Introduction

Nonprofit leaders face an escalating tension: accountability is increasingly demanded by funders, regulators, and the public — yet many organizations treat it as a compliance checkbox rather than a strategic tool. This disconnect carries real consequences. According to Independent Sector's 2025 Trust in Nonprofits report, 57% of Americans report high trust in nonprofits — higher than any other sector measured, including the military, government, and business. But this trust advantage is fragile, especially when only 29% trust wealthy philanthropy, and expectations for transparency continue to rise.

That fragile trust is exactly why the strongest nonprofits treat accountability as a strategic asset — not just a filing deadline. True accountability spans financial stewardship, governance oversight, program impact, ethical conduct, and stakeholder relationships.

This guide covers each of these dimensions in depth:

- The frameworks and mechanisms that make accountability work

- The financial rules nonprofit leaders must know

- How to embed accountability into organizational culture

- Turning compliance into a driver of mission success

Key Takeaways

- Accountability spans financial stewardship, governance, mission performance, and stakeholder trust — not just IRS compliance

- Key mechanisms: Form 990 disclosure, board fiduciary duties, internal controls, ethics policies, and impact reporting

- The 33% public support test and fund accounting rules directly affect tax-exempt status and require active monitoring

- Strategic accountability builds donor confidence and long-term credibility — it's a driver of organizational learning, not just a compliance checkbox

What Nonprofit Accountability Really Means

Accountability in the nonprofit sector is a dual question: accountability to whom and accountability for what. The "to whom" includes funders, beneficiaries, the public, regulators, and staff. The "for what" encompasses finances, governance, program outcomes, and ethical conduct. These are not the same obligation, and most organizations over-index on funder accountability at the expense of community and beneficiary accountability.

Upward vs. Downward Accountability

Edwards and Hulme (1996) define upward accountability as obligations to donors or governments, driven by control over financial or regulatory resources. Downward accountability refers to obligations to beneficiaries and communities the organization directly serves. Research consistently shows nonprofits prioritize the former — compliance-driven, funder-facing requirements — while underinvesting in the latter.

That imbalance erodes mission focus. When funder reporting crowds out beneficiary feedback, an organization becomes accountable to those who fund the work rather than those it exists to serve. The Global Standard for CSO Accountability offers a multi-stakeholder framework for closing that gap.

Reframing Accountability as Strategic

When used proactively — to gather data, communicate impact, and inform decisions — accountability becomes a tool for organizational growth, not just compliance. Done well, it creates feedback loops that:

- Strengthen program design with real beneficiary input

- Build funder confidence through transparent reporting

- Deepen community trust over time

Organizations that treat accountability as a paperwork burden never access these benefits. The ones that treat it as a strategic function tend to be more resilient, better funded, and more mission-aligned.

The Core Dimensions of Nonprofit Accountability

Financial Accountability

This dimension covers accurate financial reporting, responsible stewardship of donor and grant funds, adherence to restricted fund requirements, and transparent disclosure through Form 990 and annual audits. Financial accountability ensures resources are used as intended and that stakeholders can verify fiscal responsibility.

This is where fractional CFO support pays off practically. One Abacus Advisory provides board-ready financial reports (budgets, cash flow forecasts, and variance analysis) that make financial oversight accessible even for non-finance board members.

Governance Accountability

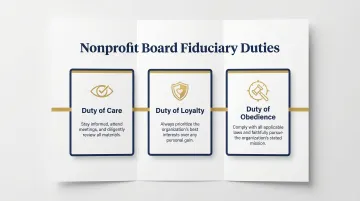

Nonprofit boards hold three fiduciary duties, as defined by BoardSource:

- Duty of Care: Exercise reasonable care, stay informed, attend meetings, review materials

- Duty of Loyalty: Put the organization's interests ahead of personal or professional interests

- Duty of Obedience: Ensure compliance with laws and operate in furtherance of the stated mission

Governance accountability means the board actively oversees executive performance, approves budgets, reviews financial statements, and enforces ethical standards. Without board ownership, accountability is structurally hollow.

Mission and Program Accountability

Nonprofits must demonstrate not just that they spent money correctly, but that programs are producing measurable outcomes aligned with the stated mission. This requires:

- Performance metrics tied to mission objectives

- Program evaluation methods (surveys, outcome tracking, beneficiary feedback)

- Regular impact reporting to stakeholders

Funders increasingly expect evidence of outcomes, not just outputs. Meeting that standard strengthens grant renewals and donor trust simultaneously.

Stakeholder and Relational Accountability

Nonprofits must answer to multiple stakeholder groups simultaneously: donors, grant-makers, service recipients, community members, and staff. Charity watchdog organizations publish ratings that directly affect fundraising capacity, including:

- Candid (GuideStar) — transparency and financial data reporting

- Charity Navigator — financial health, accountability, and transparency scores

- BBB Wise Giving Alliance — governance, finance, and donor protection standards

Ethical Accountability

Ethical accountability encompasses:

- Conflict of interest policies

- Whistleblower protections

- Executive compensation practices

- Document retention policies

Form 990 Part VI directly asks about several of these. Since the Sarbanes-Oxley Act of 2002, best-practice expectations have risen sharply. Only two SOX provisions apply directly to nonprofits (document destruction prohibition and whistleblower retaliation prohibition), but the Act prompted voluntary adoption of governance best practices across the sector.

