Introduction

Ordinary nonprofits operate in a paradox: they're mission-driven but financially fragile, stretched between programmatic impact and survival. A 2025 Nonprofit Finance Fund survey found that 36% of U.S. nonprofits ended 2024 with an operating deficit — the highest rate in 10 years of tracking — while 52% hold just three months or fewer of cash on hand.

Yet "financial capacity" and "financial sustainability" are routinely used interchangeably, even though they describe fundamentally different conditions with different implications for organizational survival.

Financial capacity is your ability to survive short-term shocks and pursue long-term goals. Financial sustainability means maintaining that capacity over time at a rate that keeps pace with or exceeds inflation. This guide breaks down both concepts using a clear, practical framework developed by Woods Bowman in his widely cited 2011 study, so nonprofit leaders can accurately assess where they stand today and what they must build toward.

Key Takeaways

- Financial capacity = surviving short-term shocks; sustainability = maintaining that capacity at a rate that matches or exceeds inflation

- Most ordinary nonprofits measure health by cash on hand rather than the two metrics that actually matter: unrestricted net asset growth and total asset growth

- Declining net assets or asset growth below the ~2.6% long-term inflation rate signal erosion — even when an organization looks stable today

- Sustainability requires revenue diversification, healthy reserves, rigorous reporting, and long-term strategic planning

- Nonprofits without adequate financial infrastructure can access CFO-level leadership through fractional support — without the cost of a full-time hire

What "Financial Capacity and Sustainability" Actually Mean for Ordinary Nonprofits

Ordinary nonprofits — as defined by Woods Bowman in his 2011 framework — are active public charities that produce goods or services without large endowments and depend on ongoing revenue from donations, grants, earned income, or a mix of all three. This distinguishes them from institutional nonprofits with permanent capital and anchors this discussion in a specific, meaningful context: organizations that must continuously generate revenue to survive.

Nonprofit leaders must distinguish three related but distinct terms:

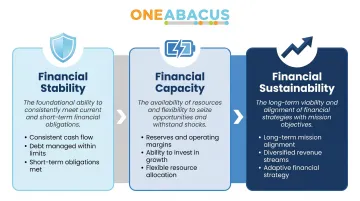

- Financial stability: Having enough revenue and fund balance to survive in the near term — covering payroll, delivering programs, meeting current obligations

- Financial capacity: Having both short-term resilience (unrestricted resources to absorb shocks) and long-term ability to maintain or expand services (growing asset base)

- Financial sustainability: Maintaining and growing financial capacity over time at a rate that keeps pace with inflation

Why the Distinction Matters in Practice

An organization can be "stable" right now — covering payroll, delivering programs — yet be unsustainable. If unrestricted net assets are declining year-over-year, or if total asset growth is lagging behind the long-term U.S. inflation rate of approximately 2.6%, the organization is slowly eroding its capacity to serve its mission even when nothing appears to be wrong.

That's where financial vulnerability (the inverse of sustainability) becomes critical — and it's rarely visible on a cash flow statement. It surfaces in eroding unrestricted reserves, deferred maintenance, and the inability to absorb any revenue disruption without cutting programs.

The NFF 2025 survey found that 18% of nonprofits have one month or less of cash on hand — leaving zero buffer against even minor revenue delays.

The Two Dimensions of Nonprofit Financial Capacity

Short-Term Capacity — Unrestricted Net Asset Growth

Short-term financial capacity, as defined by Bowman, shows up as positive annual growth in unrestricted net assets — the funds an organization controls without donor restrictions. This is the clearest signal that an organization generated enough revenue to cover expenses and build a buffer.

The practical metric to track is "months of spending":

Months of Spending = 12 × (Unrestricted Net Assets - Equity in Fixed Assets) / Annual Operating Expenses

This formula isolates liquid, unrestricted resources — removing buildings and equipment that can't be spent — and divides by operating expenses to show how many months the organization could operate if all revenue ceased.

Long-Term Capacity — Total Asset Growth and the Inflation Test

Long-term financial capacity requires positive annual total asset growth — meaning the organization's total asset base is growing, not just holding steady. This growth must meet or exceed the long-term inflation rate.

