Introduction

Government nonprofits operate in a uniquely high-stakes financial environment. Unlike private foundations or corporate entities, these organizations manage multiple restricted funding streams simultaneously—federal grants, state contracts, and local government awards—each with its own compliance obligations, allowable cost restrictions, and reporting deadlines.

A single misstep in financial recording or documentation can trigger audit findings that damage grantor relationships, draw escalated federal oversight, or result in withheld funding.

Between 2017 and 2021, auditors identified 44,104 Single Audit findings across organizations expending nearly $7 trillion in federal awards. Of these, 15,755 were classified as severe—contributing to modified audit opinions or material weaknesses in internal controls. Most troubling: 7,071 findings persisted for two or more consecutive years, signaling that many organizations struggle to implement lasting corrective action.

For government nonprofits, building an audit-ready close process is essential infrastructure — not a nice-to-have. This article breaks down what that process looks like, how it differs from a standard accounting close, and the common mistakes that determine whether your organization is truly prepared when auditors arrive.

Key Takeaways

- An audit-ready close is a structured, recurring financial discipline that produces books capable of withstanding Single Audit scrutiny—not a year-end event

- Government nonprofits face uniquely high stakes: Uniform Guidance (2 CFR 200) requires rigorous compliance documentation, fund-level reporting, and preparation of a Schedule of Expenditures of Federal Awards (SEFA)

- The process runs monthly through four stages: pre-close planning, account reconciliation, restricted fund compliance review, and financial statement finalization

- The most damaging mistake is treating audit readiness as an annual event instead of a discipline built into every close cycle

What Is the Audit-Ready Close Process for Government Nonprofits?

An audit-ready close process is a systematic, repeatable series of accounting tasks performed at the end of each reporting period—monthly, quarterly, and annually—designed to verify, reconcile, and finalize financial records so they are accurate, fully documented, and defensible under external audit review.

The result: clean financial statements that accurately reflect fund balances, proper revenue recognition for grants and contributions, and a documented evidence trail auditors can follow without gaps. That means every transaction traceable, every journal entry carrying a stated business purpose, and every restricted funding stream correctly classified.

How This Differs from a Standard Close

For government nonprofits, the close process must go well beyond basic GAAP compliance. Standard for-profit closes focus primarily on revenue recognition, expense matching, and balance sheet accuracy. Government nonprofit closes add multiple layers of complexity:

- Fund-level reporting: Restricted and unrestricted net assets must be tracked separately at all times, with every transaction tagged to the correct fund

- Grant expenditure tracking: Each federal award requires monitoring against its approved budget, with expenditures tested for allowability under Uniform Guidance cost principles

- Net asset classification by donor restriction: Under FASB ASC 958, nonprofits must classify all net assets as either "with donor restrictions" or "without donor restrictions," and properly release restrictions when conditions are met

- SEFA preparation: Organizations expending $1,000,000 or more in federal awards (effective for fiscal years beginning after October 1, 2024) must prepare a Schedule of Expenditures of Federal Awards listing every federal program by Assistance Listing Number (ALN), tracking pass-through awards, and disclosing subrecipient expenditures

Each of these layers creates discrete documentation obligations—and any gap in the close process becomes a finding during Single Audit review.

Why Government Nonprofits Face Unique Audit Pressures

Structural Complexity of Multiple Restricted Funding Streams

Government nonprofits rarely manage a single funding source. They simultaneously administer federal grants from HHS, DOE, or DOJ; state contracts with specific performance metrics; and local government awards, each carrying distinct reporting timelines, allowable cost rules, and compliance obligations.

Every funding stream must be correctly reflected in the close, with expenditures allocated appropriately and restrictions tracked separately.

This structural complexity creates compounding risk: a missed deadline on one grant report can trigger a domino effect of compliance failures across multiple awards.