Key Mechanisms and Frameworks That Ensure Accountability

IRS Form 990 as an Accountability Instrument

Form 990 is publicly available and serves as the primary transparency document for nonprofits. It discloses:

- Revenue, expenses, and changes in net assets

- Program service accomplishments

- Officer, director, trustee, and key employee compensation

- Governance practices (Part VI)

- Related organizations and unrelated business income

Watchdog organizations use Form 990 to rate nonprofits on fiscal responsibility and impact. A governance best practice specifically noted in the form itself is that board members should review the 990 before it is filed.

Board Governance Structures

Form 990 disclosures are only as strong as the governance behind them. A board must have specific oversight mechanisms in place:

- Audit or finance committee

- Annual budget approval

- Regular financial statement review

- Executive performance evaluations

- Written conflict of interest policy that is enforced

Internal Controls and Audit Processes

Internal controls — segregation of duties, authorization protocols, reconciliation procedures — prevent errors and fraud by ensuring no single person controls all aspects of a financial transaction. They form the day-to-day operating layer that keeps financial accountability functional between audits.

Annual independent audits verify the accuracy of financial statements and compliance with accounting standards. One key federal requirement to know: the Single Audit threshold was raised to $1,000,000 effective for fiscal years beginning on or after October 1, 2024 (up from $750,000). Nonprofits expending $1 million or more in federal awards must undergo a Single Audit. State audit requirements vary and should be reviewed separately.

One Abacus Advisory helps nonprofits prepare for audits by organizing financial records, strengthening internal controls, and addressing compliance gaps before auditors arrive — reducing risk and building stakeholder confidence.

Codes of Ethics and Written Policies

Written ethics codes, whistleblower policies, document retention policies, and conflict of interest policies create a formal foundation for accountability. IRS Form 990 and most state nonprofit associations now treat them as baseline expectations, even where they aren't legally required.

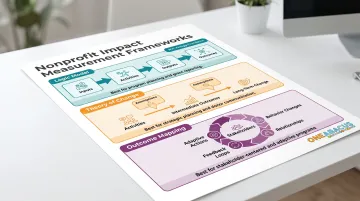

Impact Measurement and Reporting Frameworks

Nonprofits can adopt frameworks to translate program activity into measurable impact:

- Logic Models: Visual maps linking program inputs to activities, outputs, and outcomes — giving funders a clear picture of how resources produce results (W.K. Kellogg Foundation)

- Theory of Change: A cause-and-effect sequence that traces a nonprofit's activities through to intended long-term outcomes, making strategic assumptions explicit

- Outcome Mapping: Tracks changes in behavior, relationships, or actions among key stakeholders rather than just program outputs

These frameworks help nonprofits demonstrate impact to funders, boards, and the public, strengthening both accountability and fundraising capacity.

Financial Accountability: Rules, Ratios, and Real Oversight

The IRS Public Support Test (33% Rule)

To maintain 501(c)(3) public charity status, an organization generally must receive at least one-third of its total support from public sources under IRS Section 509(a)(1) or 509(a)(2).

What counts as public support:

- Individual donations

- Government grants

- Contributions from other public charities

Measurement period: Five-year rolling period, reported on Schedule A of Form 990.

Consequences of failure: Reclassification as a private foundation, which triggers:

- Excise taxes on net investment income

- Mandatory distribution requirements

- Self-dealing restrictions

Finance staff must monitor this ratio annually to avoid reclassification.

The 80/20 Rule in Nonprofit Financial Management

The Pareto Principle, widely cited in fundraising, suggests that approximately 80% of donations come from 20% of donors. Some practitioners observe even greater concentration (90/10), though digital fundraising and recurring gift programs may moderate this toward 70/30 or 60/40.

Over-reliance on a small donor base creates accountability risk and financial fragility. Diversifying revenue — across individual donors, foundations, government grants, and earned income — is both a financial health strategy and an accountability best practice for any mission-driven organization.

Program vs. Administrative Expense Ratios

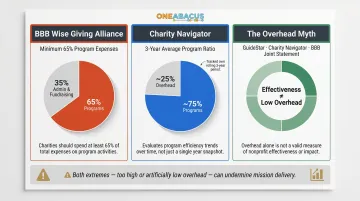

Watchdog organizations evaluate nonprofits using expense ratios:

- BBB Wise Giving Alliance: Requires at least 65% of total expenses on program activities

- Charity Navigator: Calculates program expense ratio as the average over the three most recent fiscal years

However, the overhead myth persists. In 2013, GuideStar, Charity Navigator, and BBB co-signed a letter urging donors to stop using overhead as a primary effectiveness measure. Both extremes — too high overhead or artificially low overhead that underfunds operations — can undermine financial health and mission delivery. Boards should invest in adequate infrastructure.

