Introduction

Year-end hits nonprofit finance teams from every direction at once: reconciling accounts, closing the books, drafting Form 990, preparing for external auditors, and delivering a clear financial story to the board — all under the same deadline pressure.

The core tension is that most year-end board reports land in one of two failure modes: too dense with accounting detail to be useful, or too thin on context to be meaningful. According to IRS governance guidance, nonprofit boards must "regularly receive and review up-to-date financial statements" — yet most board members don't have accounting backgrounds.

When finance teams deliver raw trial balances or jargon-heavy summaries without interpretation, boards can't fulfill their fiduciary duties with confidence.

This article covers what boards actually need from year-end reports, how to simplify the process step by step, what drives report quality, and the most common mistakes to avoid.

Key Takeaways

- Start year-end close preparation 60–90 days out to avoid a last-minute sprint

- Board reports should connect financials to mission: health, restricted fund status, budget-to-actual, and forward outlook

- Every board report needs four statements: Financial Position, Activities, Functional Expenses, and Cash Flow

- Common failures: no narrative context, buried variances, and unreconciled restricted funds

- Organizations without dedicated finance staff benefit most from fractional CFO support for structured, board-ready year-end reports

What Nonprofit Boards Actually Need from Year-End Reports

The Governance Mindset Shift

Nonprofit board members are governance-focused stewards, not accountants. BoardSource defines three core fiduciary duties: care, loyalty, and obedience. Board members need to make decisions about mission, strategy, and risk — not audit a trial balance. When you deliver year-end financial reports, frame them through the lens of governance oversight rather than accounting compliance.

This distinction matters because board composition varies widely. While some boards include finance professionals, many consist primarily of community leaders, attorneys, program experts, and mission advocates.

According to BoardSource's Leading with Intent 2023 study, boards perform strongest in mission and fiduciary oversight but weakest in fundraising and strategy. Your year-end report must bridge this gap by translating financial data into strategic insight.

Four Essential Components of a Board-Ready Report

Every effective year-end board report includes:

- Overall financial health and liquidity snapshot — cash on hand, months of operating reserves, financial position trends

- Clarity on restricted versus unrestricted funds — what resources are available for operations versus donor-designated purposes

- Program-level financial performance tied to outcomes — how efficiently programs used resources and what impact resulted

- Forward-looking section on the year ahead — budget framing, known funding risks, strategic decisions requiring board input

The Narrative Layer Is Not Optional

Financial data without context misleads as often as it informs. A budget variance with no explanation forces board members to speculate — and a revenue decline without background on grant timing creates unnecessary alarm. The narrative layer turns raw numbers into decisions boards can act on.

Consider a 40% year-over-year increase in restricted net assets. That could reflect new multi-year grant awards — a positive sign that still requires compliance monitoring. Or it could mean unspent current-year funds, which may point to program delivery issues. The same number signals either strength or risk depending on the context behind it.

What to Leave Out

More data does not equal more transparency. Exclude:

- Excessive line-item detail (summarize; detailed schedules belong in appendices)

- Accounting adjustments without business context (why the entry was made)

- Technical footnotes that belong in the audit file rather than the board packet

When in doubt, ask whether each item helps the board make a decision or take an action. If not, it belongs in a supplemental file — not the main report.

How to Simplify End-of-Year Reporting for Nonprofit Boards

Step 1: Build a Year-End Close Calendar

Work backwards from hard external deadlines:

Start with your board meeting date, Form 990 due date (15th day of the 5th month after fiscal year-end), audit or financial review window, and any grant reporting deadlines. Internal close milestones must sit well ahead of these dates.

According to practitioner consensus referenced by CPA firms such as Pinion, nonprofits that handle year-end best start 60 to 90 days early. This timeline allows for reconciliation, variance investigation, and drafting a clear board narrative — rather than rushing everything at the last minute.

Assign named owners to each deliverable:

Assign a named staff member to each deliverable so accountability is clear before the rush begins:

- Bank reconciliations

- Accounts receivable aging review

- Restricted fund schedule updates

- Draft financial statements

- Narrative preparation

- Board packet assembly

When each person knows their deadline, nothing slips through the cracks.

