Introduction

Government funding cuts, shifting donor priorities, and persistent economic uncertainty are pushing many nonprofits to the edge. The numbers are stark: 52% of nonprofits currently have three months or less of cash on hand, with 18% operating with just one month of reserves. Among organizations surveyed in both 2022 and 2025, the share with six or more months of cash reserves dropped from 36% to 26%.

Financial sustainability means more than surviving the current fiscal year. It's about building systems that protect your mission through funding disruptions, leadership transitions, and economic downturns — through diversified revenue, adequate reserves, and strong financial oversight.

This guide covers the core pillars of financial sustainability, the barriers that most commonly derail nonprofits, a practical planning framework, and the metrics that signal genuine organizational health.

TLDR:

- 52% of nonprofits have 3 months or less of cash reserves, creating acute vulnerability

- Financial sustainability requires diversified revenue, adequate reserves, and multi-year planning

- Building reserves, strengthening board oversight, and investing in financial infrastructure reduce long-term risk

- Track months of liquid reserves, revenue concentration, and operating margins to measure health

- Fractional financial leadership can fill expertise gaps cost-effectively

What is Financial Sustainability for Nonprofit Organizations?

Financial sustainability is the ongoing, strategic capacity to generate diversified revenue, manage expenses wisely, and build resilience so your organization keeps fulfilling its mission through disruptions, downturns, and leadership change. The National Council of Nonprofits defines it as "a plan that allows a nonprofit to sustain itself over the long term so that it is able to continue to support its mission."

Unlike a single-year balanced budget, financial sustainability includes:

- Multiple diversified funding streams that reduce dependence on any single source

- Adequate cash reserves to weather revenue gaps or unexpected crises

- Transparent financial reporting systems that build stakeholder trust

- Multi-year financial planning that anticipates future needs and challenges

- Leadership continuity structures that preserve institutional knowledge

For nonprofits working with fractional financial leadership providers like One Abacus Advisory, this means translating those pillars into practical systems — stronger budgeting, multi-year forecasting, audit-ready compliance, and board reporting that drives real decisions.

Sustainability vs. Stability: Why the Distinction Matters

Financial stability means being solvent and operational right now — covering this month's payroll, paying vendors on time, and keeping programs running. Sustainability goes further: it's about building the systems that keep an organization financially healthy through leadership transitions, economic downturns, and funding shifts.

Consider this contrast:

- Stability: Having enough revenue to cover this year's budget

- Sustainability: Having a funded reserve, diversified income streams, a multi-year financial plan, and documented processes that survive staff turnover

The data reveals how quickly stability can erode without sustainability structures. Among nonprofits surveyed in 2022 and again in 2025, deficit rates nearly tripled from 13% to 37%. Organizations that appeared financially stable at one point saw their positions deteriorate dramatically within just three years.

A 2025 Urban Institute study found that nonprofits dependent on government for 42% of revenue (versus the 28% average) bore the heaviest losses from funding disruptions: 29% cut staff compared to 15% across all nonprofits, and 23% reduced programming versus 12%.

Relying on stability alone leaves organizations one lost grant or major donor away from crisis. Building sustainability means that when funding shifts — and it will — the organization has the reserves, diversification, and planning infrastructure to absorb the impact and keep moving forward.

The Core Pillars of Nonprofit Financial Sustainability

Five interconnected pillars form the building blocks of a sustainable financial strategy. Weakness in any one area creates vulnerability across the entire organization, which is why comprehensive approaches deliver the strongest results.

Diversified Revenue Streams

Over-dependence on any single funding source — whether a major donor, government grant, or signature fundraising event — represents one of the most common and dangerous threats to financial sustainability. The goal is a balanced portfolio of unrestricted and restricted income from multiple source types: individual giving, foundation grants, corporate sponsorships, earned income, and recurring donations.

Revenue composition varies significantly by organizational age and size. According to Candid's analysis, organizations founded before 1990 demonstrate much greater diversification: 94% report foundation grants versus 81% for newer organizations; 67% report earned income versus 42%; and 66% report government funding versus 32%.

An informal but widely cited "Rule of Thirds" suggests no single revenue source should exceed 30-33% of total revenue. While not a formal standard, this guideline reflects sound risk management: when one funding stream represents more than a third of your budget, you're highly exposed if that source disappears or decreases.

