This guide covers the three fiduciary duties that drive reporting requirements, the specific financial statements boards must see, Form 990 obligations, reporting cadence, and best practices for presenting financials clearly.

Key Takeaways

- Boards carry three legal duties (Care, Loyalty, Obedience) that obligate active review of financial and compliance reports

- Four key financial statements form the foundation: Statement of Financial Position, Statement of Activities, Statement of Cash Flows, and Statement of Functional Expenses

- IRS asks whether boards reviewed Form 990 before filing; missing three consecutive years triggers automatic loss of tax-exempt status

- Reports should flow monthly or quarterly, with a full annual review tied to audit completion and 990 filing

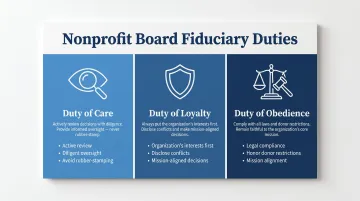

The Board's Three Legal Duties and How They Drive Reporting Requirements

Nonprofit board members are bound by three common-law fiduciary duties that define their legal and ethical responsibilities:

- Duty of Care — Board members must review financial reports with genuine diligence, not passive acceptance. Prudent oversight of all assets (facilities, staff, goodwill) is required. Rubber-stamping financials can expose individual board members to legal liability.

- Duty of Loyalty — The organization's interests come first. Members must recognize and disclose conflicts of interest, ensuring activities and transactions advance the mission rather than personal interests.

- Duty of Obedience — The nonprofit must operate consistently with its stated mission and applicable law. This means restricted funds follow donor intent, required tax returns are filed on time, and programmatic spending aligns with the mission.

Enforcement and Liability

These duties are enforced at both state and federal levels. State Attorneys General actively investigate breaches of fiduciary duties, with California, New York, and Ohio leading in oversight activity. The IRS oversees tax-exempt status at the federal level.

Board members can be held personally liable for the nonprofit's financial obligations in specific circumstances, particularly for failure to pay withholding taxes on employee wages.

Governance vs. Management Reporting

Boards should focus on strategic financial oversight, not day-to-day transactions. Governance reporting differs from management reporting — boards oversee financial health, approve budgets, and ensure compliance, while staff handles operational accounting.

Key Financial Statements Every Nonprofit Board Must Review

Four core GAAP-compliant financial statements should appear in every board financial packet, following FASB ASC 958 standards updated by ASU 2016-14.

Statement of Financial Position (Balance Sheet)

This report shows the organization's assets, liabilities, and net assets at a point in time. Board members should pay particular attention to:

- Liquid assets relative to short-term liabilities — Can the organization meet immediate obligations?

- Operating reserve size — Does the organization have sufficient cushion for unexpected challenges?

- Net asset classifications — Since 2017, nonprofits must report net assets in two categories:

- Net assets without donor restrictions (formerly unrestricted)

- Net assets with donor restrictions (formerly restricted)

Boards cannot redirect restricted funds for other uses, regardless of how much cash the organization holds.

Statement of Activities (Income Statement Equivalent)

This report shows revenues, expenses, and the change in net assets over a period. A critical nonprofit-specific accounting rule often confuses board members from for-profit backgrounds: large multi-year pledges must be recognized as revenue when committed, not when cash is received.

This creates apparent "deficits" that are not operational crises. The report narrative should always contextualize significant variances to prevent misinterpretation.

Statement of Cash Flows

The Statement of Cash Flows shows actual cash movement, not pledge-based accruals, making it the most direct indicator of near-term organizational health. Key warning signs boards should monitor include:

- Negative operating cash flow across two or more consecutive periods

- Growing gap between cash on hand and upcoming payroll or vendor obligations

- Declining unrestricted reserves without a documented drawdown plan

Statement of Functional Expenses

This statement breaks costs into program services, management/general, and fundraising. Under ASU 2016-14, all nonprofit organizations must now report expenses by both functional and natural classification — a requirement that previously applied only to health and welfare organizations.

This helps boards evaluate efficiency and shows donors exactly how resources support programs.

Form 990: Federal Filing Requirements and the Board's Role

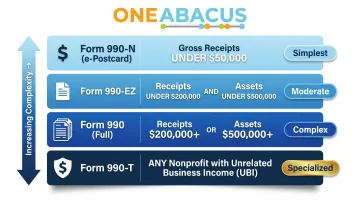

Filing Thresholds

Three versions of Form 990 exist, with filing requirements based on annual gross receipts and assets:

- Form 990-N (e-Postcard): Organizations with gross receipts under $50,000

- Form 990-EZ: Organizations with receipts under $200,000 AND assets under $500,000

- Form 990 (full): Organizations with receipts of $200,000 or more OR assets of $500,000 or more

- Form 990-T: Any nonprofit with unrelated business income, regardless of size

Filing Deadline and Extensions

Form 990 is due on the 15th day of the 5th month after the close of the fiscal year. For calendar-year organizations, this is May 15. Form 8868 provides an automatic 6-month extension.

Automatic Revocation Risk

Missing three consecutive years triggers automatic revocation of tax-exempt status. Between 2010 and 2017, the IRS revoked tax-exempt recognition for more than 760,000 nonprofit organizations due to non-filing. After revocation, the organization loses its ability to receive tax-deductible contributions and may owe corporate income tax.

Board Review Question

Form 990 Part VI, Question 11a asks whether the final Form 990 was provided to all governing board members before filing. While IRS regulations do not legally require board review, the IRS includes this question because board review correlates with accuracy and reflects engaged governance. The answer is disclosed publicly, making it a direct transparency signal to donors, foundations, and watchdog groups who routinely check it.