Regulatory Framework: Uniform Guidance and Single Audit Requirements

The regulatory framework driving these requirements is codified in 2 CFR Part 200 (Uniform Guidance). As of October 1, 2024, nonprofits expending $1,000,000 or more in federal awards in a fiscal year must undergo a Single Audit — up from the prior $750,000 threshold, narrowing the pool of organizations required to comply. For those above the threshold, the expectations remain rigorous.

Single Audits go far beyond standard financial statement audits. They add:

- Compliance testing across specific program requirements (allowable costs, eligibility, reporting, subrecipient monitoring)

- SEFA preparation and accuracy verification

- Major program determination (auditors must test at least 40% of federal expenditures if the organization isn't classified as "low-risk")

- Subrecipient monitoring under 2 CFR 200.332 — verifying subrecipients aren't debarred, assessing their risk, reviewing performance, and issuing management decisions on findings

Consequences When the Close Process Is Inadequate

The cost of a weak close process is well documented. Recent GAO analysis of TANF programs found that among 37 states, auditors identified 162 TANF-related findings, of which 56 were material weaknesses. More troubling: 105 findings were similar to or the same as prior-year findings, and 37 had repeated for two or more years — with three remaining unresolved for over a decade.

For nonprofits, the consequences include:

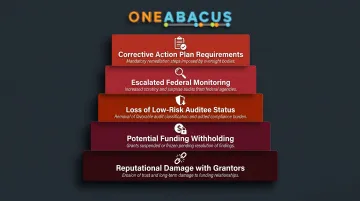

- Corrective action plan requirements with strict implementation timelines

- Escalated monitoring by federal awarding agencies

- Loss of "low-risk auditee" status, which increases required audit coverage from 20% to 40% of federal expenditures

- Potential funding withholding until corrective action is completed

- Reputational damage with grantors, making future awards harder to secure

How the Audit-Ready Close Process Works, Step by Step

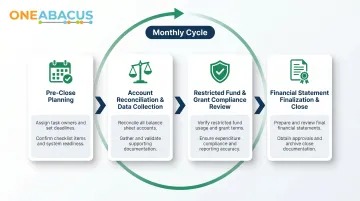

The audit-ready close process moves through four sequential stages. Quality at each stage directly determines audit readiness. This cycle should run monthly—not just at year-end—so that the annual close becomes a final review rather than a high-pressure scramble to reconstruct an entire year of transactions.

Step 1: Pre-Close Planning

Establish a master close calendar with task-level deadlines, assigned owners, and clear escalation points. This calendar must integrate compliance obligations alongside standard accounting tasks:

- Grant reporting deadlines for federal, state, and local awards

- Contribution cut-off dates to ensure revenue is recognized in the correct period

- SEFA preparation milestones (if applicable) to maintain a running schedule throughout the year

- Standard accounting tasks such as bank reconciliations, payroll processing, fixed asset depreciation, and accrual adjustments

Key principle: Compliance obligations must be built into the schedule from the start, not added reactively when a deadline approaches.

Step 2: Account Reconciliation and Data Collection

Reconcile all key accounts:

- Bank and investment accounts

- Receivables (including grant reimbursements due)

- Payables and accrued liabilities

- Payroll and related benefits

- Fixed assets and accumulated depreciation

- Grant balances—matching expenditures against approved award budgets

For government nonprofits, verify that all reimbursement requests or drawdowns are correctly recorded and that expenditures charged to each grant are allowable under the award terms.

Pull transaction data from subledgers, grant management systems, and external sources—such as bank statements or Payment Management System records.

Step 3: Restricted Fund and Grant Compliance Review

This is the step most commonly skipped by under-resourced finance teams. It's also the one most commonly flagged in Single Audits.

Review each active grant or government contract to confirm:

- Expenditures are allowable under 2 CFR Part 200, Subpart E (Cost Principles)

- Donor and funder restrictions are properly reflected in net asset classifications

- Compliance requirements—such as subrecipient monitoring under 2 CFR 200.332—have been fulfilled and documented

- Indirect cost rates (if applicable) are correctly applied and supported

- Every journal entry is tagged to the correct fund and purpose

Misclassifying restricted revenue as unrestricted—or vice versa—is one of the most common material findings in nonprofit audits. Fund coding errors caught here avoid costly audit findings later.

