Introduction

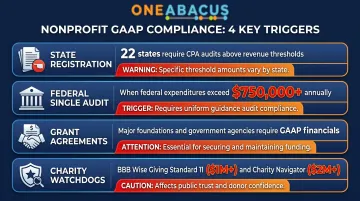

Nonprofit leaders and board members face a common frustration: GAAP compliance sounds like impenetrable accounting jargon, yet it directly affects grant eligibility, donor trust, and audit readiness. According to the National Council of Nonprofits, **22 states require independent financial audits** once organizations reach specific revenue thresholds, and the federal Single Audit threshold of $750,000 in federal expenditures triggers mandatory GAAP-compliant audits for thousands of nonprofits annually.

Those compliance stakes make GAAP literacy non-negotiable — yet most nonprofit leaders never received a plain-language explanation. This guide gives executive directors, board members, and finance staff exactly that: what GAAP requires, where nonprofits most often go wrong, and how proper reporting affects your Form 990 and funder relationships.

TL;DR:

- FASB's ASC Topic 958 governs nonprofit GAAP, covering financial reporting and transparency requirements

- Major funders, state regulators, and charity watchdogs require or expect GAAP-compliant financials

- Nonprofits must track net assets by donor restriction, allocate expenses functionally, and use accrual accounting

- Common errors: confusing conditions with restrictions, misreporting multi-year pledges, incorrect in-kind recording

- Getting these right protects your audit standing, your funder relationships, and your Form 990 accuracy

What Is GAAP, and Who Sets It?

Generally Accepted Accounting Principles (GAAP) is the standardized framework for recording and reporting financial information in the United States. It ensures consistency, comparability, and transparency across both for-profit and nonprofit organizations, allowing stakeholders to evaluate financial health on a consistent, comparable basis.

Permanence of Methods – Procedures cannot be changed between periods without disclosure and justification 5. Non-Compensation – Full disclosure without expectation of debt compensation 6. Prudence – Fact-based financial reporting without speculation 7. Continuity – Assumption that the organization will continue operating 8. Periodicity – Financial reporting divided into standard periods 9. Materiality – Complete disclosure of significant financial information 10. Utmost Good Faith – Honest financial reporting

Does GAAP Apply to Nonprofits?

Yes, GAAP applies to nonprofits. FASB's Accounting Standards Codification governs both for-profit and nonprofit entities, with nonprofit-specific guidance primarily under ASC Topic 958 (Not-for-Profit Entities). While not every nonprofit is legally mandated to follow GAAP, it is widely considered best practice and often becomes a practical requirement.

When GAAP Compliance Becomes Required

- 39 states plus the District of Columbia require charitable nonprofits to register for fundraising — and 22 states require independent CPA reviews or audits once income thresholds are crossed. Those audited statements must follow GAAP.

- Nonprofits expending **$750,000 or more in federal funds** annually must undergo a Single Audit under Uniform Guidance (2 CFR 200), which requires GAAP-compliant financial statements.

- Many private foundations and government agencies require GAAP-based financials before issuing grants, and some write it directly into grant agreements.

- BBB Wise Giving Alliance requires charities to "make available complete annual financial statements prepared in accordance with GAAP" under Standard 11.

- Charity Navigator uses Form 990 data (which parallels GAAP categories) for its ratings and expects organizations with annual revenue over $2 million to carry independent audits.

Nonprofit-Specific GAAP Guidance

Nonprofits follow sector-specific guidance on top of universal GAAP standards:

- Net asset classification under ASC 958 — with donor restrictions vs. without donor restrictions

- Contribution accounting under ASC 958-605 — distinguishing conditional from unconditional contributions

- Revenue recognition for exchange transactions under ASC 606

- Functional expense reporting across program services, management and general, and fundraising

- Qualitative liquidity disclosures explaining how liquid resources are managed

Why Nonprofits Should Follow GAAP

Funding Access and Grant Eligibility

GAAP compliance directly impacts funding access. Grant agreements frequently require GAAP-compliant financial statements, and major institutional donors request audited financials before making significant gifts. The $750,000 federal Single Audit threshold creates a concrete trigger: exceed this amount in federal expenditures, and GAAP-compliant audited statements become mandatory.

