Introduction

Should we approve all salaries? Can a board member give feedback directly to a program officer? Is it appropriate for the board to review the executive director's hiring plan for next quarter?

These questions surface constantly in nonprofit boardrooms, and the uncertainty behind them points to a real tension. Board members want to drive mission impact through smart people decisions — they know that talent determines whether strategic plans succeed or gather dust.

Yet most board members also sense that crossing certain lines risks undermining the executive director, confusing staff about reporting structures, and slowing the very operations they're trying to strengthen.

The answer is more straightforward than many boards expect: the board's HR role is real and meaningful, but it is defined by governance, not management. This article maps exactly where that boundary falls.

Whether you're navigating your first year on a nonprofit board or reassessing long-standing governance practices, here's what you'll come away with:

- Which six HR responsibilities belong squarely on the board's plate

- How to conduct executive director evaluations that actually drive performance

- Which policies require board-level approval — and which don't

- How to avoid the twin traps of micromanagement and abdication

Key Takeaways

- The board hires, evaluates, and sets compensation for the executive director — not other staff

- Day-to-day hiring, performance management, and team supervision belong entirely to the chief executive

- Boards must approve executive compensation with documented comparability data to satisfy IRS standards

- Most nonprofits lack written succession plans, leaving organizations exposed to avoidable leadership risk

- Micromanagement shortens executive director tenure — already just 5-7 years on average — while under-involvement invites compliance failures

Governance vs. Management: Setting the Right Boundaries

The Core Distinction

Governance is the board's collective function of setting strategic priorities, ensuring accountability, and approving policy. Management is the executive director and staff's function of implementing those priorities in daily operations. The board governs; the chief executive manages. This boundary is the foundation for every HR decision the board makes.

In HR terms, governing means:

- Making collective decisions about executive leadership

- Approving high-level compensation structures with market benchmarking

- Ensuring the organization has the human capital strategy to fulfill its mission

- Holding the chief executive accountable for building and managing an effective team

Governing does not mean directing individual staff members, approving every hire below the executive level, or reviewing performance improvement plans for program officers.

What Management Looks Like — and Why Boards Must Stay Out

Day-to-day staffing decisions belong to the chief executive: conducting interviews, negotiating salaries for staff positions, providing performance feedback, resolving internal conflicts, managing schedules, and implementing disciplinary processes. When boards blur this line, three problems emerge:

- Staff confusion about who actually supervises them

- Executive director undermining that erodes leadership credibility

- Delayed decisions as operational matters wait for board meeting cycles

If the chief executive requests board member involvement in hiring a senior role (CFO, COO), board members may assist in an advisory capacity only — the final hiring decision still belongs entirely to the executive.

Individual Board Members Have No HR Authority

Only the full board, acting collectively through majority vote at a properly conducted meeting or by unanimous written consent, has governance authority. An individual board member has no management authority based on their position alone. A board member who individually counsels a staff member about their performance or pressures a hiring decision is acting outside their governance role — and may expose the organization to legal risk under the "apparent authority" doctrine.

Staying within the governance role also protects board members personally. The business judgment rule shields directors from personal liability for decisions made in good faith with a reasonable basis. That protection applies only to decisions made within the board's proper governance function — not to operational overreach.

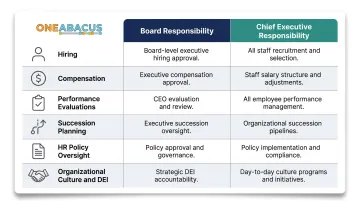

Six HR Responsibilities That Belong to the Board

The board has clear, legitimate responsibility in exactly six HR areas:

| HR Area | Board Responsibility | Chief Executive Responsibility |

|---|---|---|

| Hiring | Recruit and select the executive director | Hire and manage all other staff |

| Compensation | Negotiate executive package; approve high-level compensation philosophy | Develop and implement staff compensation plans |

| Performance Evaluations | Conduct formal annual review of the executive director | Evaluate all other staff |

| Succession Planning | Ensure written plan exists for executive and critical roles | Develop internal leadership pipeline |

| HR Policy Oversight | Approve governance-level policies (conflict of interest, whistleblower, code of ethics) | Create, update, and implement employee handbook and operational policies |

| Organizational Culture & DEI | Set strategic tone and expectations | Implement culture initiatives and monitor day-to-day climate |

