Introduction

Nonprofit leaders face a growing tension: service demand continues to rise—85% of nonprofits expect increased demand in 2025 according to the Nonprofit Finance Fund (NFF)—yet funding has become less predictable. One-third of US nonprofits experienced government funding disruptions in early 2025, with 21% losing funding outright. Individual giving fluctuates, and major donors shift priorities without warning.

Most nonprofits have a fundraising calendar—grant deadlines, events, campaigns—but not a funding plan. A funding plan is a financial strategy that defines revenue mix, allocation rules, and sustainability thresholds. That gap has real consequences: 36% of nonprofits ended 2024 with an operating deficit, the highest rate in 10 years.

This article walks through a five-step framework for building a funding plan that holds up under pressure:

- Auditing your current revenue mix

- Building core funding pillars

- Diversifying strategically

- Setting allocation guardrails

- Creating an ongoing review process

Key Takeaways

- A sustainable funding plan defines revenue mix, reserves, and allocation rules—not just a fundraising to-do list

- Audit income sources to flag dangerous concentration—any single source exceeding 30–40% of revenue is a risk

- Build 2-3 primary revenue categories with real organizational capability, not superficial diversification

- Use allocation rules—33% concentration threshold, 80/20 stewardship prioritization—as financial guardrails

- Assign ownership, run quarterly reviews, and give boards the financial KPIs they actually need

What Separates a True Funding Plan from a Fundraising Calendar

A fundraising calendar is tactical—it lists events, deadlines, and campaigns. A funding plan is strategic—it defines revenue mix targets, funding ratios, risk thresholds, and multi-year financial projections. Many nonprofits operate with only the former and struggle with persistent financial instability.

That distinction separates financial stability from financial sustainability. Stability means having enough to operate today. Sustainability means your financial systems can withstand leadership changes, donor shifts, economic downturns, and funding disruptions over years—not just quarters.

The Bridgespan Group's framework draws a clear line between strategic financial planning—building a sustainable revenue model—and tactical fundraising, which focuses on individual campaigns.

NFF's "Full Cost" framework takes this further, identifying five components that revenue must cover beyond operating expenses:

- Working capital

- Reserves

- Change capital

- Fixed asset additions

- Debt principal repayments

As NFF puts it: "A break-even budget in an uncertain world can quickly become an unplanned deficit."

Step 1: Audit Your Current Revenue Mix

Categorize All Income Sources

Pull five years of financial data—not just last year. Categorize all revenue:

- Grants: Foundation and government

- Individual donations: Small gifts, mid-level, major gifts, planned giving

- Earned income: Fee-based services, consulting, training

- Corporate sponsorships: Cause-related partnerships

- Events: Galas, fundraisers

- Investment income: Interest, endowment returns

Five years of data reveals trends invisible in a single snapshot, showing whether revenue sources are growing, declining, or becoming more concentrated.

Identify Concentration Risk

Over-dependence on a single funding source creates real operational risk. Wegner CPAs identifies a Revenue Concentration Index above 30% as "high risk"—meaning the loss of one funder could disrupt operations.

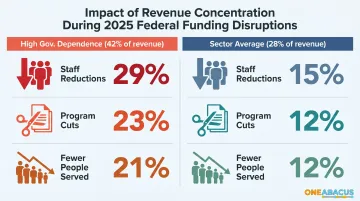

The 2025 federal funding disruptions made this concrete. Nonprofits that relied on government sources for 42% of revenue (versus 28% sector-wide) were far more likely to absorb painful cuts:

- Nearly twice as likely to reduce staff (29% vs. 15%)

- Nearly twice as likely to cut programs (23% vs. 12%)

- More likely to serve fewer people (21% vs. 12%)

One example: a nonprofit school in Kentucky lost $250,000 in federal funding overnight due to sudden DOGE cuts.

Assess Restricted vs. Unrestricted Funding

High proportions of restricted funding limit operational flexibility and prevent covering full costs. NFF identifies Liquid Unrestricted Net Assets (LUNA) as a key metric for measuring available liquidity. The scope of the problem is wide:

- 80% of nonprofits cite inability to cover full organizational costs as a top challenge

- 55% cite lack of multi-year funding as a contributing factor

Building unrestricted revenue isn't just a best practice—it's the financial buffer that keeps mission-critical programs running when restricted grants fall short.

Step 2: Build the Core Pillars of a Sustainable Funding Plan

Pillar 1: Defined Revenue Mix

A sustainable funding plan identifies a primary revenue category — the organizational engine — plus two or three supporting streams, then builds staff, systems, and infrastructure around those specific categories. Research from Bridgespan shows nonprofits that concentrate on fewer categories and build deep capability consistently outperform those spreading effort too thin.

Practical starting point:

- Select 2-3 primary revenue streams based on your organization's strengths and donor base

- Invest in staff expertise and systems specific to those streams

- Resist adding new revenue categories until existing ones are performing well

Pillar 2: Reserve Fund Policy

Operating reserves buffer against revenue disruptions and enable strategic opportunity.

