Introduction

Many nonprofit board members hold fiduciary responsibility for their organization's finances yet receive little to no training on how to read or assess the financial systems beneath the reports handed to them at quarterly meetings.

That knowledge gap creates real risk. When board members can't evaluate the quality of financial infrastructure, they can't ask the right questions — and they can't catch problems early enough to act.

The way a nonprofit structures its accounts — its chart of accounts, fund designations, and internal controls — directly shapes what the board can and cannot see. A poorly built account structure produces incomplete or misleading reports, making oversight nearly impossible. A well-built one gives the board the clarity to govern effectively, spot emerging issues early, and make informed strategic decisions.

This guide covers:

- The building blocks of nonprofit account structures

- How fund accounting works in practice

- Which financial reports boards should consistently request

- How to spot warning signs before they become crises

Key Takeaways

- The chart of accounts determines what questions boards can ask and get answered — vague structures hide critical information

- Fund accounting separates restricted and unrestricted funds — boards must actively oversee this to prevent compliance violations

- Boards need four core statements: activities, financial position, cash flows, and functional expenses

- Internal controls like separation of duties must be embedded in account structure, not treated as a staff-only concern

- Fractional CFO support provides the strategic infrastructure boards need when complexity outpaces internal capacity

What Is a Nonprofit Chart of Accounts and Why Should Boards Care

A chart of accounts (COA) is a structured, numbered list of every financial category an organization uses to record transactions. Its design determines what questions a board can ask — and actually get answered from the data on hand.

Why Structure Matters

A vague or overly simplified COA makes it impossible to track performance by program, funding source, or location. For example, if all donations are recorded in a single "Contributions" account, the board can't see which programs attract donor support or whether restricted gifts are being properly tracked. A well-structured COA enables reporting by program, funder, and restriction type that supports both governance oversight and operational management.

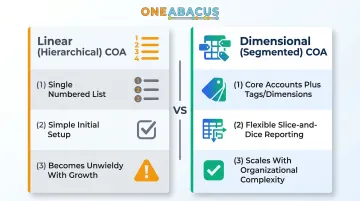

Two Structural Approaches

Nonprofits typically use one of two COA structures:

- Linear (hierarchical) COA: Embeds all account information into a single numbered list. Simple to set up but becomes unwieldy as organizations grow — tracking expenses across multiple programs, locations, and funding streams can generate thousands of unique account codes

- Dimensional (segmented) COA: Uses tags or dimensions to separate context from core accounts. Organizations maintain a simpler core account list while enabling flexible "slice and dice" reporting by program, location, department, or funding source

The Five Core Categories

Every nonprofit COA follows this basic structure:

| Category | Typical Numbering | What It Tracks |

|---|---|---|

| Assets | 1000s | Cash, receivables, property, investments |

| Liabilities | 2000s | Accounts payable, loans, deferred revenue |

| Net Assets | 3000s | Organizational equity split by restriction type |

| Revenue | 4000s-5000s | Donations, grants, program fees, investment income |

| Expenses | 6000s-9000s | Personnel, occupancy, program costs, administration |

The Board's Oversight Role

That taxonomy only serves governance if it maps to how your organization actually operates. Boards don't need to build or maintain the COA, but they should verify it reflects current programs and funding sources — not the structure the organization had five years ago. GAAP doesn't mandate a specific COA format, but nonprofits must structure accounts to support GAAP-required reporting and crosswalk to Form 990 categories.

Questions Boards Should Ask

- Does our COA allow us to track revenue and expenses by program, not just organization-wide?

- Can we produce fund-specific spending reports on request, or does staff need days to compile that information?

- Has the COA been reviewed recently?

Fund Accounting: How Restricted and Unrestricted Funds Work

Unlike for-profit businesses, nonprofits regularly receive funds tied to specific conditions — a donor designates money for a particular program, or a grant covers only certain expenses. Fund accounting is the system that tracks whether those conditions are actually being honored.

Understanding Net Asset Categories

FASB ASU 2016-14, effective for fiscal years beginning after December 15, 2017, replaced three net asset categories with two:

- Without donor restrictions: Funds available for any organizational purpose (formerly "unrestricted")

- With donor restrictions: Funds subject to time or purpose limits, including endowments where only earnings can be spent (formerly "temporarily restricted" and "permanently restricted")

This matters when reading modern financial statements — the terminology changed, but the underlying tracking requirement remains the same.