Hiring the Executive Director

This is the single most consequential HR decision the board makes. The board owns the full process:

- Defining qualifications tied to the strategic plan

- Conducting the search (often through a search committee)

- Interviewing finalists

- Negotiating the employment contract and compensation package

- Establishing clear performance expectations from day one

The board should formalize this relationship with a written employment agreement that specifies compensation, evaluation timeline, benefits, expectations, and termination terms.

Executive Performance Evaluation

Approximately 40% of nonprofit boards skip structured annual performance reviews — one of the most commonly neglected board responsibilities. The board must conduct a formal, documented evaluation every year that includes:

- Clear goal-setting tied to the strategic plan

- Executive director self-assessment against agreed goals

- Structured feedback from board members (and optionally, direct reports via 360-degree input)

- Year-end evaluation conversation

- Documentation that feeds directly into compensation decisions

This is not a single meeting in December. Effective evaluation requires regular check-ins throughout the year and begins with collaborative goal-setting in the first quarter. Strong evaluation processes also surface the leadership continuity questions that succession planning must answer.

Succession Planning

The board must ensure a written succession plan exists for the executive director and other critical leadership roles. Only 27% of nonprofits have one — leaving organizations dangerously exposed when transitions occur.

A basic succession plan covers:

- Who steps in if the executive director departs suddenly (interim protocols)

- Internal candidates worth developing for future leadership roles

- How institutional knowledge gets documented and transferred

- A clear timeline and process for planned transitions

This is a governance function because the board holds ultimate accountability for organizational continuity. The chief executive can assist in identifying internal talent, but the board owns the plan itself.

Organizational Culture and DEI Strategy

The board sets the cultural expectations the organization is held to — not by managing daily team dynamics, but by defining standards and holding leadership accountable to them. Specifically, the board should:

- Approve diversity, equity, and inclusion goals aligned with mission

- Monitor progress through periodic reporting

- Model inclusive governance practices in its own composition and processes

- Hold the executive director accountable for creating a healthy workplace culture

Board composition, turnover rates, and staff climate surveys are all data points a governance-minded board should review annually. How a board governs culture is inseparable from how well the organization fulfills its mission.

Hiring and Evaluating the Executive Director

The board's relationship with the executive director is a full lifecycle responsibility: recruit, onboard, support, evaluate, compensate, and when necessary, transition. Getting each stage right protects the organization and sets the executive director up to lead effectively.

The Executive Director Hiring Process

Best practices include:

Search committee: Form a group of 3-5 board members with diverse perspectives; consider an executive search firm for organizations with budgets above $2 million or mission-critical transitions

Success criteria: Define what the next leader needs to accomplish, tied directly to your strategic plan — including the experience, skills, and leadership style that fit your organizational stage

Compensation benchmarking: Research comparable roles at organizations of similar size, mission, and geography; this comparability research is a legal requirement under IRS standards (see below)

Employment agreement: Put the terms in writing before the hire begins, covering:

Compensation (salary, benefits, bonuses, retirement contributions)

Performance expectations and evaluation timeline

Termination terms (notice period, severance provisions)

Conflict-of-interest acknowledgment

Conducting a Meaningful Annual Performance Review

BoardSource recommends a structured process across six performance categories:

- Agency-wide program development

- Administration and HR management

- Community relations

- Financial management

- Fundraising

- Board relations

Use a consistent rating scale (e.g., Remarkable, Satisfactory, Needs Improvement, Unknown). The process should unfold in stages:

- Self-assessment: Executive director submits written reflection against agreed goals

- Board input: Executive or governance committee gathers feedback from all board members

- Feedback conversation: Board chair (or committee chair) holds structured discussion with the executive director

- Documentation: Results are recorded in writing and filed in personnel records

- Compensation decision: Evaluation findings feed directly into the next year's compensation package

Feedback should flow year-round, not only at annual review time. Schedule quarterly check-ins between the board chair and executive director to address concerns early and acknowledge progress against goals.