Recommended targets:

- Minimum: 3-6 months of operating expenses

- Stronger benchmark: 6-12 months

Candid recommends each nonprofit set its own reserve goal based on cash flow and expense structure. At the low end, reserves should cover at least one full payroll. At the high end, reserves shouldn't exceed two years' budget.

Document a formal reserve fund policy governing how reserves are:

- Built (annual contribution targets)

- Accessed (board approval thresholds)

- Replenished (timeline after use)

Most nonprofits hold less than six months of cash in reserve — a gap that leaves them exposed when a major grant isn't renewed or an economic shift reduces donations.

Pillar 3: Restricted vs. Unrestricted Funding Targets

Set explicit goals to grow unrestricted revenue percentage over time. Strategies include:

- Building a recurring individual giving program (monthly donors)

- Cultivating major donors who give without program restrictions

- Negotiating unrestricted components in institutional grants

- Developing earned income streams

Pillar 4: Financial Reporting and Oversight Protocols

A funding plan needs monitoring infrastructure:

Key KPIs:

- Revenue concentration ratios

- Months of cash on hand

- Donor retention rate

- Restricted vs. unrestricted revenue percentage

- Grant renewal rate

Reporting cadence: Quarterly performance reviews and annual comprehensive strategy updates.

Pillar 5: Financial Leadership

Tracking KPIs and running quarterly reviews only works when someone owns the process. For many nonprofits operating without a full-time CFO, that accountability gap is where funding plans stall. Organizations like One Abacus Advisory provide fractional CFO and COO services built specifically for nonprofits — giving boards and executive directors the financial leadership needed to keep a funding plan active, monitored, and adjusted as conditions change, without the overhead of a full-time hire.

Step 3: Diversify Revenue Without Losing Strategic Focus

The 5 P's of Nonprofit Fundraising

Research from Rutgers Business Review identifies five underlying motivations for donor giving:

- Pride — sense of belonging or achievement

- Pity — empathy for suffering

- PR (Public Relations) — visibility or reputational value

- Personal Interest — rational or self-serving benefit

- Pleasure — the sheer joy of giving (found to be the strongest driver)

Each motivation calls for a different message and a different relationship. Map your donor segments to these drivers and your outreach will land with more precision — and generate stronger results.

Individual Giving as a Primary Revenue Pillar

Individual giving is the most resilient nonprofit funding source — unrestricted, donor-loyal, and less vulnerable to policy shifts. It accounts for approximately two-thirds of all US charitable giving and increased 8.2% in current dollars in 2024.

The case for investing in donor retention is straightforward once you look at the numbers:

Acquiring a new donor costs approximately $1.50 per dollar raised. Retaining one costs $0.20. That gap alone makes retention strategy a funding priority — not a nice-to-have.

Research from Neon One on recurring donors makes the value even clearer:

- Retention rate: 78–80% (vs. 32% for one-time donors)

- Average relationship: 7.7 years (vs. 1.7 years)

- Lifetime value: roughly 2x that of one-time donors

- Share of donor base: only 3–3.5% of supporters, yet they drive outsized long-term revenue

Grants and Government Funding — Strategic Not Reactive

Government funding comprises nearly one-third of nonprofit revenue and is the second-largest funding source sector-wide. 68% of nonprofits received government grants or contracts in 2022.

Strategic grant pursuit:

- Focus on funders with natural mission alignment

- Pursue multi-year commitments when possible (Trust-Based Philanthropy recommends multi-year unrestricted support)

- Diversify across foundation and government sources

- Avoid building operational dependence on restricted grant dollars

Foundation grantmaking surpassed $100 billion for the third consecutive year in 2024, representing significant opportunity for aligned organizations.

Corporate Partnerships and Earned Income

Corporate sponsorships and mission-aligned earned income add revenue diversity that individual giving and grants alone can't provide. Both require intentional development — they don't materialize from a single ask.

Key considerations before pursuing these streams:

- Corporate sponsorships work best when there's genuine brand alignment — a food bank partnering with a grocery chain, for example, rather than a generic logo placement

- Earned income (consulting, training, fee-based services) requires honest capacity assessment: staff time, legal/compliance review, and program infrastructure

- Start with one earned income pilot rather than launching multiple simultaneously; prove the model before scaling

DAF (Donor-Advised Fund) Readiness

The DAF market has grown significantly: total assets reached $326 billion in 2024, with $65 billion distributed in grants. DAF accounts totaled 3.56 million, and the payout rate (23.9%) far exceeds the 5% minimum required of private foundations.

Make it easy to receive DAF grants through your donation platform and actively cultivate relationships with DAF holders as high-value prospects.

Step 4: Set Allocation Rules, Reserve Targets, and Budgeting Guardrails

The 33% Rule

This practitioner guideline states that no single revenue source should represent more than one-third of total funding. Exceeding this threshold creates dangerous dependency.

While not a legal requirement, it aligns with IRS public support test standards — which require at least 33⅓% of support to come from public sources over five years for public charity classification.