An organization that breaks even every year but doesn't grow assets is actually losing ground — the replacement cost of its assets and the cost of delivering programs both rise with inflation.

With the 20-year average U.S. CPI inflation rate at approximately 2.6%, a nonprofit whose net assets don't grow at least at that rate is losing real capacity, even when nominal balances look stable.

The Integration of Both Dimensions

Neither dimension is sufficient on its own. Each creates a specific vulnerability:

- Short-term only: The organization stays perpetually cash-strapped, unable to absorb disruption or invest in growth

- Long-term only: The balance sheet looks healthy on paper, but a single funding gap can force program cuts or closures

- Neither: The organization is one bad quarter away from a crisis

Tracking both — months of spending for liquidity and total asset growth against inflation for sustainability — gives nonprofit leaders an honest picture of where their organization actually stands.

Financial Vulnerability: Why Ordinary Nonprofits Are Most at Risk

The Tuckman-Chang financial vulnerability model identifies four organizational factors that predict whether a nonprofit is at risk:

- Insufficient equity (low net assets relative to total assets)

- Low revenue diversification (dependence on one or two sources)

- Low administrative cost ratios (a sign of chronic underinvestment in operations)

- Thin or negative operating margins (inability to generate surpluses)

Ordinary nonprofits are exposed on all four dimensions because they operate lean by necessity, not design. Validation research by Tevel, Katz, and Brock (2015) confirmed this model as the best predictor of nonprofit financial vulnerability compared to competing frameworks.

The nonprofit starvation cycle compounds this vulnerability: funders reward low overhead, so nonprofits underinvest in infrastructure, financial systems, and staff capacity. This underinvestment reduces administrative cost ratios, which signals "efficiency" externally but creates fragility internally. The result is a cycle that makes sustainable operations structurally harder to achieve.

The numbers behind this cycle are stark. Gregory and Howard's Stanford Social Innovation Review study found that nonprofits routinely underreport overhead by 5–13 percentage points due to funder pressure, while government contracts cap indirect expenses at roughly 15%. In one documented case, a nonprofit spent 31% of a grant's value on reporting requirements while the funder allowed only 13% for indirect costs: a structural mismatch that forces cost-shifting and deepens underinvestment.

The Four Pillars of Nonprofit Financial Sustainability

Revenue Diversification

Reliance on a single funding source — whether government grants, one major donor, or program fees — concentrates revenue risk. Diversification across donative income (individual gifts, foundation grants, government grants), earned income, and investment income reduces revenue volatility and protects against shocks to any single stream.

Research by Jeon (2021) found that nonprofits with more diversified revenue portfolios exhibit lower financial vulnerability over time. The Urban Institute found that 60% to 86% of nonprofits receiving government grants would have operated at a loss without that funding, illustrating acute vulnerability in the current policy environment.

Diversification should be a board-level metric, tracked annually and built into strategic planning.

Reserve Funds and Liquidity

Reserves are the clearest expression of short-term capacity. The standard recommendation is 3–6 months of operating expenses in unrestricted, liquid reserves, with some subsectors requiring up to 12 months.

Key reserve requirements:

- Genuinely unrestricted and accessible (not tied up in fixed assets or temporarily restricted funds)

- Formally documented through a written reserve policy

- Policy defines target level, conditions for drawdown, and replenishment plan

- Board-approved and reviewed annually

The National Council of Nonprofits confirms that most nonprofits fall short of this benchmark, with the NFF data showing 52% have three months or fewer of cash on hand.

Financial Reporting and Oversight

Sustainable nonprofits maintain regular, accurate financial reporting — monthly statements of activities, statement of financial position, and cash flow — reviewed by both management and the board.

Board financial oversight should include:

- Budget-to-actual variance analysis

- Liquidity ratios and trends

- Net asset growth tracking

- Cash flow projections

Without this infrastructure, leaders cannot see capacity eroding in time to correct it. For many small-to-mid-size nonprofits, this level of oversight becomes achievable through fractional CFO support. One Abacus Advisory, for instance, provides CFO-level financial leadership sized to the organization's budget — without the cost of a full-time hire.

