This guide covers the purpose of a finance committee, who should serve on it, what it should actually do, and how it connects to broader financial leadership at your organization. Whether you're forming a new committee or strengthening an existing one, you'll find practical guidance grounded in sector standards and real-world application.

Key Takeaways

- Finance committees handle detailed financial oversight, freeing the board to focus on broader governance

- Keep committees to 3–5 members with financial expertise and independence from staff

- Cover the core duties: budget approval, financial monitoring, audit oversight, and compliance

- Use a committee charter to formalize purpose, authority, and accountability

- Smaller nonprofits can strengthen committee effectiveness by partnering with a fractional CFO

What Is a Nonprofit Finance Committee?

A finance committee is a standing board committee — meaning it exists permanently, meets regularly, and carries ongoing responsibilities. Unlike ad hoc committees formed for single projects, the finance committee provides continuous financial stewardship throughout the year.

The Governance Role

The committee doesn't replace the full board's financial responsibility. Instead, it does the detailed financial work — reviewing variance reports, monitoring cash flow, stress-testing budgets — then surfaces key findings and recommendations to the full board. According to BoardSource, the finance committee is "a principal finance committee that oversees the financial planning and management of the organization."

This division of labor keeps board meetings focused on strategy rather than line items. Complex financial data gets filtered into clear, decision-ready information before it ever reaches the full board.

Finance Committee vs. Audit Committee

Many nonprofits combine both functions within a single committee, but they serve distinct purposes:

Finance Committee responsibilities:

- Ongoing financial health monitoring (cash flow, budgets, reporting)

- Budget development and approval

- Financial policy oversight

- Revenue and expense trend analysis

Audit Committee responsibilities:

- External audit process management

- Internal controls review

- Risk assessment and mitigation

- IRS Form 990 review before filing

The National Council of Nonprofits clarifies: "Not every nonprofit has a separate audit committee that is responsible for the organization's internal financial controls and independent audit. In some nonprofits, the finance committee serves the dual role of both finance and audit committee."

Smaller organizations (typically those with budgets under $2M) often assign both functions to the finance committee. As budgets grow, separating the roles prevents conflicts of interest — the same people shouldn't oversee both spending decisions and the audit that reviews them.

Who Should Serve on Your Nonprofit Finance Committee

Ideal Committee Size

BoardSource recommends 3-5 members for nonprofit finance committees. This range balances competing needs:

- Too few (1-2 members): Limits perspective, creates succession risk, may lack quorum

- Too many (6+ members): Creates coordination challenges, dilutes accountability, slows decision-making

- Just right (3-5 members): Enables focused discussion, diverse viewpoints, and reliable quorum

Essential Expertise

At minimum, your finance committee should include members who cover three areas:

Financial or accounting credentials — At least one member should hold CPA-level expertise or CFO-level experience. They need to interpret financial statements, spot red flags, and apply GAAP principles with confidence.

Nonprofit-specific reporting knowledge — Someone familiar with fund accounting, Form 990 requirements, grant compliance, and restricted fund management. General accounting experience doesn't substitute for this.

Independence from staff and management — The IRS defines board independence as members who are not compensated as officers or employees, do not receive more than $10,000 as independent contractors, and have no family or business relationships with officers or directors. The majority of your committee should meet this standard to preserve oversight integrity.

The Board Treasurer's Role

The board treasurer typically chairs or co-chairs the finance committee and serves as the primary financial liaison to the full board. According to BoardSource, the treasurer "oversees all matters related to the organization's finances and budget, and usually serves as the chair of the finance committee." In practice, that translates to four core responsibilities:

- Sets committee meeting agendas

- Presents financial reports to the full board

- Serves as the first point of contact for financial questions

- Works closely with the executive director and finance staff

Including Non-Board Members

Non-board members with financial expertise can and often should serve on the finance committee. The Charity Lawyer Blog notes that while state law governs this practice, most jurisdictions permit non-board participation in a non-voting advisory capacity.

This approach offers valuable benefits:

- Fills knowledge gaps the current board may not cover internally

- Expands your talent pool without increasing board size

- Creates a pipeline for evaluating potential future board members

- Brings outside perspective that internal members can't always provide

One practical note before you recruit: confirm that your D&O liability insurance extends to non-board committee members. That coverage is not always included by default.

Core Responsibilities of the Finance Committee

Budget Development and Approval

The committee works with the executive director and finance staff to build an annual budget that reflects strategic priorities. Active participation means going beyond rubber-stamping staff proposals. The process requires:

- Understanding program costs and revenue assumptions

- Analyzing multi-year financial trends

- Questioning unrealistic projections

- Ensuring alignment with strategic goals

- Building in appropriate contingencies

Questions like "What if that grant doesn't come through?" or "Have we budgeted for known cost increases?" are exactly what separate active financial stewardship from rubber-stamp governance.

