Introduction

Nonprofit leaders excel at advancing their missions—running food banks, managing conservation programs, staging live theater. The financial reporting side is a different challenge, and annual reports often show it. Boards and major donors increasingly scrutinize the financial substance behind the storytelling, not just the mission story.

According to BoardSource's 2023 Leading with Intent survey, boards consistently perform well on financial oversight but struggle with external-facing responsibilities. When financial data is poorly presented or incomplete, even the most mission-driven board member faces an uphill battle explaining the numbers to prospective funders.

This guide breaks down what financial literacy looks like for nonprofits specifically: which documents belong in an annual report, how to present data clearly, and where most organizations fall short. Getting these fundamentals right doesn't just satisfy auditors — it builds the donor confidence that sustains long-term growth.

Key Takeaways

- Nonprofit financial literacy means clearly communicating revenues, expenses, fund restrictions, and long-term sustainability to stakeholders

- Annual reports should include Statement of Financial Position, Statement of Activities, and functional expenses with donor-friendly explanations

- Transparency about restricted vs. unrestricted funds and reserve balances builds credibility with funders and boards

- Address narrative context and liquidity concerns directly — leaving them out signals weak governance and erodes funder trust

What Financial Literacy Really Means for Nonprofit Organizations

For nonprofits, financial literacy means whether your organization's leaders, board members, and staff understand the financial information driving strategic decisions. External funders increasingly expect nonprofit leadership to demonstrate fluency in both mission delivery and financial stewardship — and that expectation starts at the governance level.

Core Dimensions of Organizational Financial Literacy

Nonprofit financial literacy encompasses five critical dimensions:

- Revenue mix understanding — tracking grants, donations, and earned income separately

- Expense categorization — distinguishing program costs from overhead

- Cash flow management — monitoring timing of receipts and disbursements

- Adequate reserves — maintaining buffers for operational stability

- Fund restriction compliance — ensuring restricted funds serve designated purposes

Despite these fundamentals, gaps persist. BoardSource's 2016 financial literacy quiz found the average board member scored 81% — respectable, but still revealing blind spots at the governance level.

The staffing side compounds the problem. Research by BTQ Financial in 2025 found that 72% of nonprofits struggle with turnover in finance and accounting roles, with 38% reporting frequent or very frequent turnover. That instability directly undermines financial literacy across the organization.

Cash-Basis Thinking vs. Accrual-Basis Reality

Leaders who only watch the bank balance miss critical warning signs. Cash-basis accounting recognizes transactions only when money moves, which feels intuitive but leaves out important context. Accrual-basis accounting, required under GAAP, recognizes revenue when earned and expenses when incurred, regardless of cash timing.

According to Nonprofit Accounting Basics, cash-basis thinking creates timing gaps between transactions and payments, artificial monthly fluctuations, and difficulty forecasting future cash needs. Nonprofits relying solely on cash-basis thinking may appear flush one month and strapped the next, obscuring the true financial picture funders need to assess organizational health.

Internal vs. External Financial Information

Understanding the cash-accrual gap is just one layer. Nonprofit leaders also need to navigate two distinct types of financial information depending on the audience. Internally, management relies on budget variance analysis, program-level expense tracking, and cash flow projections to make operational decisions. Externally, annual reports and grant applications require summarized financial statements with narrative context that translates accounting language into mission impact.

Both require financial fluency. A treasurer who can't explain why restricted revenue appears on the balance sheet but not in available cash will struggle to guide board discussions about next year's budget.

FASB Net Asset Categories

That internal/external distinction connects directly to how net assets are classified. FASB Accounting Standards Update 2016-14 requires nonprofits to report net assets in two categories: with donor restrictions and without donor restrictions. This replaced the previous three-category model (unrestricted, temporarily restricted, permanently restricted) to simplify reporting while maintaining transparency.

Understanding this distinction is foundational. Board-designated reserves fall under "without donor restrictions" even if leadership intends them for specific purposes. Grant funds restricted to particular programs or time periods fall under "with donor restrictions."

