Introduction

Nearly three-quarters of nonprofit leaders—74% according to a 2025 BTQ Financial survey—deal with cash flow problems at least occasionally, and 36% face them frequently. Many of these crises stem from a single root cause: operating without a comprehensive financial plan. A nonprofit financial plan is a strategic document that maps how an organization generates revenue, manages expenses, and allocates resources to sustain its mission. Without one, even well-funded nonprofits can find themselves unable to cover payroll between grant disbursements, forced to decline program opportunities, or scrambling to explain budget shortfalls to concerned board members.

If any of that sounds familiar, this guide is for you. It's written for executive directors, board members, and finance staff navigating a nonprofit challenge: unpredictable funding cycles, restricted grants with tight spending rules, and overhead budgets that leave essential infrastructure underfunded.

You'll work through 9 actionable steps organized into three phases—Assess and Align, Build the Plan, and Implement and Sustain—so you can build a financial plan that holds up in real-world conditions, not just on paper.

Key Takeaways

- Nonprofit financial plans differ from for-profit models: track restricted vs. unrestricted funds separately, model grant cycles, and meet IRS compliance requirements

- Nine steps across three phases—Assess and Align, Build the Plan, and Implement and Sustain—give your nonprofit a complete financial framework

- Beyond budgeting, sound plans include monthly cash flow forecasting, scenario planning for funding gaps, and transparent reporting to maintain donor trust

- Small and mid-size nonprofits often benefit from fractional CFO support to build financially sound plans without full-time hiring costs

What Is a Nonprofit Financial Plan and Why Does It Matter?

A nonprofit financial plan is a comprehensive, mission-aligned strategy covering projected revenues, anticipated expenses, cash flow management, financial goals, and key performance indicators. It differs from a standalone annual budget, which is simply a snapshot of income versus expenses for a single period.

The National Council of Nonprofits defines a budget as "a guide that can help a nonprofit plan for the future as well as assess its current financial health." A financial plan goes further — it's a living strategic document tied to long-term mission outcomes, risk management, and stakeholder accountability.

Your budget tells you what you plan to spend this year. Your financial plan explains how you'll sustain operations through funding gaps, what reserves you're building, and how financial resources connect to your three-year strategic priorities.

Candid's 2020 research modeled 315,698 US nonprofits across crisis scenarios and found that 4% would close under normal conditions — a figure that jumped to 11% in a realistic crisis, with 22,000 additional closures directly tied to financial instability.

Nonprofits without a formal financial plan are more exposed to:

- Funding gaps when a major grant doesn't renew

- Grant compliance failures that jeopardize future awards

- Cash flow shortfalls that arrive without warning

- Leadership-driven missteps that drain reserves before problems are visible

Organizations with a financial plan can identify liquidity problems months before they hit and communicate financial reality clearly to boards and funders. That shifts financial management from reactive crisis response to proactive strategic leadership.

Phase 1: Assess and Align (Steps 1–3)

Step 1: Understand Your Nonprofit's Financial Model

Start by mapping your revenue streams and categorizing each as restricted or unrestricted. This distinction fundamentally shapes how flexible your financial plan can be.

Primary revenue sources for US nonprofits (Giving USA 2025):

- Individual donations: $392.45B (66.2% of all giving)

- Foundation grants: $109.81B (18.5%)

- Bequests: $45.84B (7.7%)

- Corporate sponsorships: $44.40B (7.5%)

- Government grants/contracts: 29% of total nonprofit revenue (Urban Institute, 2024)

Restricted vs. unrestricted funds: Restricted funds carry donor-imposed limitations on spending. A grant for youth programming can't be redirected to cover rent; unrestricted funds can cover overhead, respond to emergencies, or seed new initiatives.

Managing this distinction is more complex than most organizations expect. According to BTQ Financial, 93% of nonprofits need to reclassify funds more than once per year, and over 36% reclassify quarterly.

Your funding cycle shapes your cash flow as much as your revenue total does. Grant-dependent organizations face very different timing realities than donation-reliant ones:

- Government contracts may not disburse for 60-90 days after invoicing

- Foundation grants often pay in installments tied to milestones

- Individual donations spike in Q4 but drop off sharply in Q1-Q3

Your financial plan must model when cash actually arrives, not just how much is expected.

Step 2: Review Historical Financial Data and Key Health Ratios

Pull 2-3 years of core financial statements: Statement of Activities (your nonprofit income statement), Statement of Financial Position (balance sheet), and Cash Flow Statement. These documents reveal spending patterns, revenue trends, seasonal fluctuations, and reserve levels that inform realistic projections.

