Introduction

Nonprofit financial reporting operates under distinct accounting rules that differ from for-profit entities, with FASB ASC 958 serving as the governing standard. For executive directors, board members, and finance staff, understanding ASC 958 is a baseline requirement for maintaining compliance, building donor trust, and avoiding costly audit findings.

Recent surveys show that documentation deficiencies appear in more than 50% of reviewed nonprofit audits, with disclosure gaps among the most common findings. These failures stem from unclear guidance on net asset classification, contribution recognition timing, and enhanced disclosure requirements introduced through recent updates.

This guide covers the key areas auditors scrutinize most closely:

- The four required financial statements under ASC 958

- The two-class net asset framework

- How to distinguish conditional from restricted contributions

- Expense reporting requirements

- Critical disclosure obligations auditors review most closely

Key Takeaways

- ASC 958 sets the GAAP rules every U.S. nonprofit must follow for financial reporting

- Four statements are required: Financial Position, Activities, Functional Expenses, and Cash Flows

- Net assets now use a two-class model — with and without donor restrictions — replacing the old three-class system

- Conditional contributions must meet specific barrier criteria before they can be recognized as revenue

- Required disclosures include liquidity, board designations, expense allocation methods, and gifts-in-kind

What Is FASB ASC 958 and Why It Matters for Nonprofits

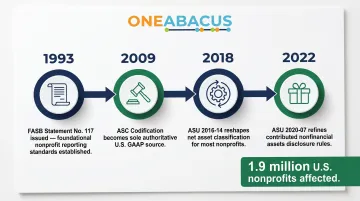

FASB ASC 958 is the Financial Accounting Standards Board's Accounting Standards Codification topic governing financial reporting for not-for-profit entities. When the Codification became authoritative on July 1, 2009, it consolidated and replaced all prior standards—including the widely cited FASB Statement No. 117 (SFAS 117) issued in June 1993.

Two significant updates reshaped nonprofit reporting:

ASU 2016-14 (effective for fiscal years beginning after December 15, 2017) restructured net asset classification from three classes to two, enhanced disclosure requirements, and required all nonprofits (not just voluntary health and welfare organizations) to prepare a Statement of Functional Expenses.

ASU 2020-07 (effective for fiscal years beginning after June 15, 2021) added specific disclosure requirements for contributed nonfinancial assets like donated goods, services, and space.

Both updates responded to stakeholder feedback about inconsistency and lack of transparency across the nonprofit sector.

The scale of impact is significant: approximately 1.9 million registered nonprofit organizations operate in the U.S., employing 12.8 million people and representing 9.9% of all private-sector employment. ASC 958 touches a substantial portion of the broader economy.

Who Must Follow ASC 958?

ASC 958 applies to all U.S.-based not-for-profit organizations operating under GAAP, including:

- Public charities and private foundations

- Educational institutions and healthcare nonprofits

- Religious organizations and cultural institutions

- Trade associations and professional societies

- Any tax-exempt entity that does not distribute profits to owners

The Four Financial Statements Required Under ASC 958

ASC 958 mandates four specific financial statements for nonprofits. Each one serves a distinct purpose — and together, they give donors, grantors, creditors, and oversight bodies what they need to assess your organization's financial health and stewardship.

Statement of Financial Position

Think of the Statement of Financial Position as the nonprofit equivalent of a balance sheet. It reports total assets, total liabilities, and total net assets as of a specific date.

Critical requirement: Net assets must be presented in two separate classes—with donor restrictions and without donor restrictions—rather than a single combined figure. This classification immediately communicates to readers how much of the organization's resources are available for discretionary use versus restricted by donor stipulations.

Statement of Activities

The Statement of Activities works like an income statement — it reports revenues, expenses, gains, losses, and other changes in net assets across both net asset classes for the reporting period.

Prior to ASU 2016-14, this statement tracked three net asset classes (unrestricted, temporarily restricted, permanently restricted). The updated format consolidates these into two classes and must show the total change in net assets for the period, giving leadership and stakeholders a direct read on whether the organization grew or drew down resources during the year.

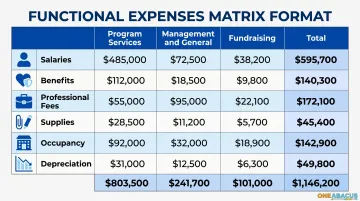

Statement of Functional Expenses

ASU 2016-14 expanded the requirement for the Statement of Functional Expenses from voluntary health and welfare organizations only to all nonprofit organizations. This statement presents expenses in a matrix format by both:

- Natural classification — salaries, rent, supplies, depreciation (what was purchased)

- Functional classification — program services, management and general, fundraising (why it was purchased)

This dual presentation reveals how resources are allocated between mission delivery and supporting activities—information critical to donors evaluating organizational efficiency.