The Fiduciary Risk

Using restricted dollars for general operations — even unintentionally — can trigger serious consequences. Board oversight means verifying that tracking systems exist, not assuming staff has it covered:

- Donor complaints and loss of future support

- Grant clawbacks requiring return of funds

- IRS penalties or loss of tax-exempt status

- State law violations under charitable trust regulations

- Reputational damage that erodes fundraising capacity

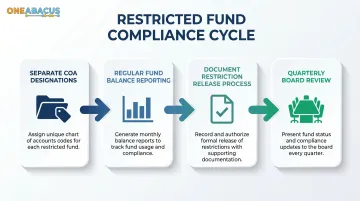

Proper Tracking in Practice

Understanding that risk makes the tracking side straightforward. Effective restricted fund management requires:

- Separate account designations in the COA for each restricted fund or grant

- Regular reporting on fund balances and spending against stated purposes

- A documented process for releasing restrictions when conditions are met

- Quarterly restricted fund activity reports reviewed by the board or finance committee

Warning Signs Boards Should Watch For

- A COA that lumps all revenue into a single donations account

- Staff inability to produce a fund-by-fund spending report on request

- Financial statements that don't distinguish between restricted and unrestricted net assets

- Frequent budget amendments to "reallocate" restricted funds

Financial Reports Every Board Should Request and Review

Understanding what each report is designed to tell you changes how useful it becomes in a board meeting. Boards need four core financial statements, each answering different governance questions.

The Four Core Financial Statements

Statement of Activities

Watch whether revenue is covering expenses and whether restricted funds are being drawn down at the right pace. This nonprofit equivalent of an income statement shows revenues and expenses over a period, broken out by restriction category — making operating performance and sustainability trends visible at a glance.

Statement of Financial Position

The key board question here: does the organization hold adequate liquid reserves, and is the ratio of restricted to unrestricted net assets sustainable? This nonprofit balance sheet captures assets, liabilities, and net assets at a point in time — your clearest view of financial stability and capacity to absorb disruption.

Statement of Cash Flows

Boards should watch for periods where cash is tight even when the statement of activities looks positive — this disconnect catches organizations off guard when payroll comes due but receivables haven't been collected. This report shows how cash actually moved through the organization, separate from accounting accruals.

Statement of Functional Expenses

Under ASU 2016-14, all nonprofits must present expenses by both natural classification and functional allocation in one location. This breaks down costs by nature (salaries, rent, supplies) and function (program, management and general, fundraising). It's critical for Form 990 compliance and for demonstrating efficient spending to donors.

Understanding Overhead Ratios

That functional expense breakdown feeds directly into how donors and watchdogs evaluate your organization. Know the benchmarks — but also their limits:

- Charity Navigator recommends 70%+ on program expenses

- BBB Wise Giving Alliance sets the floor at 65% for programs

- Both organizations co-signed the 2014 "Overhead Myth" campaign, rejecting overhead ratios as a standalone evaluation metric

Context matters. A newer organization building infrastructure or one actively investing in fundraising capacity may legitimately run higher overhead for a period.

Boards should request the statement of activities and statement of financial position at every meeting, supplemented by budget-to-actual comparison. Quarterly, add a restricted fund activity summary and cash flow statement.

Internal Controls and Red Flags Boards Should Know

Internal controls are structural safeguards built into how accounts are managed and approved. The board's governance role includes confirming these controls exist — and that they actually work.

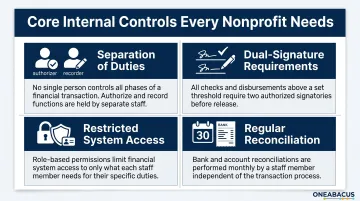

Critical Controls in Account Structure

- Separation of duties: The person who authorizes payments should not be the same person who records them or reconciles bank accounts

- Dual-signature requirements: Transactions above a defined threshold require two authorized signatures

- Restricted system access: Staff can only interact with accounts relevant to their roles, not the entire COA

- Regular reconciliation: Bank accounts are reconciled against accounting records monthly — any discrepancy investigated promptly

The COSO Internal Control Framework defines internal control as "a process effected by an organization's board of directors, management, and other personnel." Boards own this responsibility — they can't delegate it entirely to staff.

The Fraud Reality

When those controls are absent, the consequences are concrete. ACFE's 2020 Report to the Nations found a median loss of $75,000 across 191 nonprofit fraud cases, with lack of internal controls cited as the primary weakness in 35% of cases. Nonprofits lagged other organizations on anti-fraud measures: only 21% conducted surprise audits, 24% had formal fraud risk assessments, and 44% had internal audit departments.

