Introduction

Audit deficiencies are among the most preventable threats to nonprofit financial health, yet they appear consistently in audit reports across the sector. When auditors identify significant deficiencies or material weaknesses in your organization's internal controls, the consequences reach well beyond immediate embarrassment — damaged donor confidence, jeopardized grant funding, and increased regulatory scrutiny all follow.

Research from the Government Accountability Office shows that 65% of audit findings in federal grant programs are repeat findings, meaning organizations fail to address the same issues year after year.

Most audit deficiencies trace back to identifiable root causes, not mysterious accounting problems. Weak segregation of duties, disorganized documentation, improper restricted fund tracking, and insufficient financial staff expertise account for the vast majority of reportable findings. Understanding these causes and implementing controls to prevent them is the foundation of consistent clean audit opinions. This guide walks through the most common deficiency areas and the practical steps your organization can take to address each one.

Key Takeaways

- Audit deficiencies arise when internal controls fail to prevent or detect financial misstatements

- Poor segregation of duties, disorganized documentation, mismanaged restricted funds, and limited financial expertise cause most nonprofit audit findings

- Prevention requires year-round discipline, documented policies, and qualified financial oversight

- Nonprofits with dedicated financial leadership — whether in-house or fractional — resolve findings faster and avoid repeat deficiencies

Common Causes of Audit Deficiencies in Nonprofits

Audit deficiencies occur when the design or operation of an internal control fails to allow management or staff to prevent or detect misstatements on a timely basis. Under auditing standards, there are two distinct types: deficiencies in design exist when the control doesn't exist or is improperly designed, while deficiencies in operation occur when the control exists but isn't followed or isn't performed by someone with proper authority.

Nonprofit organizations face higher-than-average risk of deficiencies due to lean staffing, volunteer-driven operations, and complex fund accounting requirements. Most deficiencies stem from one or more of the root causes below.

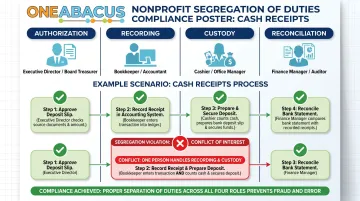

Weak or Absent Segregation of Duties

Segregation of duties failures occur when one person controls multiple steps of a financial transaction—for example, opening mail, recording receipts, preparing deposits, and reconciling the bank account. This structure opens the door to undetected errors or misappropriation.

This is the single most commonly cited deficiency in small-to-mid-size nonprofit audits. The National Council of Nonprofits identifies segregation of duties as a foundational internal control, defining it as requiring that "the person who logs in checks received in the mail is not the same person who is responsible for depositing checks" and that "the same person should not both prepare the payroll, and also distribute or have custody of paychecks." The AICPA even provides a dedicated reference chart for organizations with as few as three staff members, acknowledging how widespread this challenge is.

Incomplete or Disorganized Financial Documentation

Auditors require supporting documentation for every material transaction—receipts, contracts, bank statements, and grant agreements. Missing or poorly organized records force auditors to note a deficiency in operation, even when transactions were handled correctly.

According to peer reviews of nonprofit audits conducted in 2023, insufficient documentation was the most common problem, noted in more than 50% of all audits reviewed.

Typical scenarios include:

- Year-end scrambles to locate supporting files

- Inconsistently labeled or filed records

- Financial statements prepared outside the accounting system in spreadsheets

- Missing grant documentation or expenditure approvals

These documentation failures flag reportable deficiencies under auditing standards, even when the underlying transactions were legitimate and proper.

Improper Tracking of Restricted Funds

Donor-restricted and grant-restricted funds must be tracked, spent, and reported separately from unrestricted funds. Commingling funds, failing to release restrictions when conditions are met, or lacking proper grant documentation leads to compliance findings—especially in organizations subject to Single Audits under OMB Uniform Guidance.