IRS Rebuttable Presumption: Documenting Executive Compensation

Those compensation decisions — including the benchmarking research behind them — also carry a legal documentation obligation. For tax-exempt organizations, the IRS applies the rebuttable presumption standard to executive compensation under Section 4958. Boards that meet three specific requirements are presumed to have set reasonable compensation:

| Requirement | What It Means |

|---|---|

| Independent approval | Compensation approved in advance by a board or committee composed entirely of individuals without conflicts of interest |

| Comparability data | The approving body reviews appropriate market data before deciding |

| Contemporaneous documentation | The basis for the decision is documented in writing at the time the decision is made |

Skip any of these three steps, and your organization loses the presumption. The IRS can then challenge the compensation as excessive, triggering intermediate sanctions penalties: a 25% excise tax on the executive for excess benefits (rising to 200% if uncorrected), plus up to $20,000 per transaction for board members who knowingly approved it.

Where to Find Comparability Data:

- GuideStar/Candid compensation reports

- State nonprofit association salary surveys (many states publish annual data)

- Professional compensation consultants

- IRS Form 990 filings from peer organizations (publicly available)

Staying on the right side of Section 4958 requires more than good intentions — it requires systems. One Abacus Advisory's fractional CFO services help nonprofit boards track executive compensation costs, benefits budgets, and overall compensation spending in ways that satisfy fiduciary obligations, without pulling board members into operational payroll details.

HR Policies and Benefits: What the Board Should Oversee

The Right Level of Policy Involvement

The board should not approve every line of the employee handbook. Personnel policies covering vacation accrual, remote work protocols, performance review cycles, and similar operational matters belong to management.

That said, **certain governance-level policies require explicit board approval**:

- Conflict-of-interest policy — requires board members and staff to formally disclose and manage conflicts

- Whistleblower/anti-retaliation policy — ensures employees can report illegal or unethical conduct without fear of reprisal

- Adopt a code of ethics that sets clear behavioral expectations for both board and staff

- Maintain a document retention and destruction policy aligned with legal recordkeeping obligations

These policies appear directly on IRS Form 990 Part VI, where their presence or absence becomes public information. While the IRS doesn't legally require them to maintain tax-exempt status, their absence signals weak governance to regulators, donors, and the public.

Best practice: Management should provide the board with an annual summary or index of key HR policies, flagging any significant updates, rather than requiring line-by-line board review of every policy change.

Benefits and Retirement Plan Oversight

Changes to employee benefits are typically reviewed by the board **as part of the annual budget process**, not approved individually. The board should see aggregate benefits costs and understand how compensation packages (including benefits) compare to market rates.

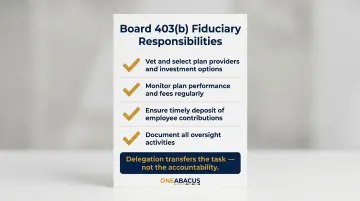

403(b) retirement plans carry unique board responsibilities. These plans are subject to ERISA fiduciary standards for most nonprofits, requiring the board to:

- Carefully vet and select plan providers and investment options

- Monitor plan performance and fees regularly

- Ensure employee contributions are deposited within required timelines (typically within 15 business days; 7-day safe harbor for plans under 100 participants)

- Document oversight activities

Even if the board delegates plan administration to a committee or third-party provider, the board retains fiduciary responsibility to monitor those delegates. Fiduciaries who breach these duties may be held personally liable to restore losses — delegation transfers the task, not the accountability.

Grievance Escalation: When the Board Gets Involved

The board should not serve as a default escalation point for staff grievances. Day-to-day personnel complaints belong to the executive director and any HR function the organization maintains.

However, the board (typically the board chair or audit committee) becomes the designated recipient when:

- The grievance involves the executive director personally

- A third-party hotline or external reporting mechanism is in place for serious concerns (fraud, harassment, legal violations)

Without a written escalation policy, serious complaints risk falling through the cracks — or landing on the wrong desk entirely. Defining these pathways in advance protects both staff and the organization.

