Introduction

The balance sheet — formally called the Statement of Financial Position — stands as one of the most critical financial documents a nonprofit produces, yet finance staff and board members often struggle to prepare it correctly. Unlike for-profit businesses, nonprofits operate under distinct accounting rules governed by FASB standards — particularly around how funds are classified and reported.

The underlying equation is straightforward — Assets = Liabilities + Net Assets — but accurate preparation involves several nonprofit-specific requirements:

- Classifying net assets according to donor restrictions

- Applying GAAP standards for nonprofit reporting

- Tracking fund limitations with precision

- Selecting the right accounting method for your organization

This guide covers what makes a nonprofit balance sheet unique, the step-by-step preparation process, key variables that affect accuracy, and the most common mistakes to avoid. Get this right, and your Statement of Financial Position gives your board and leadership team the financial clarity to make stronger decisions.

Key Takeaways

- Nonprofits report "net assets" rather than "owner's equity" using the equation: Assets = Liabilities + Net Assets

- FASB ASU 2016-14 requires splitting net assets into two categories: "with donor restrictions" and "without donor restrictions"

- Accurate preparation requires complete financial records, assets categorized by liquidity, and a balanced equation

- Accrual-basis accounting produces more accurate balance sheets than cash-basis by capturing pledges and deferred revenue

- Pair the balance sheet with the Statement of Activities, Cash Flows, and Functional Expenses for a complete financial picture

What Makes a Nonprofit Balance Sheet Unique

Unlike for-profit balance sheets that display "owner's equity," nonprofit balance sheets use the term "net assets" — reflecting a fundamental truth: nonprofits have no shareholders and exist solely to advance a mission, not distribute profits to owners.

Terminology and Structural Differences

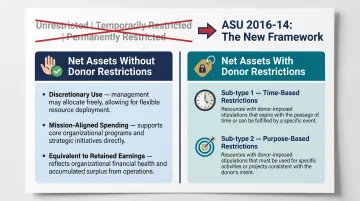

The formal name for a nonprofit balance sheet is the Statement of Financial Position, per FASB ASU 2016-14, issued in August 2016 and effective for fiscal years beginning after December 15, 2017. This standard represents the first major overhaul of nonprofit financial statement presentation since 1993.

The most significant change: replacing the older three-category system (unrestricted, temporarily restricted, and permanently restricted net assets) with a streamlined two-category framework:

- Net assets without donor restrictions — funds the organization can use at its discretion for any mission-aligned purpose

- Net assets with donor restrictions — funds subject to donor-imposed limitations, either time-based or purpose-based

Why Donor Restrictions Add Complexity

Donor restrictions make nonprofit balance sheets uniquely challenging. Restricted funds cannot be spent freely, must be tracked separately throughout the fiscal year, and require consistent, documented reporting to maintain donor trust, IRS compliance, and audit readiness.

According to the Journal of Accountancy, donor gift classification is "one of the most common issues leading to not-for-profit restatements." Misclassifying a restricted gift can set off a chain of consequences:

- Audit findings that require management response and remediation

- Financial restatements that signal control weaknesses to funders

- Damaged stakeholder confidence that's difficult to rebuild

Every restricted contribution should be tied to a documented donor agreement specifying the exact nature and duration of the restriction.

What You Need Before Preparing Your Nonprofit Balance Sheet

Before you build your balance sheet, gather the right documents and confirm your accounting method. Missing either step leads to inaccurate financials that won't hold up under audit, grant review, or Form 990 scrutiny.

Financial Records and System Requirements

Compile these essential documents:

- Bank and investment account statements (all accounts, including endowments)

- Accounts receivable aging schedules

- Pledges and contribution receivables with restriction documentation

- Prepaid expense schedules

- Fixed asset registers with accumulated depreciation

- Accounts payable and accrued expense schedules

- Loan and mortgage statements

- Deferred revenue schedules (advance registrations, membership fees, conditional grants)

Accounting Method Decision

Your accounting method shapes balance sheet accuracy.

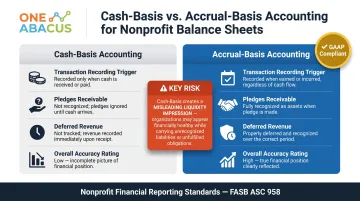

Cash-basis accounting records transactions when cash is received or paid — simpler to maintain but potentially misleading. A cash-basis balance sheet omits pledges receivable as assets and deferred revenue as liabilities, making liquidity appear stronger than reality.

Accrual-basis accounting records revenue when earned and expenses when incurred, regardless of cash movement. This approach is more accurate and GAAP-compliant. According to IRS Form 990 instructions, while the IRS permits either method on Form 990, many states that accept Form 990 in place of their own forms require accrual-basis reporting. Smaller organizations may use cash-basis for day-to-day simplicity, but that choice has real consequences when grant applications or audits require a complete picture of your financial position.