Unrestricted revenue deserves special attention. Unlike restricted grants that must be spent on specific programs or purposes, unrestricted funds give organizational leaders maximum flexibility to respond to emerging needs, invest in infrastructure, build reserves, or pivot strategies. Cultivating unrestricted support — through individual donors, unrestricted foundation grants, or earned revenue — is one of the most effective ways to build the financial flexibility that restricted funding simply cannot provide.

Adequate Operating Reserves

An operating reserve serves as your organization's financial safety net, allowing you to continue functioning during revenue gaps, unexpected expenses, or external crises. The commonly recommended benchmark is 3-6 months of operating expenses, though some experts recommend up to 12 months depending on the organization's revenue volatility and risk profile.

Currently, the nonprofit sector falls dramatically short of this benchmark. 52% of organizations have three months or less of cash on hand, and 18% have just one month or less — meaning nearly one in five nonprofits is one payroll cycle away from crisis.

Determining the right reserve target requires examining your specific risk factors:

- Revenue concentration (higher concentration = higher target needed)

- Cash flow predictability (significant seasonal swings push the target higher)

- Fixed cost burden (higher fixed costs = higher target)

- External funding volatility (government contracts often delayed = higher target)

Building reserves requires a formal reserve policy — a board-approved document that defines the reserve target, conditions under which reserves can be used, and a replenishment plan. According to Propel Nonprofits, effective policies include five elements:

- Purpose — why the organization is building reserves

- Definitions — types of reserves, intended use, target calculations

- Assignment of authority — who can authorize use

- Reporting and monitoring — regular balance reporting

- Investment policies — how reserve funds are invested

Without this policy, reserves can easily erode through undisciplined spending or mission creep. Reserves exist to bridge temporary shortfalls — not to paper over ongoing structural deficits that require a different solution.

Financial Oversight and Transparent Reporting

The board of directors has a fiduciary responsibility to monitor financial performance through regular review of key financial statements — not just annual audits. According to the National Council of Nonprofits, "Boards of directors have a fiduciary duty to ensure that the assets of a charitable nonprofit are used in support of the charitable mission, and in accordance with donors' intent."

Healthy board-level oversight includes:

- Monthly or quarterly financial reporting to the full board

- Active finance committee that reviews statements in detail

- Clear financial KPIs tracked consistently over time

- Annual budget approval with multi-year context

- Regular audit review and management letter discussion

Strong internal oversight has a direct external benefit: it builds donor and funder trust. Research published in 2025 found positive associations between perceptions of financial transparency and perceived nonprofit performance — it reduces informational asymmetry and signals legitimacy to donors and funders alike.

The results are measurable: nonprofits achieving the Candid Seal of Transparency see an average 53% increase in contributions compared to those without it.

IRS Form 990 serves as a critical public accountability tool. Organizations must provide copies of their three most recently filed Form 990s upon request, and the form contains financial data, governance policies, executive compensation, and board composition. Treating the 990 as a transparency opportunity rather than a compliance burden helps build stakeholder confidence.

This is where outside financial leadership can add real value. One Abacus Advisory, for example, helps nonprofit boards by preparing clear financial statements, managing cash flow forecasting, and translating complex data into actionable governance insights — without the cost of a full-time hire.

Long-Term Strategic Financial Planning

Sustainable organizations think in multi-year financial horizons — not just the next annual budget cycle. A multi-year financial plan includes:

- Revenue projections based on realistic assumptions about donor retention, grant renewals, and new funding development

- Expense forecasting that accounts for inflation, salary increases, program expansion, and deferred maintenance

- Funding gap identification showing where revenue falls short of planned activities

- Scenario planning for economic downturns, funding disruptions, or major donor losses

- Strategic investment planning for capacity building, technology upgrades, or reserve accumulation

This approach transforms budgeting from a reactive annual exercise into a strategic tool that guides organizational decision-making. Multi-year planning reveals whether your current trajectory is sustainable or whether course corrections are needed before crises emerge.

Leadership Continuity and Organizational Capacity

Financial sustainability is undermined when key financial knowledge lives with one person — an executive director or finance staff member who may leave. Executive replacement costs run 50-200% of annual salary, and approximately 19% annual voluntary turnover affects the nonprofit sector.

