This article walks through the preparation required before budgeting begins, a step-by-step process for translating strategic priorities into a funded budget, the key variables that determine whether a strategic budget holds or unravels, and the most common mistakes that undermine even well-intended plans.

Key Takeaways

- Strategic budgets require costing out specific new initiatives, not just projecting routine operations with a percentage increase

- Strong preparation depends on current financial data, restricted fund clarity, and early involvement from finance and development teams

- Full-cost allocation, including overhead and capacity investments, must be embedded in initiative budgets to prevent structural deficits

- Scenario planning and strategic reserves belong in the initial budget, not added as an afterthought

What You Need Before Building Your Strategic Plan Budget

The quality of a strategic budget depends entirely on the quality of its inputs. Without solid financial groundwork, even a well-structured budget process produces unreliable results that undermine decision-making and board confidence.

Financial Data and Baseline Documents

Start by assembling the documents that define your current financial reality:

- 2-3 years of audited financials or reviewed statements to establish trends in revenue, expenses, and net asset changes

- Current year-to-date actuals versus budget to identify variances and seasonal patterns

- Cash flow history to understand timing gaps between revenue and expenses

- **Breakdown of restricted versus unrestricted fund balances** to clarify which funds can be redeployed for strategic purposes

The restricted fund breakdown matters more than most organizations anticipate. FASB ASU 2016-14 requires nonprofits to classify net assets into "with donor restrictions" and "without donor restrictions" — and this classification directly constrains which funds can support new strategic initiatives.

Many organizations discover mid-process that the dollars they planned to use are already committed to specific grant conditions. TheCharityCFO recommends having at least 50% of total revenue from unrestricted sources as a baseline marker of financial flexibility.

The Right People at the Table

Strategic budgets require input from multiple perspectives. The core team should include:

- Executive director — sets overall priorities and ensures alignment with mission

- **Finance lead or CFO** — structures the budget framework and ensures technical accuracy

- Development director — provides realistic revenue projections based on donor pipeline and grant probability

- Key program leads — cost out the resources required to execute each strategic priority

Many nonprofits lack dedicated in-house financial leadership capable of structuring a strategic-level budget. A fractional CFO engagement fills that gap — One Abacus Advisory, for example, works with nonprofits to build scenario models, validate revenue projections, and stress-test assumptions before the plan is finalized. For organizations navigating growth or leadership transitions, this approach provides executive-level financial input without the overhead of a full-time hire.

How to Budget for Your Nonprofit's Strategic Plan

Step 1: Anchor the Budget to Your Strategic Priorities

Map your strategic plan's 3-5 priorities directly onto a budget framework. Each priority should become a distinct cost category or program area — so spending tracks against strategic intent, not just functional departments.

Distinguish clearly between:

- Continuation costs — what it costs to maintain current operations at existing levels

- Strategic investment costs — the new or incremental spending required to advance each priority

This distinction makes visible what the organization is already committed to funding versus what the strategic plan actually demands. The National Council of Nonprofits recommends that strategic planning identify measurable goals and approved priorities, with a clear theory of change defining what success looks like and what resources are needed.

Step 2: Cost Out Each Strategic Initiative

Once priorities are mapped, cost out each initiative line by line:

- Personnel time (including leadership hours)

- Contracted services and consulting fees

- Technology and software

- Facilities and occupancy

- Travel and communications

- Capital needs (equipment, vehicles, infrastructure)

Vague initiative descriptions produce vague cost estimates, which are reliably insufficient. Each initiative needs a detailed breakdown that program leads can defend and finance staff can track.

Full-cost allocation is critical. Shared overhead costs — HR, IT, financial management, occupancy — should be proportionally assigned to strategic initiatives, not treated as a separate pool that floats outside the plan. Propel Nonprofits' "True Program Costs" template guides nonprofits through this process, enabling organizations to understand the true, full cost of delivering programs and identify which are self-sustaining versus which require subsidy.

