Introduction

Nonprofit leaders naturally direct their energy toward mission delivery—serving communities, advancing causes, changing lives. But passion alone doesn't keep the lights on. The organizations that sustain impact longest are those with disciplined financial foundations underneath the work.

When cash flow projections replace guesswork, when reserves provide breathing room during funding gaps, and when financial statements tell a clear story to boards and funders, nonprofits gain the stability to pursue their mission without every fiscal quarter becoming a survival exercise.

According to the Nonprofit Finance Fund's 2025 survey of 2,206 nonprofits, 52% have three months or less of cash on hand, and 18% operate with just one month of reserves. Meanwhile, 36% ended 2024 with an operating deficit—the highest rate in 10 years of survey data. These aren't abstract statistics. They represent delayed payrolls, deferred programs, and leadership teams making impossible choices between mission and survival.

This guide covers the unique characteristics of nonprofit finance, the roles and documents that matter most, how to build revenue resilience and reserves, and how to create a sustainability-oriented financial plan. Whether you're a board treasurer, executive director, or finance committee member, these fundamentals will help you move from reactive crisis management to proactive financial stewardship.

Key Takeaways

- Nonprofit finance uses fund accounting to track restricted and unrestricted funds separately, unlike for-profit businesses

- Clear financial roles—treasurer, CFO, bookkeeper, accountant, finance committee—drive accountability even when outsourced

- Four core financial statements plus Form 990 give boards and funders the visibility needed to make sound decisions

- Revenue diversification and 6–12 months of operating reserves are the most powerful capacity-building moves

- A sustainable financial plan weaves together budgets, risk scenarios, and board oversight—turning finance into a forward-looking tool, not just a compliance function

What Makes Nonprofit Finance Different from For-Profit Finance

Nonprofit accounting operates under distinct rules than for-profit business finance, driven by donor intent, public accountability, and IRS requirements. The technical standard governing this framework is FASB ASC 958, which covers revenue recognition, contribution reporting, functional expense allocation, and net asset classification.

Fund Accounting and Restricted vs. Unrestricted Revenue

Unlike for-profit businesses that track a single pool of money focused on maximizing shareholder returns, nonprofits must track funds separately based on donor intent and restrictions. This system—fund accounting—requires organizations to distinguish between:

- Net assets with donor restrictions: Funds that must be used for a specific purpose (a particular program, capital project, or time period)

- Net assets without donor restrictions: Funds the organization can deploy flexibly to cover any legitimate expense

This two-class system, formalized in FASB ASU 2016-14, replaced the older three-tier structure (unrestricted, temporarily restricted, permanently restricted) and simplified reporting—but the underlying principle remains: nonprofits must demonstrate stewardship of every dollar according to donor intent.

Unrestricted funds give nonprofits the flexibility to respond to emerging challenges, cover operational expenses, and weather funding gaps. The Charity CFO recommends that at least 50% of total revenue come from unrestricted sources to maintain that flexibility.

Over-reliance on restricted grants creates a counterintuitive problem: an organization can appear financially healthy on paper while struggling to pay rent or cover payroll because every dollar is earmarked for a specific program.

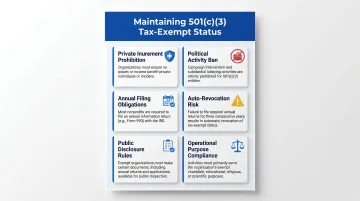

IRS Compliance and 501(c)(3) Requirements

Maintaining tax-exempt status under IRC Section 501(c)(3) requires more than filing an annual form. Organizations must satisfy both the organizational test (governing documents limit purposes to exempt activities) and the operational test (operated primarily for exempt purposes). Key requirements include:

| Requirement | Summary |

|---|---|

| Exempt purposes | Must operate for charitable, religious, educational, scientific, literary, or other qualifying purposes |

| Private inurement prohibition | Absolute prohibition on net earnings benefiting insiders |

| Political activity ban | Prohibited from political campaign intervention |

| Lobbying limits | No substantial lobbying activities |

| Annual filing | Must file Form 990, 990-EZ, or 990-N |

| Auto-revocation | Exempt status automatically revoked after 3 consecutive years of non-filing |

These requirements carry financial management implications that for-profit frameworks simply don't address. Every compensation decision, related-party transaction, and board vote must be documented with IRS scrutiny in mind.

Form 990 goes beyond a compliance checkbox — donors, foundations, and watchdog organizations review it before making funding decisions, making it one of the most consequential documents a nonprofit publishes each year.

Core Financial Roles Every Nonprofit Needs

Financial accountability requires clearly defined roles—even when those roles are outsourced, part-time, or shared. Confusion about who owns what creates gaps where critical decisions fall through or go unquestioned.