Annual reports that blur this line create confusion about financial flexibility and mislead stakeholders about what resources are truly available for general operations.

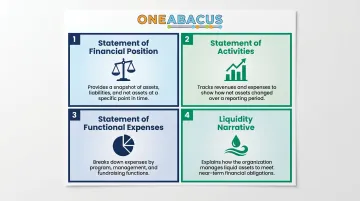

Essential Financial Statements in a Nonprofit Annual Report

Annual reports are not legally required, yet they serve as the primary vehicle for demonstrating financial accountability to donors, funders, and the public. Form 990 is a compliance document—publicly accessible but dense and technical. Annual reports offer a more accessible financial narrative.

Form 990 vs. Annual Reports

The IRS requires Form 990 for organizations with gross receipts of $200,000 or more or total assets of $500,000 or more. Failure to file for three consecutive years results in automatic loss of tax-exempt status. Small nonprofits with annual receipts under $50,000 may file Form 990-N (e-Postcard).

Form 990 satisfies legal reporting requirements and appears on public databases like GuideStar. Annual reports, by contrast, are voluntary documents designed to communicate impact and financial transparency in formats tailored to donor audiences. Sophisticated funders review both — but donors and community stakeholders typically turn to annual reports first.

Statement of Financial Position

The Statement of Financial Position (nonprofit equivalent of a balance sheet) shows:

- Assets - Cash, investments, receivables, property

- Liabilities - Accounts payable, deferred revenue, debt

- Net assets - With and without donor restrictions

Readers should look for liquidity (cash and near-cash assets), debt levels, and reserve balances. Make this accessible by including brief explanations: "Our cash reserves increased to $180,000, representing three months of operating expenses—a goal we reached for the first time this year."

Strip out excessive detail, but don't eliminate what matters to sophisticated funders. Major grantmakers want to see debt obligations, temporarily restricted balances, and whether your organization operates with a cushion or on the edge.

Statement of Activities

The Statement of Activities (income statement equivalent) captures revenue and expenses across the fiscal year. It should show program-specific performance rather than one aggregate number.

Hiding overhead costs within program expenses is a red flag. Charity Navigator and other watchdogs increasingly screen for cost allocation accuracy. Transparent reporting shows:

- Total program expenses by major program area

- Management and general (overhead)

- Fundraising costs

Funders who see this breakdown can assess how you allocate resources across your mission—and whether your numbers hold up under scrutiny.

Restricted vs. Unrestricted Funds

Grant-restricted revenue differs fundamentally from general operating support. A $100,000 grant restricted to youth programming cannot pay the electric bill or executive salaries unless the grant explicitly allows indirect cost recovery.

Annual reports should clearly show:

- How much revenue arrived with donor restrictions

- How restricted funds were deployed during the year

- Remaining restricted balances at year-end

A foundation reviewing your annual report wants assurance that prior restricted grants were used appropriately before committing new dollars. Vague or missing restricted fund reporting is one of the fastest ways to lose a renewal grant.

Statement of Functional Expenses and Liquidity Narrative

The Statement of Functional Expenses, required under FASB ASU 2016-14, shows natural expenses (salaries, rent, supplies) allocated across program, management, and fundraising functions. This reveals efficiency in ways that aggregate expense totals cannot.

A liquidity narrative—also required under ASU 2016-14—explains what financial assets are available to meet cash needs within one year. Balance sheets show what you own; liquidity narratives show what you can actually access. For example: "As of year-end, we held $210,000 in liquid unrestricted assets, sufficient to cover four months of general operating expenses."

How to Present Financial Data That Builds Donor and Board Trust

Every financial figure should answer the "so what?" question. Raw numbers without context leave readers guessing. The goal is clarity, not confusion.