Step 4: Financial Statement Finalization and Close

With reconciliations and compliance confirmed, the final step is locking the period. Two close types apply:

- Soft close: Period is locked for new entries, but adjustments remain possible while errors are still being caught

- Hard close: Period is permanently sealed; corrections must post as adjustments in the following period

Before the hard close, finalize:

- Statement of Financial Position (balance sheet)

- Statement of Activities (income statement)

- Statement of Functional Expenses (required under ASC 958)

- Statement of Cash Flows

- Schedule of Expenditures of Federal Awards (SEFA), if a Single Audit applies

Internal review by senior finance staff or the CFO should occur before releasing statements to the board, auditors, or external stakeholders.

Key Compliance Factors That Affect the Close Process

Maintain a Running SEFA Throughout the Year

Don't reconstruct your SEFA at year-end. Track each federal award's cumulative expenditures by ALN throughout the year, maintain organized grant files (award letters, budgets, drawdown records, compliance certifications), and identify which programs are major programs for audit testing purposes.

Per 2 CFR 200.510, the SEFA must list individual federal programs by agency, include ALNs, identify pass-through entity names and numbers for subawards, report total federal expenditures per program and cluster, disclose amounts provided to subrecipients, and describe significant accounting policies.

Fund Accounting Discipline Is Non-Negotiable

Restricted and unrestricted net assets must be tracked separately at all times. Under FASB ASU 2016-14, net assets are now classified as:

- Net assets without donor restrictions (formerly "unrestricted")

- Net assets with donor restrictions (formerly "temporarily restricted" and "permanently restricted")

Every transaction affecting these classifications must be recorded correctly in real time. When restrictions are released (because time restrictions expire or purpose restrictions are satisfied), document and record the release in the period it occurs.

Documentation Standards Must Meet Auditor Expectations

Every journal entry should have:

- A stated business purpose

- Supporting evidence attached (such as invoices, grant agreements, board minutes)

- Clear identification of the fund or restriction affected

Expense approvals, grant expenditure authorizations, and payroll allocation methodologies should all be documented in writing and retrievable within minutes, not days.

Internal Controls for Government-Funded Environments

Address segregation of duties in grant management. A Utah state audit found 46% of government-associated nonprofits failed to maintain proper segregation of duties. 13 of 16 deficient entities had no compensating controls in place — a finding classified as a major weakness.

Key controls include:

- The person approving expenditures should not be the same person recording them

- Establish approval thresholds for purchases under federal awards

- Document a process for reviewing subrecipient performance and pass-through compliance

- Maintain a conflict-of-interest policy and procurement policy

Technology Directly Shapes Close Quality

Fund accounting software (such as NetSuite) enables real-time grant tracking, automated fund segregation, and audit trail generation. Organizations still relying on spreadsheets face a higher risk of misclassification and documentation gaps during the close. One Abacus Advisory works specifically with nonprofits to configure and optimize NetSuite for exactly these compliance requirements.

System optimization can include:

- Configuration to enforce fund-level accounting rules

- Automated workflows for grant expenditure approvals

- Custom reporting to generate SEFA data on demand

- User training to ensure staff understand how to properly code transactions

Common Mistakes That Undermine Audit Readiness

Treating Audit Readiness as a Year-End Event

The most costly mistake is waiting until fiscal year-end to perform reconciliations and compliance reviews. Organizations that operate this way are effectively trying to identify and correct months of errors under deadline pressure—a recipe for findings.

The data bears this out: Ventana Research found 59% of organizations take six or more business days to complete month-end close. For nonprofits with complex fund accounting requirements, delays compound quickly.