Board Treasurer

The treasurer serves as the primary financial oversight voice on the board. BoardSource defines this role as "responsible for stewarding the organization's resources," ensuring records are maintained, reviewing financial reports from staff, and interacting with accountants and auditors to keep the board informed.

What the treasurer does NOT do: Manage day-to-day finances, enter transactions, or make operational spending decisions. The treasurer's power lies in asking informed questions: Why did we miss our revenue target this quarter? How does our current cash position compare to our obligations over the next 60 days? What assumptions underpin this budget?

Finance Committee

This board subgroup bridges staff finance leadership and full board oversight. The finance committee reviews financial reports before board meetings, owns key policies (investment policy, reserve policy, gift acceptance), and provides a forum for detailed financial discussions that would overwhelm full board meetings. The National Council of Nonprofits distinguishes finance committees (which advise on budgets and financial administration) from audit committees (which oversee internal controls and typically select the independent auditor).

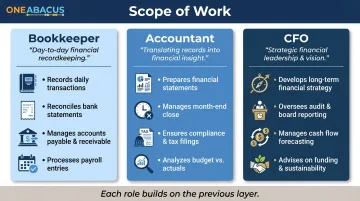

Chief Financial Officer (CFO)

The CFO provides strategic financial leadership: cash flow forecasting, budget development, financial risk assessment, and turning financial data into decisions leadership can act on. Candid's 2024 Nonprofit Compensation Report reports median compensation of $125,000 for top finance positions, ranging from $67,000 in religious organizations to $200,000 in science and technology research organizations.

The fractional CFO model for small-to-mid-sized nonprofits:

A full-time CFO typically becomes necessary when annual revenue exceeds $10–15 million. For organizations under that threshold, fractional CFO services deliver senior-level expertise at part-time cost — covering budgeting, cash flow forecasting, financial risk management, and audit preparation.

One Abacus Advisory provides fractional CFO services for nonprofits, offering strategic financial leadership without the overhead of a full-time hire. This model is particularly useful during growth phases, leadership transitions, and audit preparation.

Bookkeeper

The bookkeeper handles daily recordkeeping: recording transactions, managing payables and receivables, reconciling accounts, and maintaining the chart of accounts. Without clean, current transaction data, financial statements mislead rather than inform — and month-end close stretches from days into weeks.

Accountant

The accountant performs analytical work: preparing financial statements, managing audits and financial reviews, filing Form 990, and ensuring GAAP compliance specific to nonprofits (ASC 958). The distinction is practical: bookkeepers record what happened; accountants interpret what it means and ensure reporting meets regulatory standards.

The Financial Documents That Drive Nonprofit Decision-Making

Sound nonprofit financial management depends on the right documents — ones that plan and authorize spending, and ones that report what actually happened. Together, they give leadership and boards the information needed to make confident decisions.

Operating Budget

The operating budget is the annual financial plan, projecting revenue by source and expenses by function. It must be built on realistic assumptions, not aspirational fundraising numbers that set the organization up for disappointment. Actual-vs-budget variance reporting keeps the organization accountable throughout the year, surfacing problems early enough to correct course.

The Four Core Financial Statements

FASB ASU 2016-14 requires nonprofits to present four financial statements:

Statement of Activities (nonprofit income statement): Shows revenue, expenses, and change in net assets by restriction class. This statement answers the fundamental question: Is the organization growing or shrinking financially?

A deficit doesn't always signal crisis. Planned use of reserves for a capital project is very different from chronic overspending. Patterns over multiple years reveal sustainability or fragility.

Statement of Financial Position (balance sheet): Shows assets, liabilities, and net assets at a specific point in time. This snapshot reveals liquidity (Can we pay bills due in the next 30 days?) and long-term solvency (Are liabilities growing faster than assets?).

Statement of Cash Flows: Shows how cash actually moved through the organization regardless of accrual accounting entries. Revenue recognized on the Statement of Activities may not yet be cash in the bank: grants are often reimbursement-based, creating 30–90 day payment lags. This statement is critical for managing payroll and vendor obligations.

Statement of Functional Expenses: Unique to nonprofits, this statement breaks spending into program, administrative, and fundraising categories. Charity Navigator awards no financial metric points when program expense ratio falls below 50%, and BBB Wise Giving Alliance Standard 8 requires at least 65% of expenses go to programs. Donors, grantmakers, and watchdog sites all scrutinize this statement when evaluating organizational efficiency.

Form 990: Compliance and Public Transparency

Form 990 is both an IRS filing and a public document. Under IRC Section 6104, organizations must make their three most recent Form 990 returns publicly available. Major donors and foundations review it. Inaccuracies, high executive compensation relative to peer organizations, or poor program expense ratios can directly impact fundraising.

Failure to file for three consecutive years triggers automatic revocation of tax-exempt status — a death sentence for most nonprofits.