Protecting against this risk requires succession planning for financial leadership roles, documented processes that don't live in anyone's head, and cross-training that distributes critical knowledge across the team. According to BoardSource, "The departure of an executive and the recruitment, hiring, and installation of a new executive is a complicated process that typically requires months of work."

During transitions, many nonprofits find that fractional financial leadership fills critical gaps. One Abacus Advisory, for example, has supported organizations like the Philadelphia Zoo during CFO and Controller transitions by maintaining financial operations, optimizing accounting systems, and ensuring continuity in reporting while permanent leadership is recruited.

Common Barriers That Undermine Nonprofit Financial Sustainability

Three barriers appear repeatedly across the sector — and recognizing them is the first step toward addressing them.

Funding Concentration

Funding concentration is the most widespread barrier to financial sustainability. Many nonprofits derive the majority of their income from one or two sources, leaving them highly exposed when those sources shift.

The 2025 government funding disruptions illustrated this vulnerability starkly. Nonprofits that depended on government for 42% of revenue experienced dramatically worse outcomes than the sector average: 29% decreased employees versus 15% overall; layoff projections rose from 3% to 7% generally but reached 15% for disrupted organizations; and hiring plans fell from 52% to 38%.

One survey respondent noted that losing federal funding — which accounts for one-third of their revenue — would "unravel" their entire system. Among nonprofits with government funding, 84% expect cuts.

The Financial Leadership Gap

Many small to mid-sized nonprofits lack dedicated financial leadership — relying on overextended executive directors or part-time bookkeepers instead of experienced financial strategists. Without that leadership, organizations default to reactive budgeting, missed forecasting opportunities, insufficient board reporting, and compliance vulnerabilities.

A full-time CFO salary with benefits often exceeds organizational budget capacity. Fractional CFO services provide an alternative: executive-level financial and operational expertise without the cost or commitment of a full-time hire.

Fractional CFO services typically include:

- Designing and monitoring financial processes

- Overseeing budgeting, forecasting, and cash flow management

- Ensuring compliance with nonprofit accounting standards

- Scenario planning for funding alternatives

- Technology implementation and optimization

- Translating complex financial reports into board-ready insights

- Creating custom real-time dashboards

One Abacus Advisory specializes in this model, pairing nonprofits with senior financial leadership scaled to their actual budget and operational needs.

Chronic Under-Investment in Infrastructure

The third barrier is systematic under-investment in infrastructure and financial systems. Many nonprofits divert all resources toward programs and avoid investing in accounting technology, financial training, or reporting systems — ultimately creating inefficiency and financial blind spots that cost more over time.

This pattern is driven by what researchers call "the nonprofit starvation cycle." The cycle operates in three steps:

- Funders have unrealistic expectations about nonprofit operating costs

- Nonprofits feel pressure to conform to those expectations

- Nonprofits underspend on overhead and underreport expenditures, which reinforces funders' unrealistic expectations

Research examining 220,000+ IRS Form 990s found that nonprofits reported overhead of 13-22%, but actual rates were 17-35%. More than one-third reported zero fundraising costs on Form 990s; one in eight reported zero management and general expenses.

Government contracts typically cap indirect expenses at 15%, with foundation allowances running 10-15%. For context, average overhead rates for for-profit service industries are never below 20%.

In 2013, GuideStar, Charity Navigator, and BBB Wise Giving Alliance issued a joint letter denouncing the overhead ratio as a valid indicator of nonprofit effectiveness, calling for an end to overhead-based evaluation. Yet the pressure persists.

The human cost accumulates: 45% of nonprofit staff are projected to seek new employment in the next five years, with 49% citing inadequate pay. Underinvesting in infrastructure doesn't just affect systems — it drives away the people organizations depend on.

How to Build a Nonprofit Financial Sustainability Plan

Building a sustainability plan is not a one-time exercise — it's a living document that requires regular review and adaptation. This five-step framework provides a practical roadmap.

