable assets are mismanaged, missions drift, and public trust erodes.

This article is for nonprofit board members, executive directors, and organizational leaders who want to strengthen their governance practices.

What Is Corporate Governance in Nonprofit Organizations?

Corporate governance in the nonprofit context is the system of authority, accountability, and oversight that determines who makes decisions, how power is exercised, and how charitable assets are protected. It sits above day-to-day operations and below statutory law—the internal framework that translates legal obligations into organizational practice.

BoardSource defines the board of directors as "the governing body ultimately responsible for a nonprofit" with "specific legal and ethical responsibilities to the organization." The National Council of Nonprofits describes board members as "the fiduciaries who steer the organization towards a sustainable future by adopting sound, ethical, and legal governance and financial management policies."

Unlike for-profit governance, nonprofits have no shareholders to hold them accountable—no earnings calls, no stock price discipline. That absence of external market pressure makes internal governance mechanisms more critical, not less.

According to the National Committee for Responsive Philanthropy, "educated boards of directors are in all probability the strongest operational mechanisms of self-regulation in the sector."

Common misconceptions about board service:

- Board members are not fundraisers or cheerleaders

- They are not rubber stamps for management decisions

- Their legal role is oversight and strategic direction, not day-to-day operations

Understanding fiduciary duty is foundational. Board members hold charitable assets in trust for the public benefit. Every major decision—budget approvals, executive evaluations, major contracts—must be made in the organization's best interests, not in the personal interests of board members. That standard is what separates genuine governance from ceremonial oversight.

The Governance Structure: Who Holds Authority

Nonprofit governance typically follows a three-tier structure that defines where authority resides and how it flows through the organization:

- Board of Directors - ultimate governing authority

- Executive Director/CEO - operational leader

- Committees - focused sub-groups supporting both

Clarity of roles within this structure is foundational to both cooperation and control. When boundaries blur, governance breaks down.

The Board of Directors

The board is the primary governing body. It sets strategic direction, authorizes major transactions, oversees the executive, and bears fiduciary responsibility. According to the National Council of Nonprofits, when paid staff are in place, "board members provide foresight, oversight, and insight" rather than managing day-to-day operations.

Key board responsibilities:

- Hiring, supervising, and evaluating the CEO/executive director

- Approving annual budgets and major expenditures

- Ensuring the organization operates within its mission and legal requirements

- Monitoring financial health and organizational performance

Board independence is essential. Relationships that compromise independence—family ties to staff, business interests with vendors, dual roles as board member and employee—should be governed by a robust conflict of interest policy. According to BoardSource's 2021 Leading with Intent study, 96% of nonprofit boards now have written conflict of interest policies, and 97% require full board approval of the annual budget.

Good boards monitor and guide management — not run it.

The Executive Director and Management

The Executive Director or CEO translates the board's strategic direction into day-to-day execution. Management handles transactions, programs, staff supervision, and vendor relationships.

The executive also reports back to the board — providing transparency on financial performance, programmatic outcomes, and emerging risks.

BoardSource recommends that "the chief executive should be an ex officio, non-voting member of the board." This ensures the executive has voice and access without compromising the board's independence in oversight decisions—particularly when evaluating the executive's own performance.

When this separation blurs, governance suffers. Boards that delegate oversight to the executive — or executives who dominate board agendas — create gaps that committees and other controls can't easily fill.

Committees

Committees distribute oversight responsibilities and allow for deeper focus on specialized areas. The average nonprofit board has 4.1 standing committees, with the most common being:

- Audit/Finance (82% of boards)

- Governance/Nominating (71%)

- Executive Committee (61%)

Committees do focused work on behalf of the full board. However, authority still rests with the full board. Committees cannot bind the organization or make final decisions independently. BoardSource recommends that "the board's standing committee structure should be lean and strategic and complemented by the use of task forces" for time-limited projects.