Step 2: Reconcile and Organize Financial Records

Proactively reconcile key accounts:

In the weeks leading up to year-end, reconcile:

- Bank accounts (all operating, savings, investment accounts)

- Accounts receivable (review aging, write off uncollectible amounts)

- Accounts payable (clear stale items, confirm accruals)

- Payroll liabilities (ensure payroll tax filings match ledger)

- Restricted net assets (tie to underlying agreements)

- Fixed assets (verify existence, update depreciation)

- Lease obligations (confirm compliance with ASC 842 if applicable)

Resolving stale checks, old payables, and outstanding receivables early reduces close complexity and cuts down on last-minute surprises.

Document every journal entry clearly:

Ensure every journal entry includes a clear business purpose and accessible supporting backup. Well-documented records do more than satisfy auditors — they make explaining variances to board members faster and more credible.

If you need to reconstruct why an entry was made six weeks later, your close will slow down and errors will creep in.

Reconcile restricted fund balances:

Review and confirm that restricted fund balances are current and match underlying grant agreements or donor documentation. Research shows that failing to properly track and honor donor restrictions is one of the most common and serious audit findings. Unreconciled restrictions create board confusion and audit friction.

Step 3: Assemble the Board-Ready Report Package

Build the core financial statement package:

Include these four documents:

- Statement of Financial Position (balance sheet) — assets, liabilities, net assets

- Statement of Activities (income/expense) — revenues, expenses, changes in net assets

- Statement of Functional Expenses (program vs. management vs. fundraising) — required for all nonprofits under FASB ASU 2016-14

- Cash Flow summary — operating, investing, and financing activities

Together, these four documents give the board a complete picture of financial health and stewardship.

Add a budget-to-actual comparison:

Include a full fiscal year budget-to-actual comparison with a brief written narrative explaining significant variances. While no authoritative standard defines materiality thresholds for nonprofit variance reporting, establish an organizational policy (e.g., variances exceeding 10% and $10,000) to guide which items require board-level explanation.

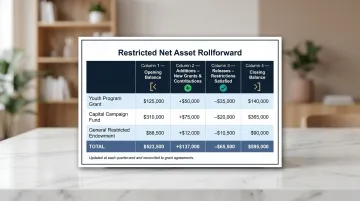

Include a restricted net asset rollforward table:

This is the single most useful tool for answering board questions about donor intent and compliance. The table should show:

- Opening balance by restriction purpose

- Additions (new grants, contributions received)

- Releases (restrictions satisfied)

- Closing balance by restriction purpose

Board members can immediately see what resources are available for strategic use versus committed to specific donor purposes — without needing to ask.

Step 4: Frame the Financial Story for Board Presentation

Open with a mission moment:

Before presenting the numbers, include a brief program highlight, a key outcome metric, or a quote from a beneficiary. Grounding the financial discussion in organizational purpose keeps board members engaged through detailed financial review — not just the summary slides.

For example:

"This year, our after-school program served 340 students, a 28% increase over last year. The financial report that follows shows how we funded this expansion while maintaining fiscal discipline."

Use simple charts and graphs:

Make financial health immediately readable with visuals:

- Revenue vs. expenses trend (3-year comparison)

- Budget vs. actual (current year)

- Liquidity trend (months of cash on hand)

- Fund balance composition (restricted vs. unrestricted)

Visuals reduce meeting time spent interpreting raw figures and help non-finance board members grasp key trends quickly.

Close with a forward-looking section:

Transition the report from a historical summary to a governance tool by including:

- Preliminary next-year budget framing

- Known funding risks (grant renewals, donor concentration)

- Reserve or operating fund status

- Strategic financial decisions the board needs to weigh in on

When boards leave the year-end meeting with clear decisions to make — not just data to absorb — the report has done its job.

Key Variables That Affect Year-End Board Report Quality

Board report quality ultimately depends on how well four underlying financial variables are managed throughout the year. These are the areas most likely to produce errors, audit findings, or board confusion if not addressed before the close.