Red Flags for Board Attention

These warning signs often surface before a formal problem does:

- Financial reports that arrive late or inconsistently

- Staff unable to produce fund-specific spending reports on request

- Unexplained variances between budgeted and actual figures

- A chart of accounts that hasn't been reviewed or updated in years

- Finance function dependent on one person with no backup

- Missing documentation for transactions, especially those involving executive staff

The board treasurer or finance committee should review these areas at least annually — and ask for written documentation of control processes, not just verbal assurances.

When Boards Should Bring in Expert Financial Leadership

Organizations typically outgrow their internal financial capacity long before they recognize it. Boards should proactively evaluate whether their current financial infrastructure supports the oversight they're responsible for — not wait for a compliance failure or audit finding to prompt action.

Signs Your Financial Capacity Is Falling Short

- Rapid growth in program complexity or funding streams

- Frequent errors in financial reporting or inability to close books on time

- Board members receiving reports they can't interpret or that don't answer basic governance questions

- Inability to track grant compliance in real time

- Finance function running on one person with no redundancy

- Staff spending more time compiling data manually than analyzing it

The Case for Fractional Financial Leadership

Rather than hiring a full-time CFO, nonprofits can engage experienced financial leadership on a part-time or project basis. This gives boards strategic oversight infrastructure — including proper COA design, fund accounting systems, and board-ready reporting — without the cost of a permanent executive hire.

Most organizations don't need a full-time CFO until they reach approximately $25 million in revenue — though nonprofits with complex funding structures often need fractional support well below that threshold. The right entry point depends on funding diversity, reporting demands, and board expectations.

One Abacus Advisory provides fractional CFO and financial leadership support scaled to each organization's complexity and stage. When Philadelphia Zoo faced the simultaneous departure of both their CFO and Controller, One Abacus stepped in with COA optimization in NetSuite, month-end close improvements, and board reporting upgrades — while providing hands-on guidance throughout the search and onboarding of new permanent leadership.

That kind of continuity during a critical transition is exactly what fractional support is designed to deliver.

Board Decision Criteria

Before deciding whether to bring in outside financial leadership, ask:

- Can our current team produce accurate, timely financial statements that meet GAAP and Form 990 requirements?

- Do we have the expertise to design and maintain fund accounting systems that track restriction compliance?

- Can we answer board governance questions from existing reports, or do we need custom analysis each time?

- Are our internal controls adequate to prevent and detect errors and fraud?

A single "no" signals a gap worth addressing before it surfaces in an audit finding or a funder conversation.

Frequently Asked Questions

What are best practices for financial oversight in a nonprofit organization?

Strong financial oversight rests on a few consistent practices:

- Establish a finance committee with clearly defined responsibilities

- Require regular review of all four core financial statements

- Maintain separation of duties across financial processes

- Conduct annual independent audits (or reviews for smaller organizations)

- Structure the chart of accounts to support transparent, mission-aligned reporting

What is the universal chart of accounts for nonprofits?

No single COA is mandated for all nonprofits. Most follow a five-category structure — assets, liabilities, net assets, revenue, and expenses — aligned with GAAP and Form 990 requirements. The Unified Chart of Accounts (UCOA) by the National Center for Charitable Statistics is a widely used reference, especially in human services.

What is the structure of a nonprofit finance department?

A typical structure includes a CFO or finance director overseeing accounting staff, with a board finance committee providing governance oversight. Smaller nonprofits often rely on a single bookkeeper or accountant. In those cases, fractional CFO support provides strategic oversight without the cost of a full-time executive hire.

What financial reports should a nonprofit board review at each meeting?

At every board meeting, review:

- Statement of activities

- Statement of financial position

- Budget-to-actual comparison

Quarterly, add a restricted fund activity summary and statement of cash flows to monitor liquidity and restriction compliance.

What is fund accounting and why do nonprofits use it?

Fund accounting tracks and reports on funds separately based on donor or grantor restrictions. GAAP requires it to demonstrate compliance with how money was received — ensuring restricted donations are spent only for their designated purposes.

How often should a nonprofit board conduct a financial audit?

The federal Single Audit threshold is $1 million in federal expenditures, effective for awards issued after October 1, 2024. Many states require audits for nonprofits above certain revenue thresholds. BBB Wise Giving Alliance recommends audited statements for organizations with over $1 million gross income, CPA reviews for $250,000-$1 million, and internally produced statements for smaller organizations.