Financial Reporting and Board Transparency

Expense ratios are only useful when boards actually understand what the numbers mean. That requires regular, readable financial reporting — not just raw data. The board (or its finance committee) should receive and review:

- Balance sheet

- Income statement (statement of activities)

- Cash flow statement

These should be compared against the approved budget. Clear, readable financial reports empower board members to ask the right questions and fulfill their fiduciary duties.

For nonprofits without a full-time finance leader, this is a real gap. One Abacus Advisory's fractional CFO work — including engagements with organizations like the San Diego Food Bank and Laguna Playhouse — centers on giving boards exactly this kind of analysis: budget-to-actual comparisons, cash flow projections, and financial narratives that make governance practical rather than ceremonial.

Restricted Fund Stewardship

Grant funds and restricted donations must be tracked and spent according to donor or grantor intent. Misuse of donor-restricted funds can be treated as breach of contract or fraud, with potential consequences including:

- Grant claw-backs

- Reputational damage

- IRS scrutiny

- Board liability

FASB ASU 2016-14 requires nonprofits to maintain contemporaneous documentation of donor intent and report net assets in two classes: with donor restrictions and without donor restrictions. A proper fund accounting system — rather than a general-ledger-only approach — simplifies compliance and supports clean audits.

Platforms like NetSuite, Sage Intacct, and QuickBooks Online each handle fund accounting differently — choosing the right one (and configuring it correctly) determines whether restricted fund tracking is a routine process or a recurring fire drill.

Turning Accountability Into Organizational Culture

Build Accountability Into Roles and Workflows, Not Just Policies

Accountability becomes organizational when it is embedded into job descriptions, performance reviews, onboarding training, and daily workflows — not just documented in a policy handbook. Assign clear ownership for each functional area: strategy, operations, programs, marketing, and fundraising.

Role-specific accountability looks different across the organization:

- Program directors: accountable for tracking and reporting outcome data, not just delivering services

- Finance staff: accountable for timely, accurate reporting and compliance

- Executive directors: accountable for overall mission alignment and organizational health

Communicate Accountability Both Inward and Outward

Share accountability data internally through:

- Staff dashboards

- All-hands updates

- Board reports

Internal transparency builds trust across the team. External communication extends that credibility to the wider community — share results through:

- Annual reports

- Website impact pages

- Social media

- Community briefings

Silence erodes trust. Even when results are imperfect, transparent communication builds credibility. Donors, board members, and community members respond positively to honesty and evidence of learning.

Treat Accountability as a Learning System, Not Just a Reporting Obligation

High-performing nonprofits use accountability mechanisms to generate organizational learning. They review what worked, what didn't, and why — then adjust programs and strategies accordingly. Done well, accountability stops being a compliance exercise and starts driving better program decisions.

The W.K. Kellogg Foundation emphasizes that evaluation should balance "proving" (accountability) with "improving" (quality). That means investing in meaningful outcome measurement — even when it's harder — rather than defaulting to metrics that are easy to track but fail to reflect real program impact.

Frequently Asked Questions

What are the 33% rule and the 80/20 rule for nonprofit organizations?

The 33% rule is the IRS public support test requiring at least one-third of a public charity's support to come from public sources over a five-year period. The 80/20 rule is a fundraising observation that roughly 80% of donations come from 20% of donors — which makes revenue diversification critical to reducing financial risk.

What mechanisms and frameworks ensure accountability in nonprofit organizations?

Core mechanisms include:

- IRS Form 990 public disclosure

- Board governance structures (audit committees, financial oversight)

- Internal controls and independent audits

- Codes of ethics and written policies

- Program evaluation frameworks like logic models and theory of change

What is nonprofit accountability and why does it matter?

Nonprofit accountability is the obligation to be answerable to multiple stakeholders — funders, beneficiaries, the public, and regulators — for both financial stewardship and mission performance. Strong accountability directly influences donor trust, fundraising capacity, and long-term organizational credibility.

Who is ultimately responsible for accountability in a nonprofit?

The board of directors holds ultimate fiduciary and governance accountability, including the duties of care, loyalty, and obedience. The executive director and senior staff are responsible for day-to-day operational and programmatic accountability.

How does IRS Form 990 support nonprofit accountability?

Form 990 is a publicly available tax document that discloses a nonprofit's finances, programs, governance practices, and executive compensation. Charity watchdog organizations use it to rate nonprofits on fiscal responsibility and charitable impact, influencing public trust and fundraising success.

What is the difference between upward and downward accountability in nonprofits?

Upward accountability refers to obligations to funders, regulators, and oversight bodies — compliance-driven and resource-focused. Downward accountability refers to obligations to the communities and beneficiaries served — mission-driven and relational. High-performing nonprofits build structured feedback loops with beneficiaries, not just reporting pipelines to funders.