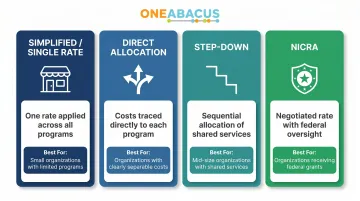

Four primary allocation methods exist:

| Method | Best For |

|---|---|

| Simplified (single rate) | Small organizations with limited programs |

| Direct allocation | Organizations with clearly separable costs |

| Step-down | Mid-size organizations with shared services |

| Negotiated Indirect Cost Rate Agreement (NICRA) | Organizations receiving federal grants |

The "overhead myth" — the pressure to minimize administrative and fundraising costs — has pushed nonprofits into systematic underinvestment in infrastructure. The Urban Institute's study of over 220,000 Form 990s found that 25% of nonprofits reported $0 in fundraising expenses and 13% reported $0 in management and general expenses — both operationally impossible figures indicating systemic underreporting.

Strategic budgets must fund the capacity needed to execute the plan. Underreporting overhead doesn't reduce costs; it just makes them invisible until they become a crisis.

Step 3: Build Revenue Projections Around What the Plan Requires

Strategic budgets must project revenue through the lens of what the plan demands, not simply what was raised last year. This requires asking:

- Are current revenue sources sufficient to fund the plan?

- If not, what new funding strategies are needed — new grants, earned income, campaigns, major gifts?

Classify revenue by reliability using a probability-based framework:

| Probability Tier | Classification | Budget Treatment |

|---|---|---|

| 90-100% | Secured funding | Include in base budget |

| 50-89% | Likely funding | Include with monitoring |

| 25-49% | Possible funding | Include in optimistic scenario only |

| Below 25% | Speculative funding | Exclude from operating budget |

The Nonprofit Finance Fund recommends separating "core" budget from "aspirational" thinking and tracking the probability of receipt for each funding source. This discipline prevents overestimating revenue and creating a structural shortfall before the plan even begins.

Step 4: Incorporate Strategic Reserves and Contingency

Most guidance on nonprofit reserves focuses on operating reserves — funds for day-to-day liquidity — but strategic plans need a separate strategic reserve to absorb cost overruns, delayed revenue, or pivot needs within the plan itself.

Propel Nonprofits identifies four reserve categories:

- Operating reserves — unrestricted fund balance for unexpected events

- Building repair and replacement reserves

- Program reserves — for program continuation if income is uncertain

- Opportunity reserves — seed funding for new ideas

A commonly used reserve goal is three to six months' expenses, though the right amount depends on the plan's risk profile. Expansion into new geographies or services carries more risk than deepening existing programs, and reserves should reflect that exposure.

The reality is sobering: 52% of nonprofits have fewer than three months of cash reserves, and 18% have one month or less. Strategic budgets should include an explicit reserve contribution line item — treated as a non-negotiable expense, not an afterthought. At minimum, reserves should cover one full payroll including taxes; at the ceiling, they should not exceed two years' budget.

Step 5: Stress-Test the Budget with Scenario Planning

Scenario planning means building at least two alternative versions of the budget:

- Conservative scenario — assumes a major grant does not renew or revenue falls below target

- Optimistic scenario — assumes new funding sources materialize and existing sources grow

This exercise forces leadership to identify which strategic initiatives are truly mission-critical versus which are contingent on funding coming through. The Nonprofit Finance Fund offers a free scenario planning tool that models up to two scenarios beyond the baseline budget.

Use scenarios to set decision rules in advance:

- If revenue lands below a certain threshold, which initiatives pause?

- Which scale back?

- Which proceed regardless?

Making these calls before a shortfall occurs — rather than in the middle of one — keeps leadership focused on mission execution instead of crisis management.

Step 6: Gain Board Approval and Establish a Monitoring Cadence

A strategic budget must be formally approved by the board, not simply shared as an informational document. That approval signals board accountability for both the plan and its financial sustainability. Financial oversight is one of the fundamental, legal responsibilities of a nonprofit board, and the budget is the mechanism through which that responsibility is exercised.

Establish a monitoring cadence that includes:

- Quarterly budget-to-actual reviews tied explicitly to strategic plan milestones, not just departmental spending

- Defined escalation process for how variances are identified, communicated, and addressed

- Annual formal approval recorded in board meeting minutes

This cadence ensures the strategic budget remains a living management tool rather than a document that gets shelved after approval.

