Introduction

Many nonprofit boards are earnest about oversight — but unclear on which structural model actually fits their organization's size, stage, and mission. Without that clarity, boards end up with real consequences: role confusion between staff and directors, accountability gaps, or executive directors left without meaningful guidance. The structural question rarely gets answered directly.

This guide cuts through the generic advice by covering the five core nonprofit governance models, how to choose between them, the legal and financial duties every board must fulfill, and what stronger oversight actually looks like in practice.

Key Takeaways

- Nonprofits can adopt one of five governance models: Advisory, Cooperative, Policy (Carver), Patron, and Management Team

- Model selection depends on leadership structure, organizational stage, and operational capacity — no single model fits every organization

- All boards share three legal duties: Duty of Care, Duty of Loyalty, and Duty of Obedience

- Financial oversight — including budget approval, audit review, and Form 990 review — is required under every governance model

- Boards should revisit their governance model fit regularly as organizations grow and change

What Is Nonprofit Board Governance?

Nonprofit board governance is the system of structures, policies, and processes through which a board of directors provides strategic direction, oversight, and accountability for the organization. The National Council of Nonprofits defines board members as "fiduciaries who steer the organization towards a sustainable future by adopting sound, ethical, and legal governance and financial management policies."

Governance vs. Management: Knowing the Difference

The National Council of Nonprofits draws a clear distinction: boards "provide foresight, oversight, and insight," while the CEO or executive director "runs the day-to-day management activities." Governance answers what the organization should achieve and why—setting direction, approving policies, ensuring mission alignment. Management determines how to execute operationally.

Boards that "steer the boat by managing day-to-day operations" when paid staff are in place blur this critical boundary. The result is often confusion, duplication of effort, or executive directors who feel micromanaged.

Why Nonprofit Governance Carries Extra Weight

That governance-management boundary matters even more in nonprofits because the stakes extend beyond the organization itself. Nonprofit boards are stewards of public trust, charitable resources, and tax-exempt status — obligations that for-profit boards simply don't carry.

The IRS explicitly states that "a well-governed charity is more likely to obey the tax laws, safeguard charitable assets, and serve charitable interests than one with poor or lax governance." In practice, this means boards must actively maintain:

- Transparency in financial reporting and decision-making

- Accountability to donors, regulators, and the communities they serve

- Compliance with federal and state requirements tied to tax-exempt status

These aren't aspirational ideals. They're the baseline for protecting the organization's credibility and operating license.

The 5 Nonprofit Board Governance Models

Choosing the wrong governance model doesn't just create internal friction — it can leave critical decisions unmade, blur accountability lines, and strain the relationship between board and staff. Each of these five models reflects a different answer to the same core question: who holds authority, and how is it exercised?

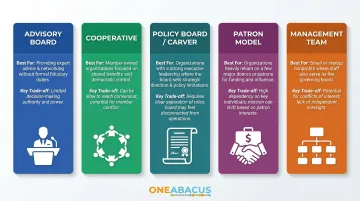

| Model | Best For | Key Trade-off |

|---|---|---|

| Advisory Board | Early-stage or founder-led nonprofits | Expertise without authority — effectiveness depends on member engagement |

| Cooperative | Small, volunteer-driven collectives | Democratic but slow; one disengaged member can stall decisions |

| Policy Board (Carver) | Mid-to-large nonprofits with professional staff | Clean oversight structure, but boards that disengage miss critical issues |

| Patron | Organizations reliant on major donor networks | Fundraising strength, but governance gaps if oversight isn't reinforced |

| Management Team | Small nonprofits without full-time staff | Leverages board skills well, but risks micromanagement when staff exist |

Advisory Board Model

An advisory board is a group of subject-matter experts who provide professional guidance to the CEO or governing board — without holding formal decision-making authority. Organizations typically use them to add credibility, specialized knowledge, or donor connections.

The catch: effectiveness hinges on whether members are genuinely committed to the mission. A board assembled for name recognition rather than engagement quickly becomes a letterhead list rather than a working resource.

