Introduction

Most nonprofits don't have a dedicated HR team — yet they face the same employment law obligations as any for-profit business, plus a layer of IRS regulations tied to tax-exempt status. The nonprofit sector accounts for 12.8 million jobs and 9.9% of the total US private workforce, yet many organizations rely on finance or operations staff to manage HR compliance alongside their primary duties.

Noncompliance carries real consequences: financial penalties, back taxes, IRS scrutiny, and in severe cases, loss of 501(c)(3) status — all of which directly threaten your organization's mission. This guide gives nonprofit leaders, executive directors, and board members a practical, 2026-ready HR compliance checklist with actionable steps to audit and close compliance gaps.

TLDR:

- Nonprofits face the same employment laws as for-profits, plus IRS tax-exempt regulations

- Misclassifying workers can result in back taxes, penalties, and personal board liability

- Annual HR compliance audits catch gaps before they become enforcement actions

- Document payroll, compensation, and policies to protect 501(c)(3) status

- Fractional financial leadership ensures compliance oversight during growth or transitions

How Nonprofit HR Compliance Differs from For-Profit

Three factors make nonprofit HR compliance uniquely complex:

- Limited budgets mean HR duties often fall to finance or operations staff rather than dedicated HR professionals

- Volunteer-employee overlap creates classification gray areas that require careful documentation and ongoing review

- Tax-exempt status adds an IRS compliance layer that for-profits never face, including public disclosure of executive compensation and private inurement restrictions

The Key Myth: Nonprofit Status Doesn't Exempt You from Employment Laws

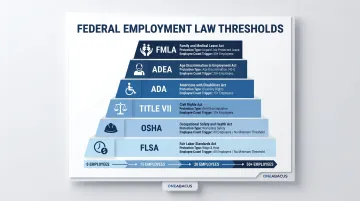

501(c)(3) status does not exempt your organization from federal or state employment laws. Once you hit the relevant employee thresholds, these federal laws apply just as they would to any business:

- FLSA — Minimum wage and overtime requirements (most employers)

- Title VII — Anti-discrimination protections (15+ employees)

- ADA — Disability accommodations (15+ employees)

- ADEA — Age discrimination protections (20+ employees)

- FMLA — Unpaid leave rights (50+ employees)

- OSHA — Workplace safety standards (most employers)

State laws often go further — California, New York, and Illinois, for example, extend anti-discrimination and leave protections to employers well below federal thresholds. Check your state's requirements even if you have fewer than 15 employees.

Your 2026 Nonprofit HR Compliance Checklist at a Glance

Worker classification: Correctly categorize all workers as employees, independent contractors, or volunteers before any other compliance work begins.

Payroll and tax withholding: Ensure federal income tax, Social Security, and Medicare are withheld for all employees regardless of tax-exempt status.

HR policies and employee handbook: Keep a legally reviewed handbook current — covering anti-discrimination, leave policies, and remote work.

Recordkeeping: Retain I-9s, personnel files, payroll records, and signed agreements per federal and state schedules.

Workplace safety: Confirm OSHA compliance applies to your nonprofit and that your work environment meets minimum safety standards.

Annual compliance audit: Audit all compliance areas at least once per year to catch gaps before they become penalties.

Worker Classification and Labor Law Requirements

Why Classification Matters

Misclassifying an employee as an independent contractor or a volunteer can result in back taxes, unpaid benefits liability, and significant IRS and state Department of Labor penalties. Correct classification is the foundation of everything else in HR compliance. The IRS has stepped up enforcement in recent years, making classification audits increasingly common.

Three Worker Categories Nonprofits Must Distinguish

Employees:

- Entitled to wage/hour protections under FLSA

- Benefits eligibility and tax withholding required

- Covered by workers' compensation and unemployment insurance

- Subject to anti-discrimination protections

Independent contractors:

- Responsible for their own taxes and benefits

- Receive Form 1099 instead of W-2

- Must meet DOL's six-factor economic reality test for legitimate contractor status

- Maintain control over how work is performed

Volunteers:

- Must not perform work that would normally require a paid employee

- Cannot receive compensation beyond expense reimbursement

- Should have clear volunteer agreements and waivers

- May receive nominal stipends without triggering employee status

FLSA Requirements for Nonprofit Employees

Federal minimum wage: $7.25 per hour (state minimums often exceed this and must be checked by state).

Overtime requirements:

- Non-exempt employees must receive overtime pay at 1.5× their regular rate for hours worked over 40 per week

- Exempt classifications (executive, administrative, professional) require minimum salary of $684 per week ($35,568 annually) and duties tests

- Misclassifying employees as exempt exposes organizations to back wage liability

Wage and hour rules are only part of the picture. Federal anti-discrimination law adds another layer of compliance obligations tied directly to your headcount.