Key Variables That Shape Your Strategic Budget Outcomes

A strategic budget can be well-constructed on paper and still fall apart in practice. These are the variables most likely to determine whether your plan holds — or quietly unravels.

Revenue Concentration Risk

If a significant portion of the budget supporting key strategic initiatives depends on one or two funding sources, the entire plan is exposed to that funder's decisions. Crowded's analysis of Form 990 data flags risk when 80% of funding comes from 20% or fewer sources, noting that losing just one funder can put the organization at serious risk.

The current environment intensifies this concern. The Nonprofit Finance Fund's 2025 survey found that 84% of nonprofits with government funding expect cuts to that funding. Any nonprofit with high government reliance must model grant non-renewal scenarios explicitly and build diversification strategies into the strategic plan itself.

Overhead Allocation Method

The method used to allocate shared costs affects how accurately each strategic initiative reflects its true cost. An inaccurate allocation can make some initiatives appear affordable when they are not, creating a structural deficit that surfaces only after the initiative is underway.

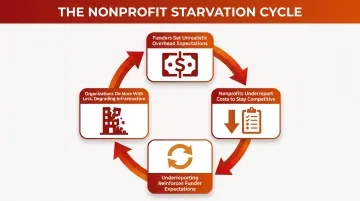

Underallocated overhead is one of the primary drivers of the "starvation cycle" — a term coined by Ann Goggins Gregory and Don Howard in their 2009 Stanford Social Innovation Review article. The cycle reinforces itself in four steps:

- Funders set unrealistic overhead expectations

- Nonprofits underreport costs to remain competitive

- Underreporting reinforces those funder expectations

- Organizations "do more with less," degrading infrastructure

This dynamic forces nonprofits to underfund the very systems — financial management, HR, communications — that strategic plans depend on.

Multi-Year vs. Single-Year Horizon

Most strategic plans span 3-5 years, but many nonprofits budget only one year at a time. This mismatch means year two and three costs — hiring, infrastructure, program expansion — are often invisible until they become urgent.

A. Michael Gellman explains that multi-year grants recorded fully in Year 1 under GAAP create an artificial "surplus" followed by years of apparent "deficit," misleading boards about financial health. He recommends creating a Usage Authorization Period (UAP) schedule showing planned annual usage and adding non-GAAP budget lines to smooth the distortion.

Building a high-level multi-year financial model alongside the annual budget allows leadership to spot future funding gaps, hiring ramp-ups, and capital needs before they become crises — rather than reacting to them mid-plan.

Timing and Cash Flow Alignment

Strategic investments often require upfront spending — hiring, contracting, launching new programs — while the revenue to fund them arrives later. Reimbursement-based grants create 30-, 60-, or 90-day cash gaps between spending and receiving funds.

Cash flow timing mismatches are a common but underappreciated cause of strategic plan stalls. Tools to bridge these gaps include:

- Lines of credit to even out timing bumps

- Bridge loans when a specific repayment source is identified but not yet received

- Phased hiring to align salary costs with revenue arrival

Propel Nonprofits warns that borrowing to cover a persistent deficit is inappropriate — loans should address timing gaps, not structural shortfalls.

Common Budgeting Mistakes That Undermine Strategic Plans

Budgeting for the Status Quo Instead of the Strategy

Many organizations build their strategic plan budget by taking last year's budget and adding a percentage increase. This approach fails to capture the incremental investment that strategic priorities actually require.

Zero-based budgeting eliminates the automatic assumption of growth, forcing each line item to be justified from scratch. While time-intensive, this method reveals the true cost difference between maintaining current operations and advancing strategic goals.

Ignoring Full Costs and Underfunding Overhead

Excluding or minimizing shared operational costs — finance, HR, communications — from strategic initiative budgets creates a structural deficit. Warren Averett notes that the "overhead myth" wrongly suggests organizations shouldn't spend on administrative expenses, when in fact such spending is essential for sustainability.