Best for: Early-stage or founder-led nonprofits needing expert counsel but not yet ready for a full governing board.

Cooperative Governance Model

In a cooperative model, there is no CEO — the board governs by consensus, with all members sharing equal responsibility and liability. It's the most peer-driven structure of the five.

It works well for grassroots organizations with tight-knit, mission-committed teams. The vulnerability is that equal accountability requires equal engagement; one disengaged member creates gaps that the entire group absorbs.

Best for: Small, volunteer-driven organizations with strong commitment and collaborative cultures.

Policy Board (Carver) Model

Developed in the 1970s by John Carver, Policy Governance draws a firm line between strategy and operations. The board sets "Ends" (the long-term outcomes it expects) and "Executive Limitations" (the boundaries within which the CEO operates), then monitors compliance — not activity reports.

Carver's framework holds that "governance is a downward extension of ownership rather than an upward extension of management." In practice, this means boards stop reviewing program details and start holding the CEO accountable to defined results.

The model gained traction in the 1980s–90s because it gave boards a principled reason to stay out of operations. Its real risk is the inverse: when boards disengage too fully, they lose the visibility needed to catch financial or leadership problems before they escalate.

Best for: Mid-to-large nonprofits with professional staff and strong executive leadership.

Patron Governance Model

In a patron model, board seats are filled based on personal wealth, philanthropic networks, or fundraising capacity. Members contribute primarily through financial support and donor cultivation — not policy decisions or operational oversight.

This trade-off is deliberate: organizations gain fundraising reach and visibility in exchange for lighter governance involvement. The risk is that without a parallel oversight structure, strategic and financial accountability can erode quietly.

Best for: Organizations heavily reliant on major donor networks and needing external visibility.

Management Team Model

The management team model organizes the board into functional committees — finance, HR, programs, fundraising — that mirror a staff org chart. It's common in volunteer-heavy nonprofits where board members fill operational gaps that paid staff otherwise would.

Where it breaks down: once a nonprofit hires professional staff, these same committee structures tend to generate role confusion and micromanagement. The model requires deliberate boundary-setting as the organization grows.

Best for: Small-to-mid-size nonprofits where board members perform hands-on work, or volunteer-driven organizations without full-time staff.

How to Choose the Right Governance Model for Your Nonprofit

Model selection should be driven by three key factors:

- Organizational stage (startup vs. mature)

- Leadership structure (CEO/ED in place or not)

- Operational capacity (how much paid staff can cover)

Avoid choosing a model based solely on what's familiar or what other nonprofits use.

Practical Decision Framework

| Organizational Profile | Best-Fit Model | Why It Works |

|---|---|---|

| No CEO in place | Cooperative | Board shares decision-making and operational work |

| Strong executive leadership | Carver | Board sets policy; CEO owns operations |

| Fundraising is the priority | Patron board | Members open doors and cultivate major donors |

| Volunteer-driven operations | Management team | Board contributes functional expertise (finance, HR, programs) |

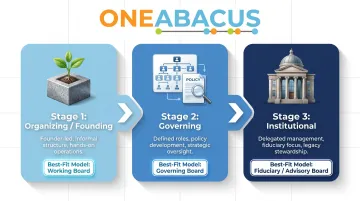

Board Lifecycle Stages

BoardSource's "Board Passages" framework identifies three distinct lifecycle stages that boards move through as organizations grow:

| Stage | Characteristics | Best-Fit Model |

|---|---|---|

| Stage 1: Organizing/Founding | Board handles day-to-day work; governance and management overlap | Cooperative or management team |

| Stage 2: Governing | Board separates oversight from operations; committees formalize | Carver or patron model |

| Stage 3: Institutional | Board owns strategy, audits, budget approval, and CEO evaluation | Carver model |

Using Hybrid Models

Nonprofits often combine elements of two models. For example, a Carver-style policy board may add a separate advisory council for subject-matter expertise, or a patron board may establish a finance committee that operates more like a management team board.