Compliance Readiness

Once your records and method are in order, confirm your balance sheet aligns with:

- GAAP standards

- FASB nonprofit reporting requirements (particularly ASU 2016-14)

- Your organization's chart of accounts structure

- Documented donor agreements supporting restricted fund classifications

How to Prepare a Nonprofit Balance Sheet: Step-by-Step

Step 1: Set Your Reporting Date and Period

Identify the "as of" date for your balance sheet — typically the last day of your fiscal year, fiscal quarter, or month. The balance sheet captures a point-in-time snapshot, not a period summary.

Best practice: prepare comparative balance sheets showing two years side-by-side (current year and prior year). FASB ASU 2016-14 notes that the reduction to two net asset classes enables "greater use of multiperiod comparative financial statements." Side-by-side comparisons support trend analysis for board reporting and audits.

Step 2: Compile and Categorize Assets

Current Assets (convertible to cash within 12 months):

- Cash and cash equivalents

- Short-term investments

- Accounts receivable

- Contributions/pledges receivable (net of allowance for uncollectible amounts)

- Prepaid expenses

- Inventory (if applicable)

Fixed/Noncurrent Assets:

- Property, land, and buildings

- Equipment and leasehold improvements

- Less: Accumulated depreciation

Fixed assets appear at net book value on the balance sheet. GAAP requires depreciation for most fixed assets, recognizing the decrease in value over each asset's useful life.

Other Long-Term Assets:

- Long-term investments

- Endowment assets held in perpetuity

- Intangible assets (patents, trademarks) less amortization

Step 3: List and Categorize Liabilities

Current Liabilities (due within 12 months):

- Accounts payable

- Accrued salaries and benefits

- Accrued expenses

- Short-term loan payments

- Deferred revenue (advance registrations, membership fees earned over time)

- Refundable advances on conditional grants

Long-Term Liabilities (due beyond 12 months):

- Mortgages

- Multi-year loans

- Finance leases

- Pension obligations

- Long-term deferred revenue

Order all liabilities by due date for clarity. Once your liabilities are tallied, you have everything you need to calculate net assets — the figure that shows what your organization actually owns after obligations are accounted for.

Step 4: Calculate and Classify Net Assets

Calculate total net assets using the formula:

Net Assets = Total Assets − Total Liabilities

Then split into FASB-required categories:

Net assets without donor restrictions: Funds available for any mission-aligned expense — earned revenue, unrestricted donations, and membership dues. This is the nonprofit equivalent of retained earnings.

Net assets with donor restrictions: Funds subject to donor-imposed limitations, either time-based (available after a future date) or purpose-based (designated for specific programs, capital projects, or endowment principal).

Note: Per FASB ASU 2018-08, conditional contributions must be recorded as refundable advances (liabilities) until conditions are substantially met or waived — not as restricted net assets.

Step 5: Verify the Equation and Finalize

Confirm that Total Assets = Total Liabilities + Total Net Assets.

If the equation doesn't balance, reconcile each section against source records before finalizing. Common discrepancies include missing depreciation entries, unrecorded liabilities, or misclassified transactions.

Include a statement header with:

- Organization's legal name

- Title: "Statement of Financial Position"

- Reporting date (e.g., "As of December 31, 2024")

- Accounting basis (cash or accrual)

- Footnotes documenting significant accounting policies, major donor restrictions, and comparative prior-period figures

A complete, balanced Statement of Financial Position gives boards and stakeholders a reliable picture of organizational health — and a solid foundation for audit preparation, grant reporting, and strategic planning.

Key Variables That Shape Your Nonprofit Balance Sheet

Even with accurate inputs, four variables consistently determine whether a nonprofit balance sheet is useful, compliant, and audit-ready.

Accounting Basis (Cash vs. Accrual)

Accrual-basis accounting captures pledges receivable as assets and deferred revenue as liabilities, giving stakeholders a complete view of obligations and receivables. Cash-basis omits both, which can distort the picture in one specific, high-stakes way: a large restricted grant received in advance will show as strong cash reserves, with no corresponding liability recorded for the future deliverables attached to it. The result is a misleading impression of available operating funds — a problem that surfaces quickly during audits or board reviews.

Net Asset Classification Accuracy

Misclassifying restricted funds as unrestricted violates FASB ASU 2016-14 and can trigger audit findings and IRS scrutiny. More immediately, it gives leadership a false sense of available operating funds — a governance risk that rarely surfaces until it's costly.

The Journal of Accountancy identifies net asset misclassification as one of the most common causes of nonprofit financial restatements.

Depreciation of Fixed Assets

Grant funds received before conditions are met — and event fees collected before the event occurs — must be recorded as liabilities, not revenue. This distinction matters because:

- Skipping this entry understates total liabilities and overstates net assets

- Overstated net assets invite compliance findings and misrepresent financial health

- Under ASC 958-605-25-5F, conditional contributions must remain as refundable advances until all barriers to entitlement are cleared

This is one of the more common errors in nonprofit accounting — and one that fractional CFO support tends to catch early, before it compounds into a restatement.