Revenue Classification Accuracy

Misclassifying contributions vs. exchange transactions — or failing to distinguish conditional from unconditional grants — can cause material misstatements in the Statement of Activities and misrepresent available net assets to the board.

Two standards govern this area:

- ASC 958-605 — Exchange transactions involve commensurate value received by the resource provider (accounted for under ASC 606); contributions provide only indirect benefit (accounted for under ASC 958-605).

- FASB ASU 2018-08 — A contribution is conditional only if both a barrier exists and the donor retains a right of return. Conditional contributions are recognized as liabilities (refundable advances) until conditions are met.

Ensure each grant and major contribution is reviewed for proper classification before year-end. Document the accounting position in a brief policy memo so the rationale is clear to auditors and board members alike.

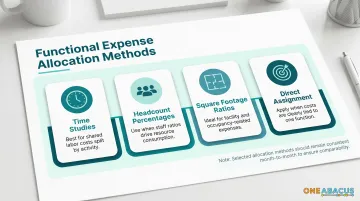

Functional Expense Allocation Methodology

Boards and major donors increasingly scrutinize the split between program, management, and fundraising costs. BBB Wise Giving Alliance Standard 8 requires charities to spend at least 65% of total expenses on program activities, while Standard 9 caps fundraising at no more than 35% of related contributions. Inconsistent or poorly documented allocation drivers undermine credibility.

Refresh allocation drivers before the close:

- Time studies (staff time allocation across functions)

- Headcount percentages

- Square footage ratios

- Direct assignment where possible

Ensure month-to-month consistency. Large year-end true-up entries raise questions from both auditors and board members about whether allocations reflect actual resource use.

Restricted Net Asset Tracking

Without a current, reconciled schedule of donor-restricted and board-designated funds, the board cannot accurately assess what portion of the organization's resources are available for operations or strategic use.

FASB ASU 2016-14 simplified net asset classifications to two categories: net assets with donor restrictions and net assets without donor restrictions. Board-designated funds are a subset of unrestricted net assets, reflecting internal decisions rather than external donor stipulations.

Maintain a rolling restricted net asset rollforward updated at least quarterly. At year-end, tie every restriction to its underlying grant agreement, pledge document, or board resolution. Organizations that track restrictions informally tend to discover discrepancies during the audit — not before it.

Documentation Completeness

Missing or vague documentation — for journal entries, revenue positions, or policy decisions — slows the close, increases audit risk, and forces finance staff to reconstruct rationale under deadline pressure.

Build documentation standards into the year so year-end review confirms what's already in order, not reconstructs it. Accounting systems like NetSuite — which One Abacus Advisory helps nonprofits configure and optimize — can automate much of this, including fund segmentation, period close checklists, and FASB-compliant reporting outputs.

Common Mistakes Nonprofits Make in Year-End Board Reporting

Starting Too Late

Compressing the year-end close into a two-to-three-week window forces rushed reconciliations, undocumented entries, and last-minute report assembly. According to practitioner guidance, preparation should begin 60 to 90 days before year-end. Early preparation allows time to investigate variances, resolve reconciliation issues, and draft thoughtful narratives rather than scrambling to meet deadlines.

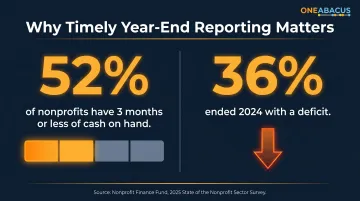

The Nonprofit Finance Fund 2025 survey found that 52% of nonprofits have three months or less of cash on hand, and 36% ended 2024 with a deficit. These thin margins raise the stakes of accurate, timely year-end reporting.

Producing Finance-Speak Reports

Delivering raw accounting outputs — unformatted trial balances, dense footnotes, or technical memos — to a board audience that includes lawyers, community leaders, and program experts leaves readers without the context they need to govern effectively. Every section of the board report should be written for a non-accountant reader.