The Cooperation Dimension: How Boards and Management Work Together

Cooperation is not optional in nonprofit governance. Mission delivery depends on the board and executive working together to set strategy, allocate resources, and adapt to challenges. Without genuine collaboration, organizations become paralyzed by tension or slip into governance theater—meetings that exist without meaningful engagement.

BoardSource identifies constructive partnership as the first principle of exceptional governance: "Exceptional boards govern in constructive partnership with the chief executive, recognizing that the effectiveness of the board and chief executive are interdependent."

What Productive Cooperation Looks Like

Genuine cooperation shows up in day-to-day governance practices:

- The board chair builds an agenda-setting process that includes management input without letting management dominate it — the board sets the governance agenda; management informs it

- The executive provides regular, candid reports on finances, programs, risks, and emerging challenges — information flows freely, not selectively

- Board members actively mentor, advise, and open doors for the executive rather than just critiquing performance

According to Leading with Intent 2021, 70% of CEOs identify the board chair as one of their top two "go-to" people for tough decisions — a strong signal of healthy cooperation.

Stakeholder Cooperation

Nonprofits must also cooperate with donors, beneficiaries, funders, and community partners. Governance structures should include mechanisms for stakeholder input — advisory councils, community feedback loops, and regular engagement. Decisions made without stakeholder context risk mission drift and loss of community trust.

Yet the data points to a real gap. Leading with Intent 2021 found:

- Only 32% of boards place high priority on "knowledge of the community served" during recruitment

- Only 28% prioritize "membership within the community served"

Boards that recruit without community context are building cooperation structures on shaky ground.

The Risk of Excessive Deference

Those same recruitment gaps create the conditions for another failure: boards that stop asking hard questions. When cooperation slides into a board that simply approves what management recommends, the oversight function disappears. Boards that are too small, too insular, or too deferential to a founder or executive represent a recurring governance failure.

True cooperation requires informed, engaged board members who ask hard questions—not passive cheerleaders. BoardSource reports that only 33% of nonprofits have board members actively involved in governance. When disengagement passes for deference, boards lose the one thing donors and regulators expect them to provide: independent judgment.

The Control Dimension: Oversight, Fiduciary Duties, and Accountability

The control function is where governance becomes legally enforceable. It is grounded in three fiduciary duties that apply to every board vote and oversight decision.

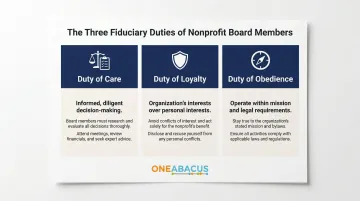

The Three Fiduciary Duties:

Duty of Care - Act with reasonable diligence and informed judgment. Board members must attend meetings, prepare conscientiously, and make decisions based on adequate information.

Duty of Loyalty - Prioritize the organization's interests over personal interests. This includes signing annual conflict-of-interest statements and recusing from discussions when conflicts arise.

Duty of Obedience - Ensure the organization operates within its stated mission and legal requirements. The IRS notes that organizations must be "organized and operated exclusively for exempt purposes" with assets dedicated to those purposes.

These duties are not aspirational. Violating them exposes individual directors to personal liability and puts the organization's tax-exempt status at risk. Financial oversight is where this exposure is most visible.

Financial Oversight as a Control Mechanism

Financial oversight is one of the board's most critical control responsibilities. This includes:

- Reviewing financial statements monthly or quarterly

- Approving annual budgets and monitoring budget-to-actuals

- Overseeing audits and ensuring restricted funds are used appropriately

- Understanding what the numbers mean, not just approving them

The board is not doing the accounting, but it must understand financial performance. According to Leading with Intent 2021, CEOs give their boards a grade of C+ for evaluating CEO performance and B- for financial oversight—indicating significant room for improvement.

Organizations that work with fractional financial leadership—such as One Abacus Advisory—can close this gap. A fractional CFO translates operational financials into the board-level reporting and policy frameworks that directors need to exercise real oversight.

Conflict of Interest and Self-Governance

Conflicts of interest undermine the control function. When a director has a personal or financial stake in a board decision, the organization's charitable purpose is at risk.