When Philadelphia Zoo needed to maintain financial continuity during a leadership transition, One Abacus Advisory optimized their NetSuite environment, improved month-end close processes, and strengthened board reporting until permanent leadership was in place.

Long-Term Strategic and Budget Planning

Budgets must be built on realistic, revenue-based forecasts — not aspirational targets. They should include explicit line items for reserve contributions and infrastructure investments, and be reviewed against actuals monthly.

Long-term planning includes:

- Scenario planning for revenue disruptions

- Succession planning for financial leadership

- Multi-year financial modeling that tests whether the organization is on a trajectory to maintain or expand mission capacity

One Abacus Advisory has worked with organizations like the American Swedish Institute to implement more effective budgeting and cash forecasting systems that provide timely, concise pictures of financial performance throughout the fiscal year.

Practical Steps to Move Toward Financial Sustainability

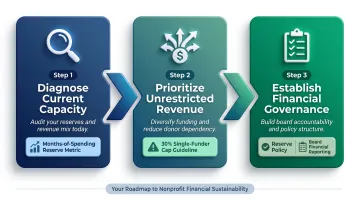

Step 1: Diagnose current capacity

Calculate your organization's months of spending metric and review year-over-year trends in unrestricted net assets and total assets. These two data points will reveal whether you are building capacity, holding steady, or eroding — and at what rate.

Step 2: Prioritize unrestricted revenue generation

Review your revenue mix for over-concentration in restricted grants or a single donor. Then identify one or two new income sources to develop over the next 12–24 months:

- Launch recurring giving programs that convert one-time donors into reliable annual contributors

- Develop earned income strategies tied to your mission and existing capabilities

- Reduce dependency on any single funder to below 30% of total revenue

Step 3: Establish formal financial governance

Strong governance doesn't require a large finance team — it requires consistent habits:

- Commit to monthly board financial reporting with clear variance notes

- Adopt a written reserve policy with a concrete savings target (typically 3–6 months of operating expenses)

- Build an annual budget approved by the board and tracked against actuals each quarter

If your organization lacks the internal capacity to maintain this infrastructure, consider working with a fractional financial leader who can build these systems and provide the CFO oversight your mission requires.

One Abacus Advisory has supported nonprofits through exactly these gaps, including the San Diego Food Bank and Laguna Playhouse, helping with leadership transitions, audit preparation, and day-to-day accounting while building sustainable financial systems from the ground up.

Frequently Asked Questions

What is the difference between financial capacity and financial sustainability for nonprofits?

Financial capacity is the ability to maintain or expand mission services, measured by unrestricted net asset growth and total asset growth. Financial sustainability is the ongoing condition of growing that capacity at a rate that meets or exceeds inflation — not a one-time achievement, but a continuous practice.

How do you measure financial capacity for a nonprofit?

Bowman's framework uses two metrics: short-term capacity is measured by positive annual unrestricted net asset growth (tracked as "months of spending"), and long-term capacity is measured by positive annual total asset growth that meets or exceeds the long-term inflation rate of approximately 2.6%.

How many months of operating reserves should a nonprofit maintain?

The standard benchmark is 3–6 months of operating expenses in unrestricted liquid reserves, with higher-risk organizations targeting up to 12 months. Reserves must be genuinely accessible — not tied up in fixed assets or restricted by donors.

Why are small nonprofits especially vulnerable to financial instability?

Funder pressure to minimize overhead drives chronic underinvestment in infrastructure — what Gregory and Howard call the nonprofit starvation cycle. Their research found nonprofits underreport overhead by 5–13 percentage points, leaving small organizations with thin margins and little buffer when funding shifts.

How does revenue diversification improve nonprofit financial sustainability?

Diversification reduces the impact of any single revenue source declining and lowers overall volatility. Jeon's 2021 study confirms that diversified revenue mixes directly correlate with lower financial vulnerability and stronger organizational resilience.

When should a nonprofit consider hiring a fractional CFO?

A fractional CFO makes sense when a nonprofit needs financial leadership — accurate reporting, reserve strategy, board-level oversight — but can't justify a full-time hire. It's particularly valuable during growth, leadership transitions, or financial stress. One Abacus Advisory has provided this support for organizations including the Philadelphia Zoo and Institute for Public Strategies.