Context matters — organization size, sector, and revenue predictability affect appropriate thresholds. Use 30–40% as your concentration risk trigger.

The 80/20 Rule in Donor Stewardship

The Pareto Principle applies broadly in nonprofit fundraising: approximately 80% of funding comes from 20% of donors or sources. Use this insight to prioritize:

- Major donor stewardship

- Grant renewals with top funders

- Corporate relationship management

- Planned giving cultivation

Knowing where your revenue concentrations lie also shapes how you plan for disruption — which is where scenario budgeting comes in.

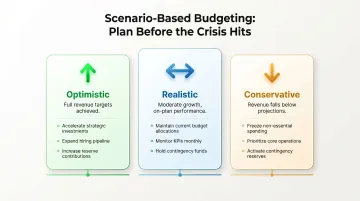

Scenario-Based Budgeting

A sustainable funding plan includes budget scenarios — at minimum three projections:

- Optimistic: Full revenue targets achieved

- Realistic: Most likely outcome based on current pipeline

- Conservative: Significant shortfall requiring operational adjustment

This structure allows pre-planned responses to revenue shortfalls rather than reactive crisis cuts.

United Way of Greater Los Angeles recommends scenario planning to "anticipate and respond to financial uncertainty before it becomes a crisis."

Reserve Fund-Building as a Line Item

Building reserves should be a budgeted expense, not an afterthought funded by year-end surpluses. Set an annual reserve contribution target (e.g., 5–10% of budget) and track progress toward your 6–12 month goal. Treat this as a non-negotiable expense category.

Step 5: Activate, Monitor, and Adapt Your Plan

Assign Clear Ownership

The funding plan needs a named owner with authority and financial literacy—typically the Executive Director, CFO, or senior development leader. For organizations without dedicated financial leadership, a fractional CFO or COO (such as those provided by One Abacus Advisory) can serve this function, keeping the plan active and accountable.

Set a Structured Review Cadence

Quarterly reviews should include:

- Revenue performance vs. targets by category

- Reserve fund balance and progress toward goal

- Donor retention metrics

- Emerging risks to current funding streams

- Variance analysis (timing vs. missing revenue)

In volatile funding environments, annual-only reviews leave too much room for undetected drift—quarterly check-ins are the minimum viable cadence.

Equip Your Board to Engage Strategically

Boards that only receive financial statements are operating reactively. Effective board engagement means reviewing funding mix health, tracking reserve progress, and actively supporting leadership in pursuing new revenue categories.

Board KPIs to track quarterly:

- Months of cash on hand (liquidity baseline)

- Revenue percentage from top funding source (concentration exposure)

- Restricted vs. unrestricted revenue ratio (operational flexibility)

BoardSource recommends boards approve annual budgets, ensure proper financial controls, review IRS Form 990 before filing, and ideally form separate audit committees for oversight.

When board and staff are aligned on these metrics, funding conversations shift from reactive problem-solving to proactive strategy—which is where sustainable plans are actually built.

Frequently Asked Questions

What common funding allocation rules (like the 33% rule and the 80/20 rule) should nonprofits follow when creating a sustainable funding plan?

The 33% rule advises that no single revenue source should exceed one-third of total funding, reducing concentration risk. The 80/20 rule recognizes that roughly 80% of funding comes from 20% of donors, guiding stewardship prioritization. Both are practical guidelines, not regulatory standards, helping organizations balance risk and focus resources.

What are the 5 P's of nonprofit fundraising?

The 5 P's represent core donor motivations: Pride (belonging/achievement), Pity (empathy for suffering), PR (visibility/reputation), Personal Interest (rational benefit), and Pleasure (joy of giving). Knowing which driver motivates each donor segment helps nonprofits tailor messaging and structure cultivation strategies that actually convert.

What is the difference between a funding plan and a fundraising plan for a nonprofit?

A fundraising plan is tactical, focusing on campaigns, events, and grant deadlines. A funding plan is a strategic financial document defining revenue mix targets, allocation rules, reserve goals, and long-term sustainability thresholds. The funding plan provides the financial strategy framework within which tactical fundraising activities operate.

How many months of operating reserves should a nonprofit maintain?

The commonly recommended range is 3–6 months as a minimum, with 6–12 months as the stronger target. The right amount depends on revenue predictability and expense flexibility—organizations with highly variable or restricted revenue should aim for the higher end to buffer against funding disruptions.

How do nonprofits balance restricted and unrestricted funding in their plans?

Unrestricted funding provides operational flexibility and the ability to cover full costs. A healthy funding plan sets explicit targets for growing unrestricted revenue through recurring individual gifts, major donor cultivation, and negotiating unrestricted grant components.

How often should a nonprofit review and update its funding plan?

Run quarterly performance reviews tracking concentration ratios, reserve levels, and donor retention, and conduct a full annual strategy review to reassess your revenue mix and multi-year projections. Trigger an off-cycle reassessment whenever a significant funding disruption or major organizational change occurs.