Common Mistakes Nonprofits Make When Preparing Their Balance Sheet

Misclassifying or Ignoring Donor Restrictions

Recording restricted grants or major gifts as unrestricted net assets is one of the most damaging errors. It misleads board members about available operating funds and can create donor relations problems, audit findings, and compliance violations.

Every restricted contribution should be tied to a donor agreement on file, clearly documenting the nature, purpose, and duration of the restriction.

Using the Balance Sheet in Isolation

Reviewing the balance sheet without the other financial statements leaves critical gaps in financial understanding. A balance sheet showing strong net assets can coexist with a cash flow crisis or unsustainable expense structure.

Read all four statements together for the full picture:

- Statement of Financial Position (Balance Sheet)

- Statement of Activities

- Statement of Cash Flows

- Statement of Functional Expenses

Preparing the Balance Sheet Infrequently or Only at Year-End

Organizations that only prepare a balance sheet annually for Form 990 filing miss ongoing trends, accumulate errors, and have no early warning system for financial issues.

The best practice is monthly preparation with regular board review. According to BoardSource, financial statements should be reviewed at every board meeting.

For organizations with complex fund structures or limited internal capacity, a fractional CFO advisor can provide ongoing accuracy without the cost of a full-time hire.

How to Read and Use Your Balance Sheet Strategically

Calculating Key Financial Metrics

Use balance sheet data to calculate critical health indicators:

Months of Cash on Hand = Cash & Cash Equivalents ÷ ((Total Expenses - Depreciation) ÷ 12)

This metric reveals how long your organization could continue operations using current cash reserves. According to the 2025 NFF State of the Nonprofit Sector Survey, 52% of nonprofits have three months or less cash on hand, and 18% have one month or less — highlighting widespread financial fragility.

Liquid Unrestricted Net Assets (LUNA) = Unrestricted Net Assets - (Property, Plant & Equipment - Related Debt)

LUNA reveals the true cushion available for unexpected problems or opportunities, excluding funds tied up in buildings and equipment. Calculate LUNA in months by dividing by average monthly expenses.

Current Ratio = Current Assets ÷ Current Liabilities

Per Propel Nonprofits, a ratio of 1.0 or higher is desirable, indicating sufficient short-term assets to cover short-term obligations.

Year-Over-Year Trend Analysis

These metrics carry the most weight when tracked over time. A single balance sheet is a snapshot — comparing two or three years reveals patterns:

- Growing restricted assets relative to unrestricted ones (indicating dependency on restricted funding)

- Rising leverage ratios (increasing debt burden)

- Declining liquidity (shrinking cash reserves)

Use these trends to drive strategic planning, reserve-building, and program investment decisions.

Applying the Balance Sheet to Stakeholder Reporting

Nonprofits use balance sheet data in multiple contexts:

- Grant applications: Demonstrating financial stability to funders

- Annual reports: Building donor confidence through transparency

- Board meetings: Supporting strategic decision-making with financial health indicators

- Independent audits: Providing auditors with accurate, reconciled data

Each of these contexts demands accurate, well-organized data — which is why the balance sheet is one of the most consequential documents your organization produces. Organizations navigating growth, leadership transitions, or increased funding complexity often work with a fractional CFO to make sure that data is both reliable and strategically actionable.

Frequently Asked Questions

What is the golden rule of the balance sheet?

The golden rule states that Assets must always equal Liabilities plus Net Assets. This fundamental equation must balance at all times, and any discrepancy signals a recording error that needs correction before finalizing the statement.

What is the equivalent of retained earnings in the nonprofit world?

Net assets without donor restrictions (formerly called unrestricted net assets) represents the nonprofit equivalent of retained earnings. It reflects accumulated surplus the organization can deploy at its discretion for any mission-aligned purpose.

How is a nonprofit balance sheet different from a for-profit balance sheet?

Nonprofits use "net assets" instead of "owner's equity," title the document "Statement of Financial Position," and must classify net assets by donor restriction status per FASB ASU 2016-14. These requirements reflect the fundamental difference: nonprofits have no shareholders and exist to advance a mission, not distribute profits.

What accounting method should nonprofits use for their balance sheet?

Accrual-basis accounting is the GAAP standard and produces more accurate balance sheets by recognizing pledges as assets and deferred revenue as liabilities. Cash-basis is simpler but can be misleading — and is generally not appropriate for organizations undergoing audits or filing Form 990 with significant revenue.

How often should a nonprofit prepare a balance sheet?

At minimum, a balance sheet is required annually for Form 990 filing. Best practice is monthly preparation so leadership and the board can monitor financial health, catch errors early, and track trends throughout the fiscal year.

Do donors and the public have a right to see a nonprofit's balance sheet?

Yes. Form 990 Part X (which includes balance sheet data) is a public document available on the IRS website and through platforms like ProPublica's Nonprofit Explorer. Many nonprofits also include balance sheet data in annual reports to strengthen donor trust.