When integrating models, clarify which body holds decision-making authority and which provides advisory input. Accountability gaps emerge when roles overlap without clear boundaries.

Revisit Your Model as You Grow

The same clarity that matters in hybrid models applies broadly: a governance structure that fit your organization at founding may no longer serve it as staff, budget, and complexity grow. Bridgespan recommends that boards "revisit their board composition matrix annually, looking three to five years ahead of current strategy," and "step forward during times of crisis or change and step back when appropriate."

Build a governance review into your annual planning cycle — not as a formality, but as a check on whether your current model still matches your operational reality.

Legal Duties and Financial Responsibilities of Nonprofit Boards

Regardless of governance model, all nonprofit board members hold three core legal duties grounded in state corporate statutes and federal tax compliance expectations.

The Three Legal Duties

| Duty | Definition | Key Obligation |

|---|---|---|

| Duty of Care | Act with reasonable diligence and informed judgment, exercising the care that an ordinarily prudent person would in a similar position | Attend meetings, review materials, ask questions, make informed decisions |

| Duty of Loyalty | Prioritize the organization's interests over personal gain and manage conflicts of interest | Disclose conflicts, recuse from conflicted decisions, act in the organization's best interest |

| Duty of Obedience | Ensure the organization adheres to its stated mission and applicable laws | Maintain mission alignment, ensure compliance with bylaws, laws, and regulations |

These duties are confirmed by BoardSource, the National Council of Nonprofits, and the IRS.

Core Financial Oversight Responsibilities

Boards must:

- Approve annual budgets and monitor financial performance against those budgets

- Review financial statements regularly to ensure prudent use of assets

- Oversee audits or financial reviews, including reviewing auditor's letters and finance committee reports

- Review IRS Form 990 before filing, as encouraged by the IRS

Yet BoardSource's 2021 Leading with Intent report found that only 62% of nonprofit boards give full board approval of the IRS Form 990 before filing. Nearly 4 in 10 boards skip this critical oversight step, exposing organizations to compliance risk.

Required Governance Policies

The IRS encourages adoption of three specific governance policies, which Form 990 Part VI asks about:

- Conflict of Interest Policy: Requires written procedures for identifying and managing conflicts, ensuring directors act solely in the charity's interests

- Whistleblower Protection Policy: Gives employees a confidential path to report suspected financial impropriety or misuse of resources

- Document Retention and Destruction Policy: Sets standards for document integrity, retention schedules, and destruction, including electronic files

Form 990 Part VI asks about all three. Boards that haven't formalized these policies face both compliance exposure and reputational risk.

Executive Compensation and the Rebuttable Presumption

Boards must approve and document executive compensation as reasonable and not excessive. Under IRC Section 4958, the IRS can impose excise taxes on "disqualified persons" who receive excess benefit transactions.

The rebuttable presumption of reasonableness is established when:

- An authorized body free of conflicts approves compensation in advance

- That body reviews and relies on appropriate comparability data

- The basis for the decision is documented at the time it's made

The Financial Clarity Challenge

Many smaller nonprofits struggle with financial oversight not because boards lack commitment, but because they lack timely, clear financial reporting. When nearly 40% of boards can't confirm they're reviewing the Form 990 before it's filed, the issue is often infrastructure — not intention.

Fractional CFO services, such as those provided by One Abacus Advisory, address this gap directly. Rather than hiring a full-time finance executive, boards gain access to audit preparation, compliance support, and board-ready financial reporting scaled to the organization's actual needs.

Nonprofit Board Governance Best Practices

Strong governance is built deliberately: through clear role definition, regular evaluation, and structures that hold up under pressure.