Chart of Accounts

The chart of accounts is the financial architecture that determines whether reporting is meaningful or unclear. Nonprofits should customize it to reflect their programs, funding types, and reporting needs rather than using generic templates. A well-designed chart of accounts lets leaders answer questions like:

- What does Program X actually cost when overhead is allocated?

- Which funding sources generate the highest unrestricted revenue?

Financial Policies

Policies provide guardrails that prevent costly mistakes and protect the organization's reputation:

- Gift acceptance policy: Protects the organization from gifts that carry unacceptable conditions, liabilities, or reputational risk

- Conflict of interest policy: Ensures board members disclose and step back from decisions where they have a personal financial stake

- Expense reimbursement policy: Establishes which expenses qualify for reimbursement and what documentation staff must provide

- Reserve policy: Sets the target reserve level, defines how funds can be accessed, and outlines a replenishment plan after use

These policies aren't bureaucracy for its own sake. They're practical shields against fraud, misunderstanding, and mission drift.

Building Financial Capacity: Revenue Diversification and Operating Reserves

Financial fragility typically stems from two sources: revenue concentration and inadequate reserves. Address both and the organization gains the stability to pursue its mission without every funding gap becoming a crisis.

Revenue Diversification: Distributing Risk

Over-dependence on a single funding source—a government contract, one major donor, a single foundation grant—is the most common financial fragility point. Candid's 2024 survey found that earned income accounts for 71% of total nonprofit revenue, with contributions at 18% and government funding at 11%. Only 7% of nonprofits rely solely on individual donors, and less than 1% rely solely on any single revenue stream.

Diversification distributes risk across:

- Individual giving (annual campaigns, major gifts, planned giving)

- Earned income (fees for service, social enterprise, membership)

- Institutional grants (foundations, corporations)

- Government contracts and grants

- Investment income (for organizations with endowments)

Newer organizations are particularly vulnerable to concentration risk, often launching with one or two major funders. Building a diversified portfolio takes years, but the effort protects programs when a single funder shifts priorities.

Operating Reserves: The Financial Shock Absorber

An operating reserve fund is distinct from project-specific funds or endowments—it's liquid, unrestricted cash available to cover expenses when revenue drops or unexpected costs arise.

Recommended targets:

- Minimum: 3–6 months of operating expenses

- Best practice: 6–12 months of operating expenses

BDO recommends nonprofits maintain at least six months in reserves. Yet NFF's 2025 survey reveals that 52% of nonprofits have three months or less of cash on hand, and 18% operate with just one month of reserves.

The reserve policy should document:

- Target amount (expressed as months of operating expenses)

- Circumstances under which reserves can be accessed

- Approval process for drawing down reserves

- Plan and timeline for replenishment

Reserves aren't a luxury or a sign of hoarding—they're the difference between weathering a crisis and closing programs.

Cash Flow Management: Timing Matters

Many nonprofits are technically solvent but cash-strapped due to grant reimbursement timing, seasonal fundraising cycles, or slow receivables. Reimbursement-based grants require organizations to spend first, then submit documentation for repayment—a process that can take 30, 60, or 90 days. During that waiting period, payroll, rent, and program costs still need to be covered.

Cash flow forecasting helps leaders anticipate gaps before they become crises. A 13-week rolling cash forecast showing expected inflows and outflows enables proactive decisions:

- Should we delay a hiring decision?

- Can we accept this new grant given the upfront costs?

- Do we need to draw from reserves this month?

Challenging the Overhead Myth

Administrative and fundraising expenses aren't waste—they're investments that allow programs to scale. In 2014, GuideStar, Charity Navigator, and BBB Wise Giving Alliance issued a joint letter pushing back against overhead ratios as the primary measure of charity effectiveness. The Ford Foundation raised its minimum indirect cost rate to 25% effective January 2023, explicitly citing the "nonprofit starvation cycle" caused by funders underpaying for indirect costs.

Nonprofits should calculate and communicate their true cost of operations rather than artificially suppressing overhead. Strong finance staff, effective technology systems, and professional development are prerequisites for sustainable impact—not line items to minimize.

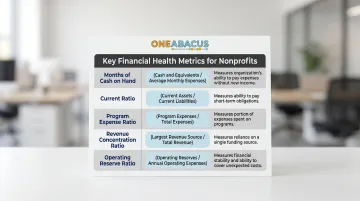

Key Metrics to Measure Your Nonprofit's Financial Health

Raw financial statements contain hundreds of numbers. Financial ratios turn that data into clear, usable signals. Tracking 3–5 key ratios regularly is more useful than producing monthly reports that nobody reads.