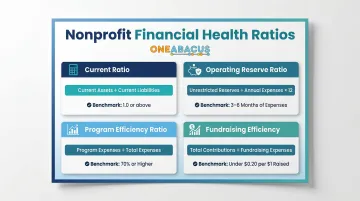

Calculate these financial health ratios:

| Ratio | Formula | Benchmark |

|---|---|---|

| Current Ratio | Current Assets / Current Liabilities | 1.0+ (you have enough liquid assets to cover near-term obligations) |

| Operating Reserve Ratio | Unrestricted Reserves / Annual Expenses × 12 | 3-6 months of expenses |

| Program Efficiency Ratio | Program Expenses / Total Expenses | 70%+ (Charity Navigator); 65%+ (BBB) |

| Fundraising Efficiency | Total Contributions / Fundraising Expenses | Spend less than $0.20 per $1 raised |

Operating reserves are critically low sector-wide. The National Council of Nonprofits reports that a minority of nonprofits hold more than 6 months of reserves, and many report fewer than 3 months. If your organization falls into this category, your financial plan must prioritize reserve building.

This assessment step is also where an outside perspective pays off. A fractional CFO with nonprofit-specific expertise can surface risks that internal teams often miss: grant compliance gaps, inefficient fund tracking, or reporting structures that obscure the real financial picture.

When the Philadelphia Zoo faced simultaneous departures of its CFO and Controller, One Abacus Advisory conducted a comprehensive accounting assessment that identified opportunities to optimize their NetSuite environment and strengthen board reporting, stabilizing operations through a critical leadership gap.

Step 3: Align the Financial Plan with Your Strategic Mission Goals

Every financial decision in your plan should trace back to your mission and strategic priorities. If a program isn't reflected in the budget, it won't get funded. If a goal isn't tied to financial resources, it won't get done.

Use your organization's strategic plan (or board-approved priorities) as the framework for financial resource allocation:

- Programs to grow: Allocate incremental funding for staff, materials, and infrastructure

- Programs to sustain: Maintain current funding levels with inflation adjustments

- Programs to wind down: Plan phase-out timelines and reallocate resources

The American Swedish Institute worked with One Abacus Advisory to implement a more effective budgeting and cash forecasting system. The result was a concise, timely picture of financial performance throughout the fiscal year, giving leadership real numbers to act on instead of end-of-quarter surprises.

Ask these alignment questions:

- Does our budget reflect our top three strategic priorities?

- Are we funding infrastructure (technology, staff development, systems) adequately to support program growth?

- Do restricted funds align with programs we're actually committed to delivering?

Phase 2: Build the Plan (Steps 4–6)

Step 4: Build a Realistic Budget That Accounts for True Costs

A mission-aligned budget must include both direct program expenses and full overhead costs: salaries and benefits, rent, technology, insurance, legal and accounting fees, and fundraising expenses. Underreporting overhead creates budgets that fail in execution and erodes donor trust when reality diverges from projections.

Understanding where your ratios should land—and why—matters before you start entering numbers. Common nonprofit budgeting benchmarks:

The BBB Wise Giving Alliance Standard 8 requires at least 65% program spending. Charity Navigator awards full credit to organizations spending 70%+ on programs, with combined administrative and fundraising costs below 25–30%.

These are targets, not rigid rules. The "80/20 rule" (80% program, 20% overhead) is an informal guideline derived loosely from Pareto's economic principle—not a legal requirement. In 2013, the CEOs of GuideStar, Charity Navigator, and BBB jointly declared that "overhead is a poor measure of charity performance," urging donors and nonprofits to focus on impact rather than arbitrary ratios.

Organizational size and mission type affect realistic ratios. A small advocacy nonprofit may legitimately spend 35% on overhead because policy research requires specialized staff. A food bank distributing donated goods may operate at 15% overhead because the model is distribution-heavy and donation-light.

Build in financial cushions:

- Contingency line: 3–5% of total expenses for unexpected costs

- Reserve fund contribution: Treat this as a budget line item, not an afterthought

- Inflation adjustment: Apply realistic cost increases to multi-year projections

Step 5: Project Income, Expenses, and Cash Flow

Build forward-looking income projections by source, anchored to historical trends and adjusted for known changes: grant renewals or losses, planned fundraising campaigns, economic conditions, and donor behavior patterns.

Don't stop at annual projections. Because grant disbursements often lag award announcements and donations spike seasonally, a monthly cash flow projection—showing when money actually arrives versus when bills are due—is critical to avoiding liquidity crises even when annual revenues look healthy.