A formal conflict of interest policy is non-negotiable. It must require:

- Annual disclosure of potential conflicts, plus immediate disclosure as new situations arise

- Recusal from any discussion or vote where a conflict has been identified

- Votes taken only by disinterested board members, with the conflict documented in minutes

Without this, boards approve their own deals, compensation conflicts go unaddressed, and regulatory scrutiny follows. Leading with Intent 2021 found that 96% of boards have written conflict of interest policies, but having the policy is not enough—it must be enforced consistently.

Documentation and Accountability

Board meeting minutes are the evidentiary record of the control function in action. Proper minutes document:

- Who was present

- What was discussed

- What conflicts were disclosed

- How votes were cast

Regulators, auditors, and courts rely on minutes to confirm that governance authority was exercised. Absence of minutes or casual recordkeeping is treated as governance failure.

Form 990 is the IRS's primary tool for gathering information about tax-exempt organizations. What is disclosed on Form 990 defines how the IRS and the public view the organization. Nonprofits must make their three most recently filed annual returns publicly available—transparency is a legal requirement, not a courtesy.

The IRS asks nonprofits to confirm adoption of five key governance policies: Conflict of Interest, Whistleblower Protection, Document Retention/Destruction, Gift Acceptance, and Joint Venture (if applicable).

When Governance Breaks Down: Warning Signs and Common Failures

Governance failures follow predictable patterns. Understanding these warning signs can help boards course-correct before damage becomes irreversible.

Most Common Cooperation Failure: Deference to the Executive

Boards that are too deferential to the executive director or founder allow one individual to control the agenda, dominate meetings, and effectively determine their own oversight. The Charity Lawyer Blog's widely cited list of governance mistakes identifies "Deference to the Executive Committee, Board Chair, or CEO" as a top failure, stating: "It is no longer sufficient to rubber-stamp committee or staff recommendations or to simply abstain from dicey decisions."

Governance authority must reside at the board level as a body—not with any individual. When board members defer reflexively to a charismatic founder or long-tenured executive, the control function gradually disappears.

Most Common Control Failure: Disengagement from Financial Oversight

Boards that disengage from financial oversight—approving budgets without understanding them, missing warning signs in financial statements, or allowing restricted funds to be misused—create serious consequences: cash flow crises, regulatory action, and lost donor trust.

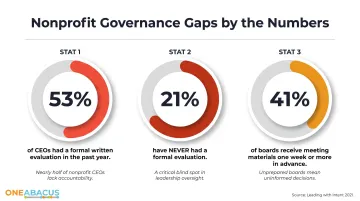

According to Leading with Intent 2021:

- Only 53% of CEOs had a formal written evaluation in the past year

- 21% have never had a formal evaluation

- Only 41% of boards receive meeting materials one week or more in advance

Each gap points to a board that has stepped back from its oversight role.

Founder's Syndrome

The transition from founder-led informal governance to institutional governance is where many nonprofits struggle. GBQ identifies founder's syndrome as characterized by "resistance to delegating key decisions or developing successor leadership."

Without clear role definitions and bylaw boundaries, boards shift their loyalty from the mission to the individual. That misalignment becomes a serious liability the moment leadership changes.

Real-World Governance Failures

Two high-profile cases illustrate what unchecked governance failures look like in practice.

National Rifle Association (NRA): In February 2024, a jury found the NRA failed to properly administer charitable funds and violated whistleblower protection laws. Wayne LaPierre was ordered to pay $5.4 million in damages and received a 10-year ban from the organization. The judge cited "a stunning lack of accountability."

Wounded Warrior Project (WWP): The WWP board fired both the CEO and CFO following public allegations of out-of-control spending and retaliation against employees who voiced concerns. BoardSource's Chief Governance Officer stated: "Governance is not a spectator sport! The work that nonprofits do and what's at stake is too important for the board to sit on the sidelines."

In both cases, the warning signs existed long before the crisis. Boards with active financial oversight and clear escalation protocols are far less likely to reach that point.