Financial Monitoring and Reporting

The committee reviews financial statements monthly or at minimum quarterly, typically including:

- Income statement with budget-to-actual comparison

- Balance sheet

- Cash flow statement

- Grant-specific or program financial reports

The committee's job is to compare actuals to budget, flag variances, and ensure the full board receives timely, accurate, and understandable financial reports. According to the National Council of Nonprofits, the finance committee should ensure "interim financial statements are prepared" on a regular basis.

Internal Controls and Asset Safeguarding

The committee ensures appropriate financial policies and internal controls exist to protect the organization's assets from errors or misuse, including:

- Segregation of duties (different people handling authorization, recording, and custody of assets)

- Approval thresholds for expenses and contracts

- Expense reimbursement policies

- Cash handling procedures

- Document retention policies

These controls protect both the organization and the individuals handling its finances — and they create a documented trail that builds board and donor confidence.

Audit Oversight

The committee works with external auditors, reviews audit findings and management letters, and ensures findings are addressed. In smaller organizations without a separate audit committee, this function falls to the finance committee.

Key responsibilities include:

- Recommending auditor selection to the full board

- Serving as the primary liaison during the audit

- Reviewing the audit report and management letter

- Developing action plans to address any findings

- Monitoring implementation of corrective actions

Compliance and Regulatory Reporting

The committee ensures all financial reporting obligations are met, including:

- IRS Form 990 filings (annual information return)

- Grant reporting to funders

- State charitable registration and reporting

- Payroll tax filings

- Any industry-specific requirements

Missed or inaccurate filings can trigger IRS scrutiny, funder penalties, or loss of charitable registration — consequences that take far longer to repair than they take to prevent. The IRS Form 990 specifically asks whether a committee assumes responsibility for financial statement oversight, making this a publicly visible governance function.

Cash Flow and Reserves Management

The committee monitors liquidity by asking: Does the organization have adequate operating reserves?

The commonly cited benchmark is 3-6 months of operating expenses, though the National Council of Nonprofits notes there's no single standard that applies to all nonprofits. Context matters — a $500K organization with predictable government contracts has different reserve needs than a $5M organization dependent on annual fundraising campaigns.

The gap between benchmark and reality is significant. According to the Nonprofit Finance Fund's 2025 survey, **52% of nonprofits have 3 months or less of cash on hand**, and 18% have 1 month or less. The committee's role is to surface these risks early — before a delayed grant payment or unexpected expense becomes an operational emergency.

Key Questions Every Finance Committee Should Be Asking

Questions About Liquidity and Sustainability

These questions separate passive oversight from active stewardship:

- Do we have at least three months of operating reserves?

- What's our cash position at month-end compared to last year?

- Are we relying too heavily on one funding source?

- Do we have a line of credit if needed?

- What's our plan if [major funder] cuts back?

Questions About Program Efficiency and Spending

How much of every dollar actually reaches programs? That ratio matters to internal leadership and to the donors, grantmakers, and watchdog organizations evaluating your organization from the outside.

Key benchmarks:

- BBB Wise Giving Alliance requires at least 65% of total expenses on program activities

- Charity Navigator uses sliding scales: 85% for large organizations, 70% for small organizations

These aren't rigid pass/fail thresholds, but consistent deviations below them signal a conversation the committee needs to have — and a plan the organization needs to make.

Questions About Revenue Diversification

Over-reliance on a single revenue stream is one of the fastest routes to financial instability. The committee should push these questions regularly:

- What percentage of revenue comes from our top three sources?

- If we lost [major donor/grant], how would we respond?

- Are we actively cultivating new funding relationships?

- What's our strategy to diversify revenue over the next 2-3 years?

A Candid study on nonprofit revenue sources found that only 7% of nonprofits rely solely on individual donors, and less than 1% depend on earned income or government funding alone — most financially stable organizations maintain diversified portfolios by design.

Questions About Financial Trend Direction

Finance committee members should look not just at current-period numbers but at trends over time:

- Are deficits growing or shrinking?

- Is fundraising cost-per-dollar increasing?

- Are program costs per participant rising faster than revenues?

- What do three-year trends tell us about organizational health?

The Nonprofit Finance Fund frames financial health as forward-looking, not backward-facing — tracking revenue reliability, building consistent surpluses, and ensuring the organization can cover its full costs, including working capital and reserves, not just program expenses.

The Finance Committee Charter: A Framework for Accountability

A finance committee charter is a governing document that defines the committee's purpose, composition, authority, meeting frequency, and reporting responsibilities. Without one, accountability gaps emerge — especially when committee members rotate off and institutional knowledge walks out the door.