Seasonal giving concentration: Blackbaud Institute reports that 36.1% of annual charitable revenue arrives in Q4, with December alone accounting for approximately 18%. If your organization depends heavily on year-end giving, your cash flow plan must model quarterly seasonality and identify bridge funding or reserve draws for Q1–Q3 operations.

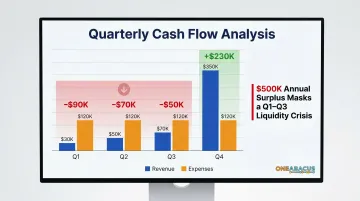

Example of a hidden cash flow gap:

Your annual budget projects $500,000 in revenue and $480,000 in expenses—a healthy $20,000 surplus. But when you model monthly cash flow, you discover:

- January–March: $30,000 in revenue, $120,000 in expenses = $90,000 shortfall

- April–June: $50,000 in revenue, $120,000 in expenses = $70,000 shortfall

- July–September: $70,000 in revenue, $120,000 in expenses = $50,000 shortfall

- October–December: $350,000 in revenue, $120,000 in expenses = $230,000 surplus

Without a cash reserve or line of credit, you'll face a liquidity crisis in Q2—even though your annual numbers are sound.

Step 6: Set Up the Right Accounting System and Fund Tracking

Nonprofits are legally required to track restricted funds separately from unrestricted funds under FASB ASC 958 (amended by ASU 2016-14). This distinction must be built into your accounting system, not managed manually on spreadsheets.

Fund accounting requirements:

FASB ASC 958 establishes:

- Two required net asset classifications: Net Assets Without Donor Restrictions and Net Assets With Donor Restrictions

- Functional expense reporting: expenses by both nature (salaries, rent) and function (program, admin, fundraising)

- Liquidity disclosure: availability of financial assets to meet cash needs within one year

Practical system requirements:

Your nonprofit accounting system must:

- Track funds by program/project and restriction type

- Generate IRS-required reports (Form 990 support)

- Manage grant compliance and drawdown tracking

- Produce board-ready financial statements with variance analysis

- Support month-end close processes efficiently

Cloud-based nonprofit-specific platforms like NetSuite for Nonprofits or QuickBooks Nonprofit handle these requirements far better than general accounting software retrofitted for nonprofit use.

When the San Diego Food Bank faced a Finance Director transition, One Abacus Advisory stepped in with interim financial leadership—keeping month-end closings on schedule and the organization's NetSuite environment delivering accurate, timely reports without disruption. That kind of continuity is what purpose-built systems and experienced support make possible.

Phase 3: Implement and Sustain (Steps 7–9)

Step 7: Conduct Risk Analysis and Scenario Planning

Model at least three scenarios—base case, optimistic, and conservative/stress case—that reflect potential funding disruptions so leadership has pre-built response plans rather than improvising under pressure.

Common funding disruption scenarios:

- Major grant not renewing (model loss of 20-40% of revenue)

- Donor giving declining by 15-25%

- Sudden program cost increase (salary adjustments, rent increase, regulatory change)

- Government contract payment delays extending 60-90 days

Operating reserve fund: Your financial buffer should cover 3-6 months of operating expenses. The National Council of Nonprofits recommends boards adopt formal reserve policies specifying:

- Amount to be set aside

- Circumstances justifying reserve use

- Internal decision-making process for draws

- Repayment timeframe and plan

- Any board-imposed restrictions

Most nonprofits fall short of this benchmark — making reserve-building one of the highest-impact financial goals a board can set.

Step 8: Build Transparency Into Reporting for Donors and the Board

Financial transparency is both an ethical obligation and a practical fundraising tool. Research published in Nature (2025) found that donor perception of nonprofit financial transparency was positively associated with donor trust and perceived organizational performance, explaining 66.9% of variance in how donors rated effectiveness.

That trust translates directly to revenue: organizations meeting transparency standards receive 53% more in contributions than less transparent peers, and nonprofits with GuideStar Gold or Platinum seals receive approximately 11% higher average donations.

Board-ready financial reporting includes:

- Monthly or quarterly financial statements presented against budget with variance explanations

- Dashboard of key financial KPIs (see Step 9)

- Forward-looking cash flow update for the next 3-6 months

- Narrative explanations in language accessible to non-financial board members

Board members carry a legal duty of care over financial health. BoardSource identifies their core responsibilities as reviewing and approving the annual budget, signing off on the IRS Form 990, ensuring audits are conducted, and maintaining appropriate reserves.