Clearly Define Roles and Expectations

Boards that articulate expectations upfront dramatically reduce conflicts of interest, disengagement, and overreach. Key tools include:

- Written governance policy documents that outline board member responsibilities, committee structures, and decision-making processes

- Structured onboarding for new board members, including orientation to mission, financials, programs, and governance policies

- Job descriptions for board roles, including officer positions and committee chairs

Build in Regular Evaluation Loops

Strong boards don't wait for crises to assess performance. They build evaluation into their annual cycle:

Board Self-Assessments: BoardSource recommends that boards conduct formal self-assessments at least every two years. Yet only 47% completed one in the prior two years, and approximately one-third have never conducted a self-assessment.

Self-assessments typically examine:

- Board composition and skills gaps

- Meeting quality and participation

- Financial oversight effectiveness

- Strategic alignment with mission

- The board's overall effectiveness relative to its own expectations

Executive Director Performance Reviews: Annual or biennial reviews ensure accountability and create structured opportunities for feedback and professional development — a step many boards skip until a problem surfaces.

Periodic Governance Audits: Review bylaws, policies, and committee structures to catch gaps before they become crises. BoardSource's Board Passages resource recommends reviewing bylaws every few years to confirm they reflect current practices and specify term lengths for orderly leadership rotation.

Common Governance Pitfalls to Avoid

Proactive evaluation helps — but knowing what to watch for matters just as much. A 2022 systematic review in Nonprofit and Voluntary Sector Quarterly analyzed 71 empirical articles on nonprofit scandals from 1990 to 2021 and identified recurring failure patterns:

- Recruiting for prestige over mission fit — 49% of chief executives said they did not have the right board members to "establish trust with the communities they serve"

- Letting one dominant voice override consensus — effective governance depends on diverse perspectives and distributed accountability, not a single authority

- Weak financial literacy on the board — without it, members cannot fulfill their duty of care, regardless of how strong other controls are

- Outdated bylaws — when bylaws go unreviewed for years, confusion grows around authority, term limits, and decision-making processes

- Board disengagement or role ambiguity — absent boards, unclear mandates, and unchecked authority delegation are recurring factors in nonprofit scandals

The same review found that 80% of governance measures studied were not associated with preventing fraud — a reminder that standard internal controls are insufficient without engaged, informed board oversight.

Frequently Asked Questions

What are the three legal duties of nonprofit board members?

The three legal duties are the Duty of Care (act with reasonable diligence), Duty of Loyalty (prioritize the organization's interests over personal gain), and Duty of Obedience (ensure adherence to mission and applicable laws). All three apply regardless of which governance model a board uses.

Who holds a nonprofit board of directors accountable?

Nonprofit boards are accountable to state attorneys general (who oversee charitable organizations), the IRS (through Form 990 reporting), donors and funders, and ultimately the public they serve. Form 990 is a public document, enabling transparency and external oversight.

What is the governance committee for a nonprofit board?

A governance committee is a standing board committee (typically 3-5 members) responsible for board recruitment, onboarding, performance evaluation, and ensuring governance policies remain current. Approximately 50% of nonprofit boards do not have a committee dedicated specifically to governance.

What is generative governance for nonprofit boards?

Generative governance is a mode of board engagement—beyond fiduciary and strategic roles—where the board engages in open-ended inquiry and meaning-making to shape organizational direction. It involves asking "why" and "what if" questions rather than only reviewing reports or approving decisions.

What are the 4 P's of governance for nonprofit boards?

The 4 P's framework—Purpose, People, Process, Performance—evaluates governance effectiveness by examining mission clarity, board composition, decision-making soundness, and measurable accountability standards. It's a practical diagnostic tool boards can use during annual self-assessments.

How do you write a report for a nonprofit board of directors?

A strong board report is concise and organized around strategic priorities: a financial summary (budget vs. actual), program updates tied to mission outcomes, key risks requiring decisions, and relevant KPIs. Every section should support informed oversight, not just document activity.

Final Thoughts

The right governance model doesn't just organize a board—it determines whether that board can actually advance the mission. Understanding the five core models, testing them against your organization's stage and culture, and revisiting the fit as you grow is how boards move from well-intentioned to genuinely effective. Governance isn't a one-time setup. It's an ongoing commitment to the people and communities your organization serves.