Anti-Discrimination Obligations

Federal protections under Title VII, ADA, and ADEA apply when nonprofits meet these thresholds:

- Title VII and ADA: 15 or more employees for at least 20 calendar weeks

- ADEA: 20 or more employees for at least 20 calendar weeks

- Equal Pay Act: Virtually all employers regardless of size

Smaller nonprofits may still be covered under state equivalents with lower thresholds.

Staying ahead of these thresholds — and documenting your worker relationships accordingly — is where an annual audit pays off.

Run an Annual Classification Audit

Have HR or operations staff review every worker relationship against IRS and DOL classification guidelines each year — especially when:

- Adding new roles or expanding services

- Transitioning volunteers to paid positions

- Bringing on consultants or temporary staff

- Receiving increased grant funding that changes operations

Payroll, Tax Withholding, and Executive Compensation

Tax Withholding: Not Optional for Nonprofits

501(c)(3) status does not exempt organizations from withholding federal income tax, Social Security, and Medicare from employee wages. Board members may be personally liable for failure to remit these withholdings under the IRS Trust Fund Recovery Penalty (TFRP), which equals 100% of the unpaid trust fund tax plus interest.

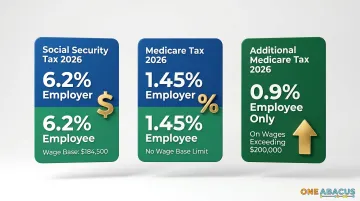

2026 tax rates:

- Social Security: 6.2% each for employer and employee (wage base limit: $184,500)

- Medicare: 1.45% each for employer and employee (no wage base limit)

- Additional Medicare: 0.9% on employee wages exceeding $200,000 (employee share only)

State-Specific Payroll Obligations

States have expanded paid leave mandates and wage requirements. Examples for 2026:

| State | Program | 2026 Requirement |

|---|---|---|

| New York | Paid Family Leave | Max weekly benefit: $1,228.53; employee contribution: 0.432% of gross wages |

| Colorado | FAMLI | Total premium: 0.88% of wages (0.44% employer / 0.44% employee) |

| Minnesota | PFML | Premiums: 0.88% on wages up to $185,000; benefits began January 1, 2026 |

Check your state's minimum wage, overtime rules, and unemployment tax methods. Many nonprofits qualify for unemployment insurance reimbursement instead of standard SUTA contributions, potentially reducing costs.

Executive Compensation Compliance

Executive director pay appears publicly on Form 990, making it highly visible to donors, funders, and the IRS. Compensation must be "reasonable and not excessive," and the board must document the decision-making process.

IRS rebuttable presumption of reasonableness requires:

- Approval by an authorized body composed entirely of individuals with no conflict of interest

- Appropriate comparability data (peer organizations, regional salary surveys, industry benchmarks)

- Adequate documentation of the basis for the determination

Private Inurement and Excess Benefit Transactions

Nonprofits cannot allow net earnings to benefit insiders — board members, officers, or key employees. All insider transactions must be at arm's length with proper documentation. Excess benefit transactions trigger IRS excise taxes and can jeopardize 501(c)(3) status. Common triggers include:

- Undocumented board member perks or expense reimbursements

- Loans to insiders without formal terms or repayment schedules

- Compensation packages that lack salary benchmark documentation

Fractional CFO Support for Compliance Oversight

For nonprofits without a full-time CFO or HR director, fractional financial leadership fills a real gap — covering payroll oversight, executive compensation benchmarking, and Form 990 disclosure review with the rigor those processes require.

Organizations navigating growth, leadership transitions, or increased regulatory scrutiny often find this model most useful. One Abacus Advisory's fractional CFO services handle these responsibilities at the executive level, without the overhead of a full-time hire.

HR Policies, Documentation, and Record-Keeping

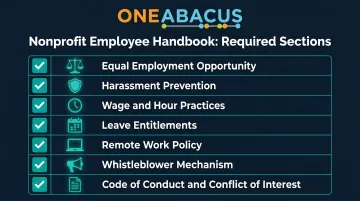

What Your Employee Handbook Must Include in 2026

Every nonprofit employee handbook should cover these core areas at minimum:

- Equal employment opportunity and non-discrimination

- Harassment and discrimination prevention with reporting procedures

- Wage and hour practices (overtime, breaks, timekeeping)

- Leave entitlements (FMLA, state paid sick leave, vacation)

- Remote work expectations and equipment use

- Whistleblower/reporting mechanism for workplace concerns

- Code of conduct and conflict of interest policies

Once your handbook policies are in place, maintaining the records that back them up becomes equally important.