Statement of Cash Flows

The Statement of Cash Flows reports cash inflows and outflows across operating, investing, and financing activities. Nonprofits may use either the direct or indirect method.

Important change: Under ASC 958, if your organization uses the direct method, the supplemental reconciliation schedule (indirect method) is no longer required. This reduces preparation time without sacrificing the underlying information stakeholders need.

Net Asset Classification: The Two-Class Framework

ASU 2016-14 reduced net asset classes from three to two. This change improved comparability across organizations and eliminated the long-standing confusion between "temporarily restricted" and "permanently restricted" designations.

Net Assets Without Donor Restrictions

Net assets without donor restrictions encompass funds available for use at the board's or management's discretion for any organizational purpose. This class replaced what was formerly called "unrestricted" net assets.

When a governing board sets aside funds for a specific purpose — such as a capital reserve or future program expansion — those funds remain classified as "without donor restrictions" but require separate disclosure in the notes. Two key differences distinguish board designations from donor-restricted funds:

- Reversibility: The board can reverse its designation at any time

- Authority: Donor restrictions cannot be unilaterally removed by the organization

Net Assets With Donor Restrictions

Net assets with donor restrictions include funds subject to donor-imposed stipulations limiting how or when they can be used. Two sub-types exist:

- Purpose restrictions: Contributions tied to a specific program or activity — for example, "$50,000 designated exclusively for youth programming"

- Time restrictions: Contributions unavailable until a future date or triggering event, including permanent endowments where only investment earnings may be spent

Underwater Endowment Funds

A particular risk within donor-restricted net assets involves endowment funds. When a fund's fair value falls below its original gift amount, it is considered "underwater." NACUBO survey data from 2020 found that approximately 20% of endowment funds were underwater during the COVID-19 market downturn.

ASC 958 requires specific disclosures for underwater endowments:

- The organization's policy and any actions taken concerning appropriation from underwater funds

- The aggregate fair value of such funds

- The aggregate original gift amounts required to be maintained

- The aggregate amount of the deficiency

Smaller nonprofits without dedicated finance staff are most likely to miss these disclosures — making this a priority review item during audit preparation.

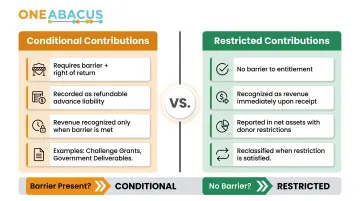

Recognizing Contributions: Conditional vs. Restricted Donations

The distinction between conditional and restricted contributions determines when a nonprofit may legally recognize a gift as revenue on the Statement of Activities. Misclassifying contributions leads to inaccurate financial reporting, audit findings, and potential restatements.

Conditional Contributions

ASU 2018-08 clarified that a contribution is conditional when the donor imposes both:

- A barrier the nonprofit must overcome to be entitled to the funds

- A right of return or right of release from obligation

Barrier indicators include:

- Measurable performance requirements (specific outputs, outcomes, or service levels)

- Stipulations that significantly limit discretion on conducting an activity

- Requirements related to the purpose of the agreement (not just administrative tasks)

Accounting treatment: Conditional contributions received in advance must be recorded as a refundable advance (liability), not as revenue. Revenue is recognized only when the barrier is substantially met or explicitly waived.

Common examples:

- A $500,000 challenge grant requiring the nonprofit to raise matching funds from other sources

- A government grant contingent on completing specific program deliverables and submitting performance reports

- A foundation award requiring IRB approval before research activities can begin

Recording a conditional gift as revenue before the barrier is met inflates reported revenue, risks donor agreement violations, and can trigger audit findings.

Restricted Contributions

Unlike conditional contributions, restricted contributions involve donor-imposed stipulations on use or timing but carry no barrier to entitlement — the nonprofit has already earned the gift.

Accounting treatment: Restricted contributions are recognized as revenue immediately upon receipt in the "net assets with donor restrictions" class. When the restriction is met, the amount is reclassified to "net assets without donor restrictions."

Key distinctions at recognition:

- Recorded immediately as revenue (not held as a liability)

- Reported under "net assets with donor restrictions"

- Reclassified to unrestricted net assets once the purpose or time condition is satisfied

Placed-in-Service Approach

When a restricted gift is used to acquire or construct a long-lived asset, the restriction is released when the asset is placed in service. ASU 2016-14 eliminated the prior option to release the restriction over the asset's useful life, simplifying reporting and improving consistency.

Expense Reporting: Functional and Natural Classifications

All nonprofits subject to ASC 958 must present expenses in two dimensions simultaneously, typically in a matrix format within the Statement of Functional Expenses.