Strategic budgets should explicitly fund infrastructure as strategic initiatives, not hidden overhead. When boards and funders see overhead tied directly to outcomes — faster reporting, stronger compliance, reduced staff turnover — capacity investment becomes a harder case to dismiss.

Treating the Strategic Plan Budget as a One-Time Exercise

A budget built once at the start of the planning cycle and never revisited quickly becomes a fiction. Quarterly budget-to-actuals aligned with strategic milestones are essential, not optional. These reviews enable leadership to identify early warning signs — revenue shortfalls, cost overruns, timeline delays — and adjust before problems compound.

Failing to Involve the Development Team in Revenue Projections

When finance builds revenue assumptions without input from the team responsible for raising the money, projections are frequently optimistic and disconnected from realistic pipeline assessments.

A collaborative process fixes this. Development staff should weigh in on:

- Donor capacity and relationship stage

- Grant likelihood and funder timelines

- Constraints that affect when revenue will actually arrive

Those assessments can then be bucketed into probability tiers — confirmed, likely, and speculative — so the final revenue figure reflects realistic timing, not wishful thinking.

When to Revisit Your Strategic Plan Budget

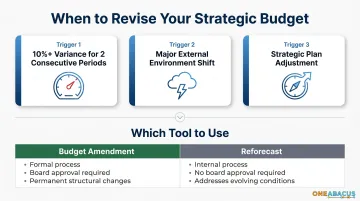

Budgeting for a strategic plan is not a one-time event at the start of the planning cycle — it requires planned, structured reassessment at specific trigger points throughout the plan's life.

Three primary triggers warrant a formal budget revision:

- Significant variance in results: JFW Accounting Services recommends organizations establish clear variance thresholds and trigger a reforecast when revenue or expenses deviate 10% or more from budget for two consecutive reporting periods. Labor changes should be an automatic trigger since personnel is typically the largest expense category.

- Major shift in the external environment: Loss of a key funder, regulatory change, unexpected community need, or economic conditions affecting donor capacity all require revisiting which initiatives remain viable.

- Leadership decision to adjust the strategic plan: Adding, pausing, or reprioritizing initiatives mid-cycle requires a corresponding budget adjustment to keep strategy and resources aligned.

It's also worth knowing which tool to use when changes arise:

- A budget amendment is a formal adjustment to the approved budget mid-cycle, requiring board notification or approval. Use this when changes are material and permanent.

- A reforecast is an internal management tool that updates projections without altering the official approved budget. Use this when conditions are still evolving.

Frequently Asked Questions

How much does strategic planning cost for a nonprofit organization?

Costs vary widely based on whether the nonprofit uses internal staff time, engages a consultant, or both. Direct facilitation and consulting fees typically range from $5,000 to $20,000, with complex projects reaching $50,000–$100,000+. Average consultant rates are approximately $159 per hour, though staff time — often the largest hidden cost — should also be budgeted.

What budget allocation rules should nonprofits consider when creating a strategic plan?

No single allocation rule fits all nonprofits. Frameworks like 70/20/10 (core operations/growth initiatives/innovation) offer a useful starting point, but the right split depends on your organization's financial health, risk tolerance, and plan priorities.

Should a nonprofit's strategic plan budget be separate from its annual operating budget?

They should be integrated. Reflect the strategic plan's financial requirements within the annual operating budget as distinct cost categories or initiative lines — not as a parallel document. This ensures real-time tracking and board accountability.

Who should lead the budgeting process for a nonprofit strategic plan?

The executive director and finance lead (CFO, controller, or fractional CFO) should co-lead the process, with input from the development director and program leads. Board finance committee review and full board approval are required before finalizing.

How do you budget for a multi-year nonprofit strategic plan?

Build a high-level multi-year financial model covering the full plan period alongside your first annual budget. This surfaces future funding gaps, hiring ramp-ups, and capital needs before they become crises — even as detailed annual budgets are built one year at a time.

What should a nonprofit do if its strategic plan budget has a shortfall?

A shortfall should trigger a structured review of which initiatives are fully funded, which are contingent on new funding, and which should be deferred. Scenario plans built during budgeting make this a manageable decision — leadership can execute pre-defined rules rather than react under pressure.