Federal Recordkeeping Obligations

Required records and retention periods:

| Record Type | Minimum Retention | Authority |

|---|---|---|

| Form I-9 | 3 years from hire OR 1 year after termination (whichever is later) | USCIS M-274 |

| Payroll records | 3 years | DOL FLSA |

| Employment tax records | 4 years | IRS Publication 15 |

| OSHA 300 Log and incident reports | 5 years | OSHA Reg. 1904.33 |

| Personnel files | Duration of employment + 1-3 years | State-dependent |

Secure Storage Practices

Retention schedules only matter if records are actually protected. For nonprofits running with small HR teams, cloud-based systems with role-based permissions offer a practical way to control access without heavy IT overhead. At minimum:

- Only authorized staff can access personnel files

- Digital records are backed up regularly

- Physical files are stored in locked cabinets

- Terminated employee records are archived separately

Conducting Annual HR Compliance Audits

What a Nonprofit HR Compliance Audit Covers

An annual review of:

- Worker classifications (employees vs. contractors vs. volunteers)

- Pay practices (minimum wage, overtime, salary thresholds)

- I-9 forms (completion, retention, E-Verify if applicable)

- Policy documentation (handbook currency, acknowledgment signatures)

- Training records (harassment prevention, safety, compliance topics)

- Safety standards (OSHA compliance, incident logs, workplace assessments)

Proactive audits catch gaps before they become enforcement actions. State agencies have increased scrutiny of nonprofit worker classification, making regular reviews essential.

Five Steps for a Practical Compliance Audit

1. Assemble a small team from HR, finance, and leadership with compliance knowledge and access to records.

2. Build or update a checklist against current federal and state requirements (DOL fact sheets, IRS guidance, state labor department updates).

3. Gather all relevant HR documents:

- Employee files and I-9 forms

- Payroll records and tax filings

- Signed handbook acknowledgments

- Training completion records

- OSHA logs (if applicable)

4. Identify gaps or inconsistencies:

- Missing or expired I-9 forms

- Misclassified workers

- Outdated policy language

- Incomplete training documentation

- Recordkeeping deficiencies

5. Create a written action plan with owners and deadlines for remediation, and report findings to leadership and the board.

External Support for Resource-Constrained Nonprofits

Many nonprofits complete a five-step audit only to realize they don't have the internal bandwidth to run it consistently year after year. That's where external support fills a real gap.

A fractional COO or HR consultant can conduct or oversee the audit, identify issues an internal team might overlook, and build a remediation plan leadership can actually execute. The cost is far less than a DOL penalty or the reputational fallout from a compliance failure — and it frees internal staff to focus on programs rather than paperwork.

Frequently Asked Questions

What are common HR compliance issues?

The most frequent nonprofit HR compliance pitfalls include worker misclassification, failure to follow wage and hour laws, missing or outdated HR policies, improper recordkeeping, and overlooking state-specific leave or wage requirements. These issues often stem from limited HR expertise and competing priorities.

What should an HR report include?

A nonprofit HR compliance report should cover:

- Workforce composition and worker classifications

- Payroll accuracy and wage compliance

- Policy acknowledgment status and training completion

- Open compliance gaps and any active incidents or investigations

This gives boards and leadership a clear picture of risk exposure and where resources are needed.

Can nonprofits lose their tax-exempt status over HR violations?

While minor HR infractions typically result in fines rather than status revocation, repeated violations — particularly those involving private inurement, excess benefit transactions, or failure to pay employment taxes — can draw IRS scrutiny that puts 501(c)(3) status at risk. Board members may face personal liability for trust fund tax failures.

Do volunteers at nonprofits need to follow the same HR rules as employees?

Volunteers are not covered by wage and hour laws, but nonprofits still need clear policies, signed waivers, safety training, and documentation to manage liability and avoid misclassification claims. Any stipends or benefits beyond direct expense reimbursement may trigger employee status under the IRS economic reality test.

How often should nonprofits conduct an HR compliance audit?

At minimum, conduct an annual audit. More frequent reviews (semi-annual) are recommended during periods of organizational growth, staff changes, or after significant updates to state or federal employment laws. Document findings and remediation actions each time.

What are the penalties for misclassifying workers at a nonprofit?

Misclassification penalties include:

- Back taxes and unpaid overtime or benefits

- IRS Trust Fund penalties (100% of unpaid withholding)

- State fines and potential litigation

Board members may bear personal liability for tax withholding failures — making correct classification a financial priority for the organization and its leadership.

Need help navigating nonprofit HR compliance? One Abacus Advisory provides fractional CFO and COO services tailored to nonprofits, delivering hands-on financial and operational oversight to keep your organization compliant through growth, leadership transitions, and regulatory change. Schedule a free consultation to discuss your organization's needs.