Step 1: Assess Your Current Financial Position

A thorough financial assessment involves:

- Analyzing current revenue by source — Calculate what percentage each funding stream represents and identify concentration risks

- Reviewing 2-3 years of financial statements — Look for trends in revenue growth, expense patterns, operating margins, and reserve levels

- Calculating months of liquid operating reserves — Divide unrestricted liquid net assets by average monthly operating expenses

- Examining cash flow patterns — Identify seasonal fluctuations, payment delays, or timing mismatches between revenue and expenses

- Identifying structural deficits or deferred needs — Note whether the organization consistently spends more than it earns or has postponed critical investments

A strong assessment goes beyond reviewing numbers — it surfaces the structural patterns and control gaps that create long-term risk. One Abacus Advisory's financial assessments are built around exactly this kind of diagnostic work, pairing system reviews with actionable recommendations specific to each organization's situation.

Step 2: Diversify and Strengthen Your Revenue Base

Once you understand where your revenue stands, the assessment findings become the foundation for a diversification strategy:

- Identify which new income streams are realistic for your size and mission

- Set specific targets for unrestricted revenue growth

- Build multi-year donor cultivation pipelines

- Develop earned income opportunities aligned with mission

- Establish recurring giving programs to improve predictability

- Expand foundation and corporate grant prospects

Focus on sources that reduce concentration. If 50% of revenue comes from one government contract, diversification doesn't mean adding more government contracts — it means building individual donor capacity, earned income, or foundation support.

Step 3: Establish and Fund an Operating Reserve

Creating a reserve requires three actions:

Set a reserve target. Based on your risk profile, determine an appropriate goal — typically 3-6 months of operating expenses. If monthly expenses average $50,000, a three-month reserve equals $150,000.

Adopt a board reserve policy. Document the purpose, target amount, conditions for use, authorization process, and replenishment plan. The policy should clarify that reserves address temporary disruptions, not ongoing structural deficits.

Build the reserve incrementally. Few organizations can fund reserves all at once. Allocating 5-10% of any annual surplus is a realistic starting point. Some organizations also direct a portion of unrestricted contributions to reserves or run targeted reserve-building campaigns to accelerate progress.

Step 4: Strengthen Financial Oversight and Reporting Systems

Practical steps to improve oversight include:

- Establish a finance committee with defined responsibilities for financial review, policy recommendations, and audit oversight

- Set a monthly or quarterly reporting cadence so the board receives and discusses financial statements consistently

- Define financial KPIs — months of cash, revenue concentration ratio, operating margin, and program expense ratio

- Invest in accounting platforms like NetSuite, Sage Intacct, or QuickBooks Online that generate nonprofit-specific reports

The right accounting platform makes a real difference in reporting speed and accuracy. One Abacus Advisory's system optimization work — covering configuration, workflow automation, and staff training — helps nonprofits get more out of the tools they already have.

Step 5: Align Leadership and Build Internal Financial Capacity

The final step involves organizational alignment:

- Get board members, senior staff, and key stakeholders aligned on the sustainability plan

- Update the strategic plan to reflect financial sustainability goals

- Formalize financial policies (reserve policy, investment policy, gift acceptance policy)

- Invest in staff financial literacy through training and professional development

- Document financial processes to preserve institutional knowledge

- Consider succession planning for critical financial roles

For organizations without a dedicated CFO, fractional financial leadership fills that gap — providing board reporting support, long-term planning, and strategic oversight at a fraction of the cost of a full-time hire.

Key Financial Metrics Nonprofits Should Track for Long-Term Health

Financial sustainability is measurable, not just aspirational. Tracking the right indicators helps boards and leaders make informed, timely decisions rather than reacting to crises. Four metrics in particular give the clearest picture of where your organization stands — and where it's headed.

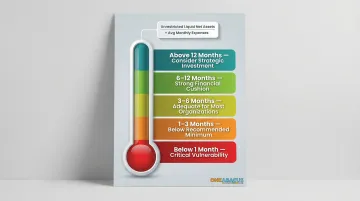

Months of Liquid Operating Reserves

This is the single most important indicator of nonprofit financial health. Calculate it by dividing unrestricted liquid net assets by average monthly operating expenses.

Formula: Unrestricted Liquid Net Assets ÷ Average Monthly Operating Expenses = Months of Reserves

Example: If you have $180,000 in unrestricted cash and investments, and monthly expenses average $50,000: $180,000 ÷ $50,000 = 3.6 months of reserves.