Replace technical terms with plain language:

- "Net assets with donor restrictions" → "Funds designated by donors for specific purposes"

- "Liquidity and availability" → "Cash available to meet operational needs"

- "Functional expense allocation" → "How we divide costs across programs, management, and fundraising"

Skipping the Narrative

Board members can't govern what they can't interpret. A budget variance with no explanation leaves board members to speculate. A mission moment with no financial connection misses the governance purpose. That context is not optional.

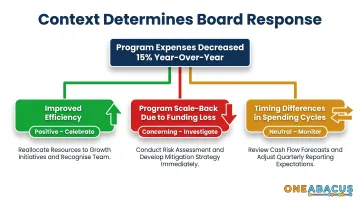

For example, if program expenses decreased 15% year-over-year, the board needs to know whether this reflects:

- Improved efficiency (positive)

- Program scale-back due to funding loss (concerning)

- Timing differences in spending cycles (neutral, requires monitoring)

Context determines whether the board should celebrate, investigate, or simply note the variance.

Neglecting Restricted Fund Reconciliation

Walking into a board meeting without a current, reconciled view of restricted net assets is one of the most common — and avoidable — sources of difficult board questions. Restrictions that aren't properly tracked and released can signal compliance failures to major donors and grantors.

To close this gap before year-end:

- Maintain a rolling restricted net asset schedule, updated at least quarterly

- Verify every restriction ties to its underlying grant agreement or donor letter

- Confirm that releases match actual expenditures for the designated purpose

Conclusion

Effective nonprofit year-end board reporting works best when preparation starts early, financial records are clean and well-documented, and the final report translates accounting data into a clear, mission-connected narrative the board can act on. When reporting falls short, it usually comes down to the same two problems: preparation that starts too late and financial data delivered without context. Fixing both puts boards in a position to govern — not just review numbers.

For nonprofits without dedicated senior finance staff, a fractional CFO provides the structured financial leadership needed to produce board-ready reports consistently — without the cost of a full-time hire. One Abacus Advisory offers exactly that kind of support, built specifically for mission-driven organizations.

Founder Lorin Port has partnered with organizations including the Philadelphia Zoo, San Diego Food Bank, and Laguna Playhouse through year-end close processes — optimizing financial systems, strengthening board reporting, and ensuring compliance during critical transitions.

Frequently Asked Questions

What is the end of year report for a nonprofit organization?

The year-end report is a formal package of financial statements, compliance documentation, and narrative that summarizes the organization's financial performance and stewardship of donor funds. It serves as the board's primary tool for fiduciary oversight.

What financial statements should be included in a nonprofit board report?

The four core statements are: Statement of Financial Position, Statement of Activities, Statement of Functional Expenses, and Cash Flow. A budget-to-actual comparison and restricted net asset rollforward are equally important additions for complete board governance.

How might a nonprofit ensure transparency in the reporting process?

Adopt a consistent accounting framework (GAAP/ASC 958), use plain language and visuals in board materials, clearly separate restricted from unrestricted funds, and seek third-party financial advisory review to verify accuracy. Consistent structure — not more pages — is what makes board materials genuinely useful.

What is the difference between restricted and unrestricted funds in nonprofit reporting?

Restricted funds are donor- or grantor-designated for a specific purpose and cannot be used for general operations. Unrestricted funds give the organization flexibility in how resources are allocated. Understanding both is essential for sound board decisions about operations and strategic priorities.

How often should nonprofits report financials to their board?

BoardSource recommends monthly or quarterly financial reporting throughout the year to avoid surprises at year-end. The annual year-end report serves as the comprehensive summary that ties back to each prior period's updates and provides the full fiscal picture.

What is the 5% materiality rule?

Materiality is an accounting concept where errors or omissions exceeding roughly 5% of a key financial figure — such as total expenses or net assets — are significant enough to require correction or disclosure. No formal "5% rule" exists in AICPA or FASB guidance; auditors apply professional judgment based on both quantitative and qualitative factors. Nonprofits should establish a written materiality policy so their finance team and auditors work from the same standard.