Introduction

Picture this: Your finance team spends three months building the annual budget in isolation, presents it to leadership for approval in a single board meeting, and then files it away until year-end reconciliation. It's a common pattern — and one that disconnects financial planning from operational reality.

36% of nonprofits ended 2024 with an operating deficit — the highest level in a decade — while 52% hold three months or less of cash on hand. These aren't just numbers; they're symptoms of budget processes that lack cross-functional input and ongoing oversight.

If your organization is navigating these pressures, the problem often isn't the numbers — it's the process behind them. This article covers why siloed budgeting fails, what genuine cross-functional collaboration looks like in practice, and how to build a forecasting process that keeps your mission and your finances moving in the same direction.

Key Takeaways

- Collaborative budgeting means finance, program, development, and leadership work together — not in handoff sequence

- Budgets are plans; forecasts are progress checks — both require cross-team input to stay accurate

- Program staff own cost reality, development owns revenue projections, and finance ties it all together

- Unclear roles, late input, and post-approval silence are the most common reasons the process breaks down

- Without a full-time CFO, fractional financial leadership can own and drive this process for your team

What Is Collaborative Budgeting in Nonprofits?

Collaborative budgeting is the structured process where multiple stakeholders across departments and leadership levels contribute to building, validating, and monitoring a nonprofit's financial plan. Finance leads it, but the process depends on meaningful input from across the organization.

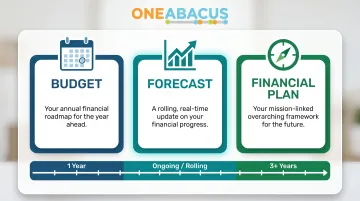

Three terms that are often used interchangeably — but shouldn't be:

According to AICPA guidance, these are distinct components:

| Component | Definition | Time Horizon |

|---|---|---|

| Budget | Annual financial roadmap tied to organizational goals | Planning year (1 year) |

| Forecast | Rolling, real-time update tracking progress against the budget | Ongoing throughout the year |

| Financial Plan | Overarching framework linking mission with resources | Minimum 3 years total |

Conflating these leads to poor decisions — like treating a static budget as gospel when reality has shifted dramatically by June. Getting the definitions right is only part of the challenge — the harder problem is building a process that actually works.

The Gap Most Nonprofits Face

Collaborative budgeting is widely referenced in nonprofit finance, but rarely designed with clear ownership, defined timelines, or role-based accountability. When that structure is missing, the same failure patterns repeat:

- Deadlines slip as departments wait on each other for inputs

- Submissions arrive incomplete, forcing finance to fill gaps with assumptions

- Final budgets reflect the loudest voice in the room, not the most informed one

Why Collaboration Shapes Financial Outcomes in Nonprofits

Nonprofits operate with uniquely complex funding: restricted grants, unrestricted donations, earned revenue, government contracts. Only cross-departmental input can accurately capture how these streams align with program costs.

What Goes Wrong Without Collaboration

Finance builds projections using assumptions that program staff would immediately flag as wrong. Development submits optimistic grant figures with no pipeline to support them. Leadership approves a budget disconnected from operations — and by mid-year, the organization is scrambling to reforecast or cover unexpected shortfalls.

Consider the data:

- 41% of large nonprofits cite diversification of funding sources as a top financial challenge

- Fewer than 1% of nonprofits rely on a single revenue source — most juggle multiple streams simultaneously

- 84% of nonprofits receiving government funding expect cuts, while 85% expect service demand to increase

Governance Expectations

Those funding pressures make collaboration a governance issue, not just an operational one. Boards and auditors expect budgets built on documented assumptions with staff-level input — not numbers that appeared from the finance office alone. The National Council of Nonprofits describes budget approval as a "fundamental building block of sound financial management."

How the Collaborative Budget and Forecast Process Works

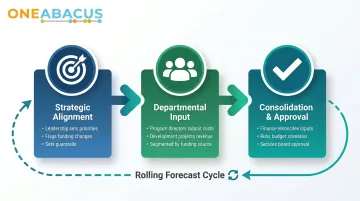

The process moves from strategic goal-setting at the top, to departmental input from the middle, to financial consolidation and board approval at the end — then continues as a rolling forecast cycle rather than a one-time annual event.

Critical timing: Begin 2–3 months before the fiscal year start. Delayed starts are one of the most common and avoidable sources of dysfunction.

Step 1: Strategic Alignment

Leadership (executive director and finance lead) defines the organization's strategic priorities, expected funding constraints, and any known changes in program scope for the coming year. This gives department heads the parameters they need to build realistic projections.

What this looks like:

- Review prior year performance and identify variances

- Confirm board-approved strategic priorities for the coming year

- Flag known funding changes (expiring grants, expected cuts, new opportunities)

- Set revenue assumptions and spending guardrails

Step 2: Departmental Input and Revenue Projection

Program directors submit detailed cost estimates for their activities. Development staff project income by funding category — restricted grants by grant, individual giving, events.

Budgets gain real accuracy at this stage because program and development staff know their pipelines and cost drivers better than finance does. That knowledge only translates into reliable numbers when staff have clear guidance on how to document it.