Strengthening Governance: Practical Strategies for Nonprofit Leaders

Strong governance comes down to documented practices, clear roles, and consistent execution — not just good intentions.

Foundational Governance Practices

Every nonprofit should have these baseline practices in place:

- Bylaws defining board authority, officer duties, term limits, and meeting requirements

- Conflict of interest policy with mandatory disclosure and recusal procedures

- Financial controls: regular budget reviews, audit oversight for organizations with $1M+ in revenue, and dual-signature spending authorizations

- Board meeting minutes that create an evidentiary record of governance decisions

Without these in place, everything else — strategic planning, executive oversight, donor accountability — sits on unstable ground.

Role Clarity and Board Composition

Boards should be composed of members selected for their ability and availability to govern—not only for their name recognition, wealth, or connection to the cause.

Diverse expertise strengthens both cooperation and control:

- Financial literacy (accounting, budgeting, audit oversight)

- Legal knowledge (compliance, contracts, employment law)

- Program expertise (understanding the work being funded)

- Community representation (voice of those served)

BoardSource recommends term limits to "avoid stagnation" and provide "a respectful and efficient method for removing unproductive members." The most common structure is two consecutive three-year terms. 71% of nonprofit boards have term limits.

High-profile figures or major donors who lack governance capacity are better served on advisory or honorary boards—not the governing board.

Bridging the Financial Reporting Gap

For many nonprofits, the gap between what the board needs to see and what management can produce is a significant governance challenge. Organizations experiencing growth, preparing for audits, or navigating leadership transitions often lack the internal capacity to deliver board-ready financial analysis.

Fractional financial leadership addresses this gap directly. One Abacus Advisory's CFO and COO services give nonprofits access to senior-level expertise on a right-sized basis, including:

- Board-ready financial reporting with clear, actionable insights

- Policy frameworks that strengthen internal controls and transparency

- Strategic analysis that supports informed decision-making

- Audit preparation and compliance support

This model supports both dimensions of governance: it gives management the expert capacity to perform, and gives boards the financial clarity they need for meaningful oversight — without the cost of a full-time C-suite hire.

Frequently Asked Questions

What are the main principles of corporate governance?

Five core principles guide nonprofit governance, each reoriented around mission fulfillment rather than shareholder return:

- Accountability — board oversight of organizational performance

- Transparency — public disclosure of Form 990 and financial statements

- Fairness — equitable treatment of all stakeholders

- Responsibility — fiduciary duty to mission and assets

- Ethical leadership — conflict of interest policies and whistleblower protections

What is the governance structure of a nonprofit organization?

The board of directors holds ultimate legal authority and oversight responsibility. The executive director or CEO manages day-to-day operations and reports to the board. Standing committees — typically 4–5, covering areas like finance/audit, governance/nominating, and executive functions — handle specialized oversight, but final authority always flows through the full board.

What is corporate governance as a system of controlling an organization?

Governance is the internal system of checks and balances—fiduciary duties, conflict of interest policies, financial oversight, and documented decision-making—that ensures authority is exercised responsibly and charitable assets are protected. It operates through transparency, accountability, and board independence to prevent mission drift and financial mismanagement.

What are the fiduciary duties of nonprofit board members?

Board members carry three primary legal duties:

- Duty of Care — informed, diligent decision-making based on adequate preparation

- Duty of Loyalty — prioritizing the organization's interests and disclosing personal conflicts

- Duty of Obedience — staying within the mission and legal requirements set by governing documents

How is nonprofit governance different from for-profit corporate governance?

The core differences come down to purpose and accountability structure:

- Nonprofits serve a public charitable mission, not shareholder returns

- Without market accountability, self-governance becomes the primary check on leadership

- Stakeholder relationships are more complex, spanning donors, beneficiaries, and the public

- A duty of obedience ties boards to their charitable purpose in ways for-profit boards aren't bound

Without shareholders to impose external discipline, nonprofit boards must be genuinely self-correcting.