In practice, transparent reporting often requires infrastructure that isn't yet in place. Laguna Playhouse and the Institute for Public Strategies both engaged One Abacus Advisory during crisis periods to stabilize day-to-day accounting and prepare for complex audits — ensuring boards received clear, timely information when it mattered most. That kind of fractional CFO support is often what makes consistent transparency achievable during transitions.

Step 9: Set KPIs and Establish a Regular Review Cycle

Track these financial KPIs consistently:

- Operating reserve ratio: Months of expenses covered by unrestricted reserves

- Program efficiency ratio: Percentage of total spending directed to programs

- Fundraising ROI: Dollars raised per dollar spent on fundraising

- Donor retention rate: Percentage of prior-year donors who gave again

- Days of cash on hand: Current cash / (annual expenses / 365)

- Budget variance: Actual vs. budgeted performance by major category

Review schedule:

- Monthly operational review: Finance staff and executive director compare actuals to budget, update cash flow projections

- Quarterly board review: Present financial statements, KPI dashboard, and any significant variances or risks

- Annual plan refresh: Update multi-year projections, adjust scenarios, revise strategic resource allocation

The AFP Fundraising Effectiveness Project (Q4 2025) reported overall donor retention at just 43.3%, with donor counts declining 3.6% year-over-year for the fifth consecutive year. Organizations tracking retention by donor segment—not just totals—can identify and address weaknesses before they compound.

None of this works as a one-time exercise. BTQ Financial found that 54% of nonprofit leaders reforecast quarterly or more often — and your plan should be updated whenever major funding changes occur, the organization enters a growth or transition phase, or leadership turns over. One Abacus Advisory structures fractional CFO engagements specifically to support this ongoing review cycle, providing continuity and financial expertise without the overhead of a full-time hire.

Common Financial Planning Mistakes Nonprofits Make

Underfunding or omitting overhead: The most damaging mistake is building a budget that omits essential infrastructure costs—technology, professional development, adequate staffing, fundraising systems—creating a structural deficit from day one. Organizations forced to drain reserves or cut programs to stay afloat often trace the problem back to this single planning gap. Budget for true costs rather than aspirational ratios that look good on paper but collapse in practice.

Over-reliance on a single funder: When one grant or donor represents more than 30-40% of annual revenue, your entire financial plan is built on a fragile foundation. Bridgespan Group research (2024) found that over 90% of nonprofits reaching $50M+ annual revenue concentrated funding in a single category—but for small and mid-size organizations, that level of concentration from one source is a significant risk. Treating diversification as a core planning principle—spreading revenue across government agencies, foundations, and individual donors—reduces that exposure before it becomes a crisis.

Treating the financial plan as a one-time annual exercise: Plans that aren't reviewed mid-year against actuals quickly become irrelevant, leading to budget overruns and missed course-correction opportunities. The National Council of Nonprofits recommends periodic budget reviews comparing projections to actual cash flow and expenses, with amendments as conditions change. Without regular review, budget variances compound quietly until they're too large to absorb.

Frequently Asked Questions

What are common budgeting rules for nonprofits (e.g., 33%, 80/20, 50/30/20)?

Common guidelines like the 80/20 rule (80% program costs, 20% overhead) and the 33% rule (no single revenue source exceeding one-third of total income) are useful benchmarks, not legal requirements. The right ratios depend on your organization's size, mission type, and funding model—there is no one-size-fits-all standard.

What are five good financial goals for a nonprofit's long- and short-term financial plan?

Five practical financial goals to target:

- Build a 3–6 month operating reserve

- Diversify so no single revenue source exceeds 33% of income

- Achieve a program efficiency ratio above 75%

- Maintain positive operating cash flow each quarter

- Reduce year-over-year budget variance to under 10%

What is the difference between a nonprofit budget and a financial plan?

A budget is a single-period income and expense projection. A financial plan is a broader strategic document that includes multi-year projections, cash flow forecasting, risk analysis, fundraising goals, KPIs, and alignment with the organization's mission and strategic priorities.

How often should a nonprofit update its financial plan?

Review and update the financial plan annually, aligned with your fiscal year, and conduct mid-year check-ins comparing actuals to projections. Trigger immediate updates after major funding changes, leadership transitions, or significant shifts in program scope.

Do small nonprofits really need a formal financial plan?

Small nonprofits need a financial plan more than larger ones—they have less cushion to absorb surprises. Even a simple one-page plan covering revenue projections, expense categories, cash flow timing, and a reserve goal provides meaningful protection and donor credibility.