Donor and Stakeholder Trust

GAAP-based reporting enables apples-to-apples comparisons across organizations. When a donor evaluates multiple nonprofits, standardized financial statements reveal which organizations manage resources effectively and which struggle with overhead. Charity Navigator's ratings rely on Form 990 data structured around GAAP categories, and BBB Wise Giving Alliance's Standard 11 explicitly requires GAAP-prepared statements for organizations with gross income exceeding $1 million.

Regulatory Compliance and IRS Alignment

Many elements of IRS Form 990—required for 501(c)(3) organizations—align directly with GAAP principles:

- Part VIII (Statement of Revenue) parallels the GAAP Statement of Activities

- Part IX (Statement of Functional Expenses) mirrors GAAP functional expense analysis

- Part X (Balance Sheet) parallels the GAAP Statement of Financial Position

Not following GAAP can create discrepancies between your audited financials and Form 990, raising red flags for regulators and potentially jeopardizing tax-exempt status.

Better Decision-Making Through Accrual Accounting

The accrual accounting method required under GAAP provides leadership with a more accurate picture of financial health than cash-basis reporting. Revenue is recorded when pledged (not when cash arrives), and expenses when incurred (not when paid). This is particularly significant for nonprofits managing multi-year pledges, bequests, and conditional grants, all of which look very different under cash vs. accrual methods.

Strengthened Internal Controls

GAAP compliance inherently strengthens internal controls because following standardized procedures requires documentation, checks, and accountability. This helps detect or prevent fraud. For organizations without full-time financial leadership, a nonprofit-specialized fractional CFO — such as those at One Abacus Advisory — can help build these systems cost-effectively, without the overhead of a full-time hire.

How GAAP Applies Uniquely to Nonprofits

Accrual Accounting: The Foundation

GAAP requires accrual accounting: revenue is recorded when pledged (not received) and expenses when incurred (not paid). This contrasts with cash accounting, which records transactions only when money changes hands.

Two practical examples show why this matters:

- A $100,000 three-year pledge is recognized immediately at present value — not spread over three years as cash arrives

- A grant awarded in December but not spent until January appears as revenue in December and a liability until conditions are met

Revenue Recognition: Contributions vs. Exchange Transactions

Nonprofits must distinguish between two types of revenue:

Contribution revenue (ASC 958-605): Donations, grants, and gifts where the donor receives no commensurate value in return. These are recognized immediately if unconditional, or deferred until conditions are met if conditional.

Exchange transaction revenue (ASC 606): Fees for services, membership dues with specific benefits, and contracts where the funder receives a direct benefit in return. Revenue is recognized as performance obligations are satisfied.

Some transactions require bifurcation—separating a single payment into contribution and exchange components. For example, a $500 gala ticket might include a $150 meal (exchange transaction) and a $350 donation (contribution).

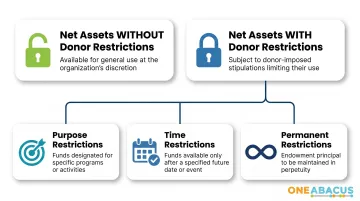

Donor Restriction Tracking

GAAP requires nonprofits to separate net assets into two categories (per ASU 2016-14, effective for fiscal years beginning after December 15, 2017):

- Net assets without donor restrictions (formerly "unrestricted")

- Net assets with donor restrictions (combines former "temporarily restricted" and "permanently restricted")

Within donor-restricted net assets, organizations must distinguish:

- Purpose restrictions: Funds designated for specific programs or activities

- Time restrictions: Funds not available until a future period

- Permanent restrictions: Endowment principal that must be maintained in perpetuity

Restricted funds cannot be repurposed without explicit donor consent and must be tracked separately in your accounting system.