Essential Ratios for Nonprofit Boards

| Metric | Formula | What It Measures |

|---|---|---|

| Months of cash on hand | Total cash ÷ (annual expenses ÷ 12) | How long the organization can operate without new revenue |

| Current ratio | Current assets ÷ current liabilities | Short-term liquidity and ability to meet obligations |

| Program expense ratio | Program expenses ÷ total expenses | Percentage of spending directed to mission delivery |

| Revenue concentration ratio | Largest single revenue source ÷ total revenue | Dependence on any one funding stream |

| Operating reserve ratio | Unrestricted net assets ÷ annual operating expenses | Financial cushion available for shocks |

Sources: NFF, BBB WGA, Charity Navigator

These metrics are most powerful when tracked over time as trends, not evaluated as isolated snapshots. A declining cash position across three consecutive quarters signals real trouble — even if the most recent month looks fine. Board finance committees should review these ratios at every meeting and use them to probe what's driving the numbers: "Why has our revenue concentration ratio stayed above 60% for two quarters?" is a far sharper question than a nod of approval.

Creating a Financial Sustainability Plan for Your Nonprofit

A financial sustainability plan isn't a separate document filed away after completion—it's the integration of financial goals, risk scenarios, and leadership accountability into the organization's broader strategic plan. Financial health is driven by mission priorities, not managed in isolation by a finance department.

Key Components

A strong sustainability plan typically addresses five interconnected areas:

Multi-year financial projections model revenue and expenses over 3–5 years based on strategic plan assumptions. If the plan calls for expanding into two new counties, what will that cost? When do those programs become self-sustaining or attract dedicated funding?

Scenario planning means developing "best case," "expected," and "stress case" financial models. What happens if that major grant isn't renewed? If individual giving grows 15% faster than projected? Scenario planning helps boards make pre-authorized decisions before a crisis hits — for example: If Grant X is lost, we defer the new hire until Q3 and freeze discretionary spending until revenue stabilizes.

Dashboard reporting gives leadership the right information at the right level. Boards need 2-page dashboards showing variance to budget, key ratio trends, and cash runway — not 40-page monthly reports. Each metric should point toward a decision, not just document history.

Reserve accumulation requires a concrete path, not just a target. If current reserves sit at 2 months and the goal is 6 months, what closes that gap? An annual surplus of 5% of budget? A dedicated operating reserve campaign? Timeline matters — building reserves takes years of disciplined choices.

External financial partnership can accelerate all of the above, especially for organizations navigating growth, capital campaigns, or leadership transitions. One Abacus Advisory, for example, provides fractional CFO and COO support that helps nonprofits build these systems without the cost of a full-time executive hire. Whether the work involves optimizing accounting systems, preparing for audits, or developing cash forecasting tools, fractional leadership brings expertise calibrated to nonprofit scale and mission.

Frequently Asked Questions

What is fund accounting and why do nonprofits use it?

Fund accounting tracks revenue and expenses by designated purpose, allowing nonprofits to demonstrate stewardship of restricted donations and comply with donor intent and IRS requirements. Unlike standard business accounting—which treats all money as a single pool—it maintains separate ledgers for each restricted fund alongside unrestricted general operating resources.

How much should a nonprofit keep in its operating reserve?

Standard guidance recommends a minimum of 3–6 months of operating expenses in reserve, with 6–12 months as the best-practice goal. A written reserve policy should document the target amount, the approval process for accessing funds, and the replenishment plan after any drawdown.

What is the difference between a nonprofit bookkeeper and a nonprofit accountant?

A bookkeeper handles daily transaction recording, payables, receivables, and reconciliation—the recordkeeping foundation. An accountant performs financial analysis, prepares statements, manages audits, and files Form 990—the interpretation and compliance layer. Neither role replaces the forward-looking strategic oversight a CFO provides.

When does a nonprofit need a CFO vs. a fractional CFO?

A full-time CFO is typically justified when an organization's budget exceeds $10–15 million or when financial complexity demands daily executive attention. A fractional CFO delivers the same strategic expertise—budgeting, forecasting, risk management, compliance oversight—at a fraction of the cost, making it the practical choice for small-to-mid-sized nonprofits or those navigating transition.

What financial ratio matters most to foundation funders and major donors?

Program expense ratio—the share of total spending directed to mission activities rather than overhead—is the metric funders scrutinize most. BBB Wise Giving Alliance requires at least 65%; Charity Navigator awards no financial points below 50%. Be ready to explain your ratio in context, since artificially low overhead can signal underinvestment in essential infrastructure.

How can a nonprofit board improve its financial oversight without becoming a micromanager?

Boards improve oversight by focusing on key financial ratios and policy compliance rather than transaction-level details, establishing a finance committee to review reports before full board meetings, and ensuring leadership produces concise financial summaries that prompt informed questions, not rubber-stamp approvals. The treasurer and finance committee should ask "why" questions—why did revenue miss projections, why is cash declining—rather than drilling into line-item details like last month's supply spend.