Benchmarks:

- Below 1 month: Critical vulnerability

- 1-3 months: Below recommended minimum

- 3-6 months: Adequate for most organizations

- 6-12 months: Strong financial cushion

- Above 12 months: May exceed mission need (consider strategic investment)

Context matters. Organizations with highly predictable revenue (endowment income, long-term government contracts) may operate safely with lower reserves. Those with volatile revenue (event-dependent, seasonal programs) need higher targets.

Revenue Concentration Ratio

This measures how dependent your organization is on its top funding sources. Calculate the percentage of total revenue represented by your largest one, two, or three sources.

Warning signs:

- Any single source exceeding 33% of total revenue

- Top two sources exceeding 50% of total revenue

- Top three sources exceeding 65% of total revenue

Organizations experiencing government disruptions in 2025 averaged 42% government dependence versus 28% sector-wide — and that concentration drove dramatically worse operational outcomes.

When concentration creeps past these thresholds, that's the signal to start cultivating new revenue streams — not after a major funder cuts back.

Program Efficiency Ratio and Overhead Ratio

While over-focusing on overhead ratios can fuel the nonprofit starvation cycle, tracking both metrics provides honest self-assessment and supports stakeholder communication.

Program Expense Ratio = Program Expenses ÷ Total Expenses

Charity Navigator recommends above 75% (65-70% is adequate). This shows what portion of spending directly advances mission versus supporting functions.

Important context: Overhead investment is mission-critical. As the 2013 joint letter from leading watchdog organizations emphasized, the overhead ratio is an unreliable measure of effectiveness. Don't chase artificially low overhead at the expense of organizational capacity.

Unrestricted Net Assets and Operating Surplus/Deficit Trend

Tracking unrestricted net assets over time reveals whether the organization is genuinely building financial cushion or eroding it — even if restricted revenue looks strong.

A multi-year trend of operating deficits, even small ones, signals a sustainability problem. Among repeat survey respondents, deficit rates rose from 13% in 2021 to 37% in 2024 — a nearly threefold increase in just three years.

What to track:

- Is unrestricted net assets growing, stable, or declining?

- Are you ending each year with a surplus or deficit?

- Is the trend improving or deteriorating?

A deficit in one year is manageable. A three-year downward trend demands a response: revenue growth, expense realignment, or a strategic repositioning of programs.

Frequently Asked Questions

What is a sustainability plan for a nonprofit?

A nonprofit sustainability plan is a strategic document outlining how the organization will maintain financial health over the long term. It covers revenue diversification, reserve management, leadership continuity, and financial oversight to ensure the mission continues regardless of external disruptions.

What are the three elements of financial sustainability?

The three widely cited elements are: diversified revenue streams (reducing dependence on any single source), adequate financial reserves (a buffer against disruptions), and sound financial management and oversight (including transparent reporting and strategic planning).

What is the 33% rule for nonprofits?

The 33% rule refers to the IRS public support test under IRC Sections 509(a)(1) and 509(a)(2), which requires at least 33⅓% of a 501(c)(3)'s total support to come from the public over a rolling five-year period. Failing this test can trigger reclassification from public charity to private foundation, with additional restrictions and excise taxes.

What is the 80/20 rule for nonprofits?

The 80/20 rule (Pareto Principle) typically refers to the observation that roughly 80% of donations come from 20% of donors. Research shows almost 80% of dollars come from major gifts above $5,000, highlighting the importance of major donor cultivation while warning against over-reliance on a small donor base.

What is the rule of three in nonprofit organizations?

The rule of three typically means: maintaining at least three months of operating expenses in reserve, holding at least three distinct revenue streams, and ensuring no single board member, donor, or funder holds outsized control. Together, these guardrails reduce concentration risk across finances, funding, and governance.

What are the 3 C's of fundraising?

The 3 C's of fundraising are Capacity (a donor's financial ability to give), Connection (their relationship to the organization), and Commitment (their dedication to the cause). Prioritizing donors who score high on all three tends to produce the most reliable, long-term giving relationships.

Ready to strengthen your nonprofit's financial sustainability? One Abacus Advisory provides fractional CFO and COO services tailored to mission-driven organizations seeking cost-effective financial leadership, strategic planning support, and board-ready reporting. Schedule a consultation to discuss how customized financial guidance can help your organization build lasting resilience.