Translating Numbers for Donors

Plain-language translation examples:

- Instead of "program efficiency ratio of 0.87," say "87 cents of every dollar goes directly to programs"

- Instead of "net assets increased by $45,000," say "We ended the year with a stronger financial foundation, adding $45,000 to reserves—our first surplus in three years"

- Instead of "temporarily restricted net assets totaled $120,000," say "$120,000 in grant funds are earmarked for next year's literacy program expansion"

Practical techniques for visual accessibility include:

- Pie charts for revenue sources and expense allocation

- Year-over-year comparison charts to show growth or contraction

- Call-out boxes highlighting key metrics like months of reserves or percentage of budget from individual donors

Visuals should clarify, not obscure. Avoid burying overhead or reserve levels in footnotes. If your overhead ratio is higher than sector norms, explain why: "Administrative costs rose 12% this year due to a planned technology system upgrade that will reduce manual processing and improve data security."

The "You-Attitude" in Financial Reporting

Frame financial performance around donor impact:

- "Your contributions helped us maintain a three-month operating reserve for the first time in five years"

- "Thanks to your support, we expanded evening programs without adding debt"

- "Donor investment enabled us to allocate 89% of spending directly to mission-critical services"

That framing matters for board presentations too — when directors see the same donor-centered language reflected in financial reports, it reinforces why fiduciary oversight connects directly to mission outcomes.

Presenting to the Board

Boards need financial information in two contexts: regular board finance packets (monthly or quarterly) and annual reports. The board's fiduciary role requires ongoing oversight; annual reports should reinforce, not replace, this regular review.

BoardSource research identifies three legal duties for all board members:

- Duty of Care — making sound, informed decisions

- Duty of Loyalty — acting in the organization's best interest

- Duty of Obedience — adhering to legal and ethical standards

The board cannot delegate its primary fiduciary duty.

Organizations working with a fractional CFO through a firm like One Abacus Advisory have financial statements prepared to board-ready standards year-round, rather than assembled under deadline pressure at report time. Boards receive timely, accurate reports at every meeting, with annual reports serving as the public-facing summary of what the board has already reviewed in detail.

Common Financial Literacy Gaps in Nonprofit Annual Reports

Most annual report problems aren't about missing numbers. They're about missing context—and that gap quietly erodes donor and funder trust.

No Narrative Context for Financial Numbers

Reporting revenue and expenses without explaining variances, one-time items, or strategic decisions leaves donors guessing and erodes trust.

Example: A nonprofit's administrative costs spike 18% year-over-year. Without explanation, this looks like mission drift. With context:

"We completed a planned migration to cloud-based accounting software, incurring $22,000 in one-time setup and training costs that will reduce manual processing time by 40% going forward."

The increase signals strategic investment, not waste.

Incomplete or Misleading Fund Reporting

Nonprofits sometimes report total revenue without distinguishing restricted from unrestricted funds, creating an inflated impression of financial flexibility. A $500,000 revenue line looks strong until you realize $400,000 is restricted to a capital campaign and only $100,000 is available for operations.

Mission Edge identifies misclassifying restricted and unrestricted funds as one of the most common and costly accounting errors nonprofits make. It breaches donor trust and triggers compliance issues under FASB ASC 958. Grantmakers reviewing multiple funding cycles watch closely to ensure prior restricted awards were deployed appropriately.

Omission of Forward-Looking Financial Context

Annual reports that only look backward miss the opportunity to demonstrate resilience planning. Strong organizations include:

- A brief statement on reserve policy (e.g., "Our board maintains a policy target of three months' operating reserves")

- Upcoming capital needs (e.g., "Next year we will replace our aging HVAC system, budgeted at $35,000 and fully funded through a designated capital reserve")

- Revenue diversification strategy (e.g., "We are actively reducing dependence on a single government contract, which currently represents 60% of revenue, by expanding individual donor cultivation")

Funders making multi-year commitments want evidence that an organization plans beyond the current fiscal year. These disclosures answer that question directly—before it gets asked.

How Strategic Financial Leadership Strengthens Your Annual Report

The quality of your annual report's financial section directly reflects the quality of financial management throughout the year. Organizations that track program-level expenses, maintain clean fund accounting, and reconcile regularly produce annual reports with credible, audit-ready financial data.