Key Elements a Charter Should Include

Purpose statement — why the committee exists, its governance role, and how it supports the full board

Member qualifications and term limits — required expertise, selection process, and rotation schedules

Meeting cadence — frequency (monthly or quarterly), quorum requirements, and remote participation policies

Scope of authority — what the committee decides independently, what requires full board approval, spending limits, and policy authority

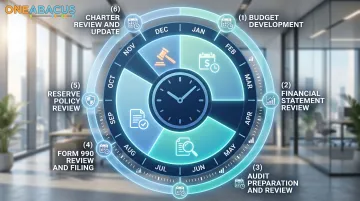

Annual calendar of duties:

- Budget development timeline

- Financial statement review schedule

- Audit preparation and review

- Form 990 review and filing

- Reserve policy review

- Charter review and update

BoardSource provides a committee charter template that covers these standard elements.

Reviewing and Updating the Charter

Having the right charter is only half the equation — keeping it current is the other. Review it annually to ensure it still reflects the organization's size, complexity, and governance needs. A charter written for a $500K organization may not serve a $5M organization well.

The BBB Wise Giving Alliance requires charities to assess organizational performance no less than every two years. Applying this standard to committee charters ensures they remain relevant and effective.

The Finance Committee and Financial Leadership: Working Together Effectively

The Critical Partnership

The relationship between the finance committee and the organization's senior finance staff or CFO creates a powerful check-and-balance system when it works well. The committee sets oversight direction and asks strategic questions, while finance staff or the CFO prepares reports, manages day-to-day operations, and brings analysis to the committee.

This partnership works best when:

- The CFO or finance director attends all committee meetings

- Staff provides reports at least 3-5 days before meetings

- The committee asks questions that push beyond the numbers

- Staff brings problems to the committee proactively, not after they've escalated

The Gap in Smaller Nonprofits

Many smaller nonprofits don't have a dedicated CFO or senior finance officer, leaving the finance committee without reliable analysis and proactive financial guidance. In these cases, the committee may be reviewing data without having the context to act on it effectively.

According to the Nonprofit Finance Fund's 2025 survey, 36% of organizations ended 2024 with an operating deficit — the highest in 10 years. Financial capacity challenges are widespread, particularly among smaller organizations.

The Fractional CFO Solution

Fractional CFO services offer nonprofits access to experienced financial leadership on a part-time basis that fits their budget and stage. Firms like One Abacus Advisory give the finance committee a knowledgeable partner who can:

- Prepare board-ready financial reports with narrative analysis

- Flag risks proactively before they become crises

- Provide strategic context the committee needs to fulfill its oversight role

- Support audit preparation and compliance requirements

- Optimize accounting systems and processes

For example, when the Philadelphia Zoo faced both CFO and Controller vacancies, One Abacus Advisory provided fractional support that optimized their NetSuite environment, improved month-end close processes, and enhanced board reporting.

That continuity gave the finance committee the financial stability and insights they needed during a critical leadership transition.

This model works particularly well for organizations with budgets between $1M–$10M: large enough to need sophisticated financial leadership, but not large enough to justify a full-time CFO hire.

Frequently Asked Questions

What committees should a nonprofit board have?

Most nonprofit boards maintain at minimum a finance committee, governance/nominating committee, and executive committee as core standing committees. According to BoardSource's Leading with Intent survey, the average number of standing committees is 4.1. Additional committees (fundraising, audit, programs) are added based on organizational size and needs.

What is the difference between a finance committee and an audit committee?

The finance committee handles ongoing financial management and oversight (budgets, cash flow, reporting), while the audit committee focuses specifically on the external audit process and internal controls. Smaller nonprofits typically assign both functions to the finance committee.

How often should a nonprofit finance committee meet?

Most finance committees meet monthly or at minimum quarterly. Monthly meetings allow the committee to review current financial statements and catch issues before they escalate.

Who should chair a nonprofit finance committee?

The board treasurer typically chairs the finance committee, serving as the financial liaison between the committee and the full board. A board member with strong financial expertise (such as a CPA or former CFO) can also serve in this role.

What financial reports should a nonprofit finance committee review?

Core reports include an income statement with budget-to-actual comparison, balance sheet, cash flow statement, and any grant-specific or program financial reports — reviewed monthly at minimum.

Does a small nonprofit need a finance committee?

Yes. Even small nonprofits benefit from a finance committee to ensure financial oversight is not concentrated in one person. Smaller organizations often supplement committee expertise with outside advisors or fractional financial leadership from firms like One Abacus Advisory.