Conditions vs. Restrictions: A Critical Distinction

This distinction trips up many nonprofits:

Donor-imposed conditions affect the timing of revenue recognition. Under ASC 958-605-25-11, a conditional contribution contains both:

- A barrier that must be overcome (measurable performance requirement, specific compliance protocol)

- A right of return to the donor or release from obligation if the barrier isn't met

Conditional contributions are recorded only when conditions are substantially met. Until then, any transferred funds appear as a refundable advance (liability), not revenue.

Donor-imposed restrictions affect the use of funds but don't delay recognition. An unconditional contribution with a purpose restriction is recognized immediately as revenue with donor restrictions.

Real-world scenario: A foundation awards $50,000 to serve 200 meals to homeless individuals. If the agreement allows the foundation to reclaim unspent funds if you fall short of 200 meals, the grant is conditional. Recognize revenue only as you meet that barrier.

If the agreement simply designates funds for meal programs without a recapture clause tied to performance, it's an unconditional restricted contribution. Recognize the full amount immediately as restricted revenue.

Functional Expense Allocation

GAAP requires nonprofits to analyze expenses by both:

- Natural classification: Salaries, rent, supplies, depreciation

- Functional classification: Program services, management and general (M&G), fundraising

Functional allocation shows stakeholders how much of every dollar goes toward mission-driven work vs. overhead. Form 990 requires this breakdown, and charity watchdogs use it to evaluate efficiency.

Key allocation rules:

- Human resources and finance/budgeting costs are generally classified as management and general

- Joint costs (activities with multiple purposes) must be allocated using reasonable methods

- Organizations must disclose their allocation methodology

Required Financial Statements Under GAAP for Nonprofits

GAAP requires nonprofits to produce four core financial statements. Together, they give donors, boards, and auditors a complete picture of financial health and stewardship.

Statement of Financial Position

The nonprofit equivalent of a balance sheet, this statement reports assets, liabilities, and net assets as of a specific date. Critical requirement: Net assets must be split into two categories—with donor restrictions and without donor restrictions.

Statement of Activities

Alongside the financial position statement, this is often the first report stakeholders review. It shows revenues, expenses, and changes in net assets over a reporting period. Both revenues and net asset changes must be presented by restriction category—a key distinction from for-profit income statements.

Statement of Cash Flows

This statement classifies cash inflows and outflows as operating, investing, or financing activities. ASU 2016-14 added mandatory liquidity disclosures in two forms:

- Financial assets available to meet general expenditures within one year (quantitative)

- How the organization manages liquid resources and its liquidity policies (qualitative)

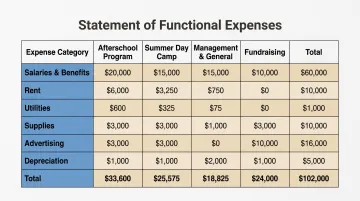

Statement of Functional Expenses

Required for voluntary health and welfare organizations, and FASB recommends it as best practice for all nonprofits. It presents natural and functional expense classifications in a matrix format—directly feeding Form 990 Part IX and giving auditors and boards clear visibility into how program, management, and fundraising costs break down.

Common GAAP Mistakes Nonprofits Make

Confusing Conditions with Restrictions

The error: Recording conditional contributions as revenue before conditions are met, or treating unconditional restricted contributions as conditional (delaying revenue recognition).

The fix: Carefully read grant agreements. Look for two specific signals: a barrier (a specific performance requirement) and a right of return (the funder can reclaim funds if you don't perform). If both exist, it's conditional — record as a refundable advance until you substantially meet the barrier. If funds are designated for a purpose without a right of return tied to performance, it's an unconditional restricted contribution — recognize immediately.

How it plays out in practice:

- A grant requiring you to "file a summary report" at year-end is a routine administrative stipulation — not a barrier. That grant is unconditional with a restriction; recognize revenue immediately.

- A grant requiring you to "demonstrate 20% improvement in client outcomes," with a right of return if you don't, contains a substantive barrier. Record it as a refundable advance until the condition is met.