The Role of a CFO or Fractional CFO

A CFO or fractional CFO plays a specific role in annual report preparation:

- Reviewing financial statement accuracy - Ensuring numbers match general ledger balances and audit trails

- Ensuring GAAP compliance - Applying FASB nonprofit accounting standards correctly

- Translating complex accounting outcomes into narrative - Drafting explanations that make sense to non-accountants

- Coordinating with auditors - Confirming that financials are presentation-ready and audit findings are addressed

For many mid-sized nonprofits, 30% now outsource finance and accounting functions to access CFO-level guidance they cannot afford full-time. A fractional CFO from a firm like One Abacus Advisory provides this expertise at a fraction of the cost, giving boards the financial clarity they need when annual reporting demands are highest.

One Abacus Advisory's engagement with the Philadelphia Zoo shows what this looks like in practice. Following the simultaneous departure of the CFO and Controller, One Abacus provided accounting assessment, fractional CFO and Controller support, and NetSuite optimization.

The outcomes included faster month-end close cycles, stronger board reporting, and uninterrupted financial operations through the full recruitment and onboarding of permanent leadership.

Strong Financial Systems Enable Faster, More Accurate Reporting

Well-configured accounting platforms—such as NetSuite, Sage Intacct, or QuickBooks Online—make annual report preparation faster and more accurate. Data is clean, categorized, and accessible throughout the year rather than reconstructed at year-end.

System optimization typically covers:

- Workflow automation to reduce manual data entry and close bottlenecks

- Reporting enhancements that surface program-level and fund-level data quickly

- User training that strengthens internal controls and supports compliance

Organizations with these systems in place can generate financial statements in hours, not weeks, freeing leadership to focus on narrative and strategic messaging rather than data reconciliation.

Frequently Asked Questions

What does a financial advisory board do?

A nonprofit financial advisory board (or finance committee) reviews budgets, monitors financial statements, oversees audits, and advises leadership on financial strategy. It works closely with the treasurer and CFO to analyze financial data before presenting recommendations to the full board.

What are the 5 principles of financial literacy?

In a nonprofit context, the five principles are: earning (revenue management across diverse sources), saving (building and maintaining reserves), spending (expense control and program efficiency), borrowing (debt awareness and responsible leverage), and protecting (risk management, insurance, and compliance). Each applies to organizational financial health, not just personal finance.

What is the difference between a nonprofit annual report and Form 990?

Form 990 is a mandatory IRS filing satisfying legal reporting requirements, publicly accessible, and formatted for regulatory compliance. An annual report is a voluntary, donor-facing document designed to communicate impact, financial transparency, and mission progress in an accessible, narrative-driven format tailored to stakeholders.

What financial statements should be included in a nonprofit annual report?

Include the Statement of Financial Position, Statement of Activities, and ideally a Statement of Functional Expenses, along with a brief liquidity narrative. Present these with plain-language explanations rather than raw accounting output to ensure accessibility for donors and community stakeholders.

How should nonprofits explain restricted vs. unrestricted funds in an annual report?

Clearly show both categories of net assets, briefly describe what major restrictions apply (e.g., "Grant funds designated for youth programming"), and explain how restricted funds were deployed during the year. Avoid presenting restricted revenue as general operating income to maintain funder trust and transparency.

How often should nonprofit boards review financial reports?

Boards should review financial statements at every meeting—typically monthly or quarterly—with deeper reviews during budget approval and audit cycles. Annual reports reinforce this ongoing oversight; they don't replace it.

Financial literacy is a leadership competency—one that strengthens governance, builds donor trust, and protects your mission. Annual reports that present financial data with clarity and context signal mature stewardship to funders, boards, and communities. Organizations that invest in ongoing financial leadership—whether through full-time hires, fractional CFOs, or advisory partnerships—consistently produce stronger annual reports because that rigor runs throughout the year, not only during reporting season.

If your nonprofit is preparing an annual report and facing challenges with financial statement accuracy, GAAP compliance, or translating complex data into donor-friendly narratives, consider reaching out to One Abacus Advisory for a consultation. Their fractional CFO and financial leadership services help nonprofits navigate these exact challenges with nonprofit-focused expertise and a flexible, right-sized approach built around each organization's needs.