Common Mistakes: When Board HR Involvement Goes Too Far or Not Far Enough

The Over-Involvement Trap

Boards that try to approve all hires, review salary decisions below the executive level, or direct staff performance improvement plans create serious operational problems:

- Slower hiring cycles that cause the organization to lose top candidates

- Staff confusion about reporting lines and authority

- Executive director burnout from constant second-guessing

Research shows that micromanagement negatively impacts executive director tenure and organizational effectiveness. When boards blur governance and management boundaries, talented chief executives leave. Average sector-wide ED tenure is just 5 to 7 years, with board conflict named as one of the top three drivers of departures.

BoardSource offers six criteria for determining when a matter warrants board involvement. A decision should come to the board if it is:

- Permanent — affects the organization beyond the current year

- Directional — shapes the organization's strategic course

- Controversial — contentious with stakeholders or the community

- Positional — involves the public stance of the organization

- Essential — touches mission, vision, or core values

- Financial — represents a significant departure from the approved budget

If a staffing decision doesn't meet at least one of these criteria, it belongs to the executive director.

The Under-Involvement Risk

Over-involvement gets most of the attention, but abdication carries its own risks. Boards that step back entirely from HR governance — especially around executive director performance and compensation — expose the organization to:

- Mission drift when the executive director lacks clear, board-approved goals

- IRS compliance issues (private benefit concerns when executive compensation isn't documented with comparability data)

- Sudden leadership crises with no succession plan in place

One common pattern: a board discovers serious HR and administrative problems only after a long-tenure executive departs. Years of deferred oversight leave behind compliance gaps, unclear policies, and operational chaos that can take months to unravel. Under-involvement often feels like trusting the executive director. Without verification, though, that trust is indistinguishable from neglect.

Diagnostic: Is Your Board in the Right Zone?

Ask yourself these four questions:

- Do we have a documented, structured process for evaluating the executive director annually?

- Has the board formally approved a conflict-of-interest policy, whistleblower policy, and code of ethics within the last 12 months?

- Does a written succession plan exist for the executive director (both emergency and planned transition scenarios)?

- Are we receiving compensation benchmarking data from comparable organizations before approving executive pay?

If you answered "no" to any of these, your board is under-involved in its core HR governance responsibilities.

Frequently Asked Questions

Who holds board members accountable?

Nonprofit board members answer to state charity regulators (typically the Attorney General's office), the IRS for tax-exempt compliance, and ultimately the public and donors. Internal mechanisms — bylaws, peer evaluation, and term limits — reinforce that accountability within the board itself.

What are the 5 responsibilities of a board member for a nonprofit?

The five core responsibilities are:

- Setting strategic direction

- Ensuring financial oversight and sustainability

- Hiring and evaluating the chief executive

- Ensuring legal and ethical compliance

- Supporting and advocating for the mission

All five flow from the legal duties of care, loyalty, and obedience.

Should a nonprofit board member be involved in staff hiring decisions?

Board members should not make or direct hiring decisions for staff below the chief executive. If the executive director invites a board member to assist in recruiting for a senior role, that member may offer input, but final hiring authority rests with the chief executive.

What are the HR policies for nonprofit organizations?

Core HR policies cover conflict of interest, anti-harassment, whistleblower protections, compensation, performance management, and code of conduct. The board approves governance-level policies (conflict of interest, whistleblower, code of ethics); all operational policies are management's responsibility.

What is the difference between board governance and management in a nonprofit?

Governance is the board's collective function of setting strategic priorities, ensuring accountability, and approving policy. Management is the executive director and staff's function of implementing those priorities in daily operations. The board governs; the staff manages.

What are the 7 main principles of HR?

The seven principles are staffing, development, compensation, benefits, employee relations, safety/compliance, and performance management. Nonprofit boards interact most directly with compensation, compliance, and chief executive hiring and evaluation; the remaining principles fall under the executive team's day-to-day responsibility.