Key considerations:

- Program staff need guidance on restricted vs. unrestricted fund distinctions to avoid compliance issues

- Development projections should be tied to pipeline data, not aspirational targets

- Each department should document assumptions (for example, "assumes 10% donor retention increase")

This is also where nonprofits without dedicated financial leadership often struggle — staff submit numbers without context, and finance has to guess at the reasoning behind them. One Abacus Advisory addresses this directly by providing financial literacy coaching to non-finance staff and building input templates that make assumptions explicit from the start.

Step 3: Finance Consolidation, Scenario Testing, and Approval

Finance consolidates all inputs into a unified model and identifies gaps or mismatches — for example, expenses exceeding projected revenue in Q2. From there, the team runs scenarios (conservative vs. optimistic) and brings a draft back to leadership for review.

The process includes:

- Reconciling departmental inputs with overall funding capacity

- Testing scenarios: What if grant X doesn't come through? What if inflation exceeds projections?

- Preparing board-ready summaries with narrative context

- Securing board finance committee review before full board approval

After approval, the budget becomes the baseline for a monthly or quarterly rolling forecast — comparing actuals against projections and adjusting proactively rather than reactively at year-end.

Who Should Be Involved and What They Contribute

Effective nonprofit budgets have defined roles with specific inputs expected from each. Not "everyone weighs in" chaos, but structured, accountable participation.

Executive Director / CEO

Responsibility: Set strategic direction and final organizational priorities before numbers are built.

Role in process:

- Frame constraints and goals that shape the budget

- Bridge staff input and board expectations

- Should not be building the budget model but must approve the strategic framework

Program and Operations Staff

Responsibility: Provide the most grounded cost projections because they know what programs actually cost to deliver.

What they contribute:

- Staffing needs by program

- Direct program costs (supplies, travel, subcontractors)

- Changes in scope or service levels

- Assumptions about client volume or service intensity

This input is often the most underused in nonprofit budgeting, and consistently the most valuable.

Development and Fundraising Staff

Responsibility: Project contributed revenue by source and restriction status.

What they contribute:

- Pipeline data: grants applied for, pending, and awarded

- Grant calendars showing expected award timing

- Donor retention assumptions based on historical data

- Event revenue projections with supporting detail

Warning: Revenue projections from this team that aren't grounded in actual pipeline data routinely produce mid-year budget shortfalls.

Finance Lead or Fractional CFO

Responsibility: Serve as the process owner and financial translator.

What they do:

- Consolidate inputs from all departments

- Stress-test assumptions and flag risks

- Build scenario models

- Present the board-ready version with narrative context

Many mid-size nonprofits without a full-time CFO bring in a fractional CFO to own this process — One Abacus Advisory works with nonprofits in exactly this capacity, keeping the budget cycle on schedule and the assumptions defensible. Median nonprofit CFO compensation is approximately $125,000–$152,000 per year, making fractional arrangements cost-effective for organizations under $10M in revenue.

Key Factors and Common Pitfalls That Affect Budget Collaboration

Several structural factors quietly undermine collaboration before the first number is entered. Recognizing them is the first step toward fixing them.

Timing Failures

Launching the budget process too close to the fiscal year start leaves insufficient time for meaningful departmental input. Best practice: start 2–3 months before fiscal year-end.

Restricted Fund Complexity

When program staff don't understand which costs are grant-eligible, finance ends up correcting assumptions after submission — creating rework and friction. Clear guidance up front prevents this.

Version Control and Data Integrity

61% of nonprofit organizations continue to use spreadsheets for core financial management, while only 24% achieve organization-wide data sharing. Spreadsheet-based processes with multiple emailed versions create conflicting numbers and erode trust.

Unclear Accountability

When no one owns the process end-to-end, deadlines slip, inputs arrive incomplete, and the budget reflects the loudest voice rather than the most informed one.

The Persistent Misconception

The budget is "done" once it's approved. In well-run nonprofits, the budget is updated monthly through active forecasting, so leadership can course-correct in real time rather than discovering problems at year-end.

These pitfalls compound each other. Nonprofit finance teams typically spend 70–80% of their time on manual data gathering and reconciliation — leaving only 20–30% for actual analysis. Collaborative systems and FP&A tools can flip that ratio, giving finance staff more time to surface insights rather than chase numbers.

Frequently Asked Questions

What is the 50 30 20 rule for charities?

This informal rule suggests allocating roughly 50% of a nonprofit's budget to programs, 30% to operations/overhead, and 20% to fundraising. It's not a regulatory standard or recognized benchmark — actual ratios vary significantly by organization type and mission.

Who should be involved in a nonprofit's budget process?

At minimum: the executive director, finance lead, program directors, and development staff should each contribute. The board finance committee reviews, and the full board approves the final budget.

What is the difference between a nonprofit budget and a forecast?

A budget is the annual financial plan approved before the fiscal year begins. A forecast is an ongoing update that compares actual performance against the budget and adjusts projections for the rest of the year.

How often should a nonprofit update its financial forecast?

Monthly forecast updates tied to the month-end close cycle are ideal. Minimum: quarterly updates for smaller organizations.

Why do nonprofit budgets often fall apart mid-year?

The most common causes:

- Overstated revenue projections, especially for grants not yet awarded

- No rolling forecast to catch variance early

- A budget built without sufficient input from program and development staff

What role does a fractional CFO play in nonprofit budget collaboration?

A fractional CFO typically owns the entire budget process: setting timelines, guiding department heads through their input, consolidating the model, and presenting a board-ready budget. For nonprofits without a full-time CFO, this fills a critical operational gap.