Public Accessibility

Form 990 is publicly available through ProPublica, Candid, and other platforms. Donors, foundations, and watchdog groups will review it. That visibility means the narrative portions of the 990 — program descriptions, executive compensation disclosures, and governance policies — carry real weight. Boards that engage with those sections before filing are better positioned to ensure the document accurately reflects the organization's mission and stewardship.

Key areas where board input strengthens the 990:

- Program Service Accomplishments (Part III): Ensures descriptions reflect actual impact, not just activity

- Compensation disclosures: Board awareness prevents surprises in public filings

- Governance policies (Part VI): Confirms the organization's stated practices match reality

How to Present Financial Reports to Your Board Effectively

Even accurate financials fail boards if they're hard to read. A Stanford study of 924 nonprofit directors found that 42% of boards lack an audit committee, and many rely solely on monthly bank statements for financial monitoring — leaving critical decisions underinformed.

Plain Language and Visual Clarity

Financial reports should:

- Use plain language and define nonprofit-specific terms (e.g., "net assets with donor restrictions")

- Include charts or visuals illustrating revenue vs. expenses, budget-to-actual variances, and liquidity trends

- Avoid technical jargon that alienates non-financial board members

- Provide context for variances that might alarm board members unfamiliar with nonprofit accounting rules

Connect Data to Mission Impact

Every board packet should include a program-level financial summary showing:

- What it cost to deliver key services

- Whether restricted funds were used in compliance with donor intent

- Where the organization stands against its annual budget

- How financial performance aligns with strategic goals

Fractional CFO Support

Organizations without a full-time CFO often struggle to produce board-ready financial packages consistently. One Abacus Advisory steps in to prepare clear, mission-aligned financial reports and serve as the financial expert in the boardroom. During the Philadelphia Zoo's leadership transition, for instance, One Abacus optimized their NetSuite environment and enhanced board reporting. The result: greater board confidence in financial results and a smoother transition overall.

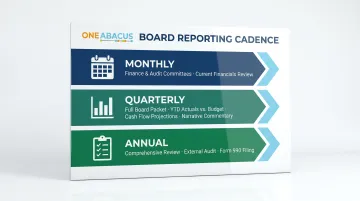

Nonprofit Board Reporting Cadence: How Often Should Reports Be Delivered?

Standard reporting rhythm includes:

- Monthly financial reports for active committees (finance committee, audit committee)

- Full quarterly financial packets for the full board, including YTD actuals vs. budget, cash flow projections, and narrative commentary

- Comprehensive annual report tied to completion of the external audit and filing of Form 990

Aligning with Board Meeting Frequency

The average nonprofit board meets 6.9 times per year, with most boards meeting quarterly. Smaller nonprofits typically consolidate monthly data into quarterly packets. Larger organizations with complex finances benefit from monthly finance committee review before the full board presentation.

Proactive vs. Reactive Reporting

Cadence matters, but so does the nature of what gets reported. Proactive reporting — sharing financial projections and flagging potential shortfalls before they become crises — is a hallmark of strong financial governance. Strong boards require forward-looking analysis, not just historical data.

Common Nonprofit Board Reporting Mistakes to Avoid

The most consequential reporting mistakes include:

- Presenting numbers without narrative context leaves boards guessing what the figures actually mean

- Showing actuals without budget comparisons makes it impossible to assess whether performance is on track

- Conflating cash position with pledge-based revenue — an organization can show positive net assets while facing an immediate cash shortfall

- Submitting Form 990 before board review, cutting out the governance step that should happen before filing

Over-Reporting vs. Under-Reporting

Boards fall short in two directions: overwhelmed by excessive detail, or left without the information they actually need. According to Brady Martz's nonprofit governance research, both failure modes undermine fiduciary oversight. The goal is a concise, decision-ready financial packet — not a data dump. Every report should answer one question: what does the board need to know to fulfill its fiduciary duties?

Frequently Asked Questions

What are the three legal responsibilities of a nonprofit board?

The three fiduciary duties are Duty of Care (active, informed oversight), Duty of Loyalty (placing organizational interests above personal interests), and Duty of Obedience (ensuring legal compliance and mission alignment). Each duty requires regular review of financial and operational reports.

What financial statements should a nonprofit board review at each meeting?

Boards should review four core statements: Statement of Financial Position, Statement of Activities, Statement of Cash Flows, and Statement of Functional Expenses. A budget-to-actual comparison should accompany every meeting packet to give members clear context for each statement.

How often should a nonprofit board receive financial reports?

Standard cadence is monthly for finance/audit committees, quarterly for the full board, and annually with the audit and Form 990. Frequency should align with board meeting schedules and organizational complexity.

Does the board have to review Form 990 before it's filed?

The IRS doesn't require board review of the 990 by law, but it asks about it on the form as a governance disclosure. Best practice strongly recommends full board review before filing to ensure accuracy and transparency.

What happens if a nonprofit fails to file Form 990?

Late filing triggers penalties. Missing three consecutive years results in automatic revocation of tax-exempt status. At that point, the organization loses eligibility for tax-deductible donations and may face corporate income tax.

What is the difference between restricted and unrestricted funds, and why does it matter for board reporting?

Restricted funds must be used only for donor-specified purposes, while unrestricted funds give the board flexibility. Board members must confirm in every reporting cycle that restricted funds are being spent in compliance with donor intent.