Each additional day of open close increases the risk of unreconciled transactions carrying forward and creating year-end audit adjustments.

Solution: Embed compliance reviews into every monthly close cycle. Make reconciliation, fund classification verification, and grant expenditure testing routine disciplines, not year-end emergencies.

Confusing GAAP Compliance with Uniform Guidance Compliance

A nonprofit can have technically accurate financial statements under GAAP and still receive material findings in a Single Audit. Why? Because grant expenditure tracking, subrecipient monitoring documentation, and SEFA preparation are separate compliance disciplines governed by 2 CFR Part 200, not FASB standards.

GAAP governs financial statement presentation. Uniform Guidance governs whether federal funds were spent according to program requirements. Satisfying one does not satisfy the other — and auditors check both independently.

Relying on Institutional Knowledge Without Documentation

When the person who knows "how we do it" departs, the close process breaks down. Auditors find inconsistencies, question methodology changes, and flag material weaknesses in documentation.

Solution: Document policies and procedures for every key financial process:

- Expense approval workflows

- Revenue recognition methodology

- Bank reconciliation procedures

- Grant expenditure coding rules

- Subrecipient monitoring steps

- SEFA preparation instructions

These documents serve as audit infrastructure. When turnover happens, they keep your close process consistent and your organization defensible under scrutiny.

Conclusion

An audit-ready close process for government nonprofits is ultimately about operating with the financial discipline and compliance structure that protects funding, supports mission-driven decisions, and builds lasting trust with the funders, boards, and communities you serve.

When you embed audit readiness into every monthly close cycle—rather than treating it as a year-end sprint—you reduce risk, improve financial visibility, and free your leadership team to focus on mission impact rather than scrambling through compliance emergencies.

Many government nonprofits lack the internal capacity to build and sustain this infrastructure on their own. Working with a specialized fractional CFO—such as One Abacus Advisory—provides a cost-effective way to establish the systems, close calendars, and compliance frameworks your organization needs without the overhead of a full-time hire.

Founder Lorin Port brings over 25 years of finance and accounting experience, with a focused nonprofit practice that has served organizations including the San Diego Food Bank, Philadelphia Zoo, and Laguna Playhouse. One Abacus Advisory helps nonprofits strengthen their financial operations and navigate audit cycles with confidence.

Frequently Asked Questions

What is the audit closure process?

The audit closure process covers everything that happens after fieldwork ends. It includes reviewing draft findings, issuing management responses, finalizing the auditor's report, and implementing corrective action plans to formally conclude the audit cycle.

What are the 5 C's of audit findings?

Auditors use the 5 C's to structure every finding in a management letter or Single Audit report:

- Criteria — the standard or requirement

- Condition — what was actually found

- Cause — why the gap occurred

- Consequence — the risk or impact

- Corrective Action — what will be done to fix it

What triggers a Single Audit for a government nonprofit?

A Single Audit is required when a nonprofit expends $1,000,000 or more in federal awards in a fiscal year, per 2 CFR Part 200. This threshold increased from $750,000 effective for fiscal years beginning on or after October 1, 2024.

How often should a government nonprofit reconcile accounts to stay audit-ready?

Reconcile all key accounts—including bank accounts, grant balances, receivables, and payroll—monthly. This ensures discrepancies are caught and corrected in real time rather than accumulated until year-end, when they become far more time-consuming to resolve.

What documents should be prepared before a nonprofit audit?

Core items to prepare include:

- Bank reconciliations and financial statements

- Grant agreements and related expenditure documentation

- Finalized SEFA (if applicable)

- Board meeting minutes and donor restriction documentation

- Prepared by Client (PBC) checklist provided by the auditor in advance

What is the difference between a soft close and a hard close in nonprofit accounting?

A soft close locks the period against new data entry while still allowing adjustments if errors are found. A hard close permanently closes the period. Any corrections after a hard close must be recorded as adjustments in the following period, making accuracy before the hard close essential.