Misreporting In-Kind Contributions

Two opposite errors show up here: recording everything donated as revenue, or missing contributions that should be recorded.

Under ASC 958-605-25-16, in-kind contributions qualify for recognition based on what was donated:

- Tangible goods and space: Record at fair market value as both revenue and expense when received

- Volunteer services — qualifying: Recognize when services create or enhance a nonfinancial asset (such as construction or repairs), or when they require specialized skills — accounting, legal, medical, trades — provided by individuals who hold those skills, and that your organization would otherwise pay for

- Volunteer services — non-qualifying: General volunteer time, including event support and board meeting attendance, does not meet the recognition threshold

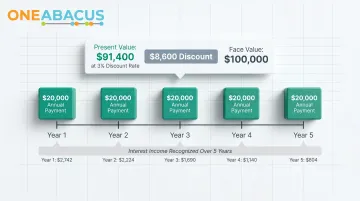

Multi-Year Pledge Recording Errors

The error: Recording multi-year pledges on a cash-received basis, or failing to discount unconditional pledges to present value.

The fix: Under ASC 958-310-25-1, unconditional promises to give are recognized immediately as receivables and contribution revenue in the period the promise is received. Multi-year unconditional pledges must be measured at the present value of estimated future cash flows using a risk-adjusted discount rate.

Example: A donor pledges $100,000 payable over five years ($20,000 annually). If your discount rate is 3%, the present value is approximately $91,400. Record $91,400 as revenue immediately (not $20,000 per year), and the discount unwinds over time as interest income.

Conditional pledges are different: recognize only when conditions are substantially met, regardless of payment timing.

Frequently Asked Questions

Does GAAP apply to nonprofits?

Yes. FASB's Accounting Standards Codification (ASC) covers both for-profit and nonprofit organizations, with nonprofit-specific guidance under ASC 958. While not always legally mandated, GAAP compliance is expected by most funders, state regulators, and charity watchdogs for organizations above certain revenue thresholds.

What are the accounting standards for nonprofits?

Nonprofits follow U.S. GAAP as established by FASB, with sector-specific guidance primarily under ASC 958 (Not-for-Profit Entities). Key standards include ASC 606 (revenue from contracts), ASC 842 (leases), and IRS Form 990 requirements for functional expense reporting and net asset classification.

Does ASC 842 apply to nonprofits?

Yes. ASC 842 (lease accounting) became effective for nonprofits in fiscal years beginning after December 15, 2021. Nonprofits must recognize right-of-use assets and lease liabilities on their Statement of Financial Position for most leases, significantly affecting reported assets and liabilities for organizations with operating leases.

What financial statements do nonprofits use?

Nonprofits prepare four statements: Statement of Financial Position, Statement of Activities (showing changes in net assets by restriction category), Statement of Cash Flows, and Statement of Functional Expenses (required for voluntary health and welfare organizations; recommended for all others). Each differs from its for-profit equivalent in presentation and required disclosures.

What are the 5 principles of GAAP?

GAAP actually comprises 10 recognized principles, not five. The most commonly referenced include Consistency (same methods applied across periods), Materiality (complete disclosure of significant information), Prudence (fact-based reporting), Periodicity (standard reporting periods), and Sincerity (unbiased representation). All 10 principles work together to ensure accurate, transparent financial reporting.

What is the 33% rule for nonprofits?

The 33% rule refers to the IRS public support test under IRC Section 509(a)(1). To maintain 501(c)(3) public charity status, an organization must receive at least one-third of its total support from public sources—donations, grants, and government funding. This is a tax compliance standard reported on Form 990 Schedule A, not a GAAP requirement.

Understanding GAAP doesn't have to be overwhelming. Whether you're preparing for your first audit, transitioning to accrual accounting, or strengthening financial reporting for major grants, the right guidance matters. One Abacus Advisory specializes in helping nonprofits build GAAP-compliant systems, optimize accounting platforms like NetSuite, and prepare board-ready financial statements that meet funder requirements—all without the cost of a full-time CFO. Schedule a free consultation to discuss your organization's financial reporting needs.