Natural classification (what was purchased):

- Salaries and wages

- Employee benefits

- Professional fees and contract services

- Supplies and materials

- Occupancy costs (rent, utilities)

- Depreciation and amortization

- Interest expense

Functional classification (why it was purchased):

- Program services: Broken out by individual program (e.g., youth services, community outreach, research initiatives)

- Management and general: Oversight, business management, recordkeeping, budgeting

- Fundraising: Soliciting contributions, grant writing, donor cultivation

Cost Allocation Requirements

Cost allocation methods must be disclosed in the notes to the financial statements. Allocation of shared costs—such as an executive director who spends time on programs, administration, and fundraising—must be based on reasonable, rational, and consistently applied methodology.

Acceptable methods include:

- Tracking how personnel actually spend their time across functions (time studies)

- Allocating costs proportionally based on the number of staff engaged in each function

- Distributing occupancy costs by physical space used for each function

- Assigning costs directly to whichever function generated or benefited from them

Choosing the right method is only half the challenge — applying it consistently across reporting periods and documenting it clearly for auditors is where many organizations fall short. Nonprofits without dedicated finance staff often struggle to build and maintain these systems on their own.

That's where fractional CFO support makes a concrete difference. One Abacus Advisory works with nonprofits to design allocation frameworks that hold up under auditor scrutiny and accurately reflect how resources support mission delivery.

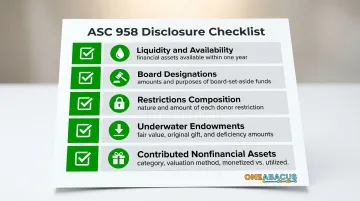

Enhanced Disclosure Requirements Under ASC 958

Liquidity and Availability Disclosure

ASC 958 requires nonprofits to disclose:

Quantitative information: A schedule of financial assets available within one year of the balance sheet date to meet cash needs for general expenditures

Qualitative information: How the organization manages liquid resources and ensures sufficient liquidity to meet obligations

This disclosure targets a practical stakeholder concern: whether the nonprofit can meet near-term financial obligations. Organizations with significant net assets but limited liquidity must explain how they plan to fund operations — especially when most assets are restricted or board-designated.

Contributed Nonfinancial Assets

ASU 2020-07 requires nonprofits receiving gifts-in-kind to:

- Present contributed nonfinancial assets as a separate line item in the Statement of Activities

- Disaggregate by category (food, supplies, equipment, services, use of facilities)

- Disclose whether assets were monetized (sold) or utilized (used in programs)

- Describe any donor-imposed restrictions

- Explain the valuation techniques used to arrive at fair value

This enhanced transparency responds to long-standing concerns about inconsistent valuation practices. Beyond gifts-in-kind, ASC 958 imposes several additional disclosure requirements that affect most nonprofits.

Other Key Disclosures

- Board designations — specific amounts and purposes of any governing board designations of net assets without donor restrictions

- Composition of restrictions — nature and amount of each donor restriction type, including time, purpose, and perpetual restrictions

- Underwater endowments — fair value, original gift amounts, and deficiency for all underwater endowment funds

- Cost allocation methods — how shared costs are distributed among program and support functions

- Collections policies — for museums and cultural institutions, whether collections are capitalized or expensed

Missing or incomplete disclosures are among the most common findings in nonprofit audits. A systematic disclosure checklist — reviewed annually before audit fieldwork begins — is the most reliable way to catch gaps before auditors do.

Frequently Asked Questions

What is FASB ASC 958?

FASB ASC 958 is the section of the FASB Accounting Standards Codification that establishes GAAP financial reporting requirements specifically for not-for-profit entities. It covers financial statement presentation, revenue recognition for contributions, expense reporting by function and nature, and required disclosures.

What financial statements are required for a nonprofit?

Nonprofits must prepare four statements under ASC 958: the Statement of Financial Position, Statement of Activities, Statement of Functional Expenses, and Statement of Cash Flows, plus accompanying notes to the financial statements.

Do non-profits need to follow GAAP?

Yes — nonprofits must follow GAAP (specifically ASC 958) if they undergo an independent audit or review, receive federal funding subject to Uniform Guidance (single audit threshold rises to $1,000,000 for fiscal years ending after September 30, 2025), or are required to do so by lenders, grantors, or state law.

How does the FASB require not-for-profit organizations to report expenses?

ASC 958 requires nonprofits to report expenses by both functional classification (program services, management and general, fundraising) and natural classification (salaries, occupancy, depreciation, etc.), presented together in a Statement of Functional Expenses matrix format.

What is FASB 117?

FASB Statement No. 117 was the original 1993 standard for nonprofit financial statements, introducing a three-class net asset model (unrestricted, temporarily restricted, permanently restricted). It was superseded by ASC 958 and then significantly updated by ASU 2016-14, which consolidated those three classes into two.

Does ASC 606 apply to nonprofits?

ASC 606 applies to nonprofits for exchange transactions where the nonprofit provides goods or services of roughly equal value in return for payment (such as tuition, membership dues with reciprocal benefits, and ticket sales). However, contributions and grants without commensurate exchange are governed by ASC 958-605, not ASC 606.