When staff lack systems to identify which expenses satisfy which restrictions, questioned costs follow. Per federal regulations, a questioned cost is an amount the auditor judges as noncompliant with federal statutes, lacking adequate documentation, or appearing unreasonable.

In a 2025 GAO review of TANF single audit findings, 22% involved questioned costs, with one finding totaling nearly $1.3 million.

Organizations that spend **$1,000,000 or more in federal awards** during their fiscal year must have a Single Audit conducted under 2 CFR 200.501—a threshold raised from $750,000 in April 2024.

Insufficient Financial Staff Expertise or Capacity

Nonprofits with limited or undertrained finance staff frequently produce financial statements that do not conform to GAAP, which requires the auditor to create or significantly adjust financial statements—a direct deficiency in operation. The National Council of Nonprofits' 2023 survey found that 74.6% of nonprofits reported job vacancies, and a separate 2025 report found that 72% of nonprofits struggle with finance staff turnover.

Leadership transitions, staff turnover, and volunteers handling financial functions without proper training all contribute to this deficiency type. When the person preparing financial statements lacks the skills to do so correctly, auditors must evaluate whether management has the competence to oversee the process—a recurring finding in peer reviews.

What Happens If Audit Deficiencies Go Unaddressed

Audit findings follow an escalating severity scale. Control deficiencies that go unresolved year over year can be elevated to significant deficiencies and eventually material weaknesses. Each level increases the risk of a modified or adverse audit opinion, which signals deeper financial integrity issues to funders and regulatory bodies.

The GAO found that 65% of TANF single audit findings were repeat findings persisting for at least one year, with 37 repeating for two or more years. Most critically, 48 of the 56 findings classified as material weaknesses were repeat findings—demonstrating the pattern of escalation when issues remain unaddressed. Three findings remained unresolved for over a decade.

Downstream consequences of repeated audit findings include:

- Lost grant eligibility as grantors view findings as financial stewardship failures

- Increased audit fees, since auditors spend more time testing weak controls

- Damaged donor trust and reputational harm

- IRS scrutiny or potential revocation of tax-exempt status

- Going concern disclosures in severe cases

These consequences rarely appear without warning. Watch for these early indicators that audit findings may be coming:

Warning Signs Your Nonprofit Is Heading for Audit Findings

- One staff member or volunteer handles end-to-end financial transactions with no independent review or oversight

- Financial reports are prepared in spreadsheets or external tools rather than directly from the accounting system, creating reconciliation gaps auditors must address

- Restricted fund balances are tracked informally or are not reconciled to supporting grant agreements regularly

How to Prevent Audit Deficiencies in Nonprofit Audits

Audit readiness is built through controls and practices maintained every month of the fiscal year, not scrambled together in the weeks before your auditor arrives.

Establish and Enforce Segregation of Duties

Redistribute financial responsibilities across multiple staff members or volunteers. Key separations include:

- Authorization, recording, and custody functions for cash receipts

- Check preparation versus check signing

- Bank reconciliation performed by someone other than the person who processes transactions

- Payroll preparation versus payroll distribution

For very small organizations where full segregation isn't feasible, implement compensating controls:

- Regular board review of bank statements and transaction registers

- Dual signatures on checks above a specified threshold (typically $2,500–$5,000)

- Periodic management or board treasurer review of financial activity

- Monthly reconciliation reviews by an independent party

Build Year-Round Documentation and Record-Keeping Practices

Implement a clear documentation policy specifying what supporting records are required for each transaction type and how they must be filed. This should be followed consistently, not just during audit season.

- Maintain digital or physical filing systems organized by vendor, grant, or transaction type

- Require approval signatures and supporting documentation before processing any payment

- Generate financial statements directly from your accounting system, not spreadsheets

- Conduct quarterly documentation audits to catch gaps early

Accounting systems capable of generating GAAP-compliant financial statements directly eliminate a major source of reportable deficiencies. Nonprofit-specific platforms like NetSuite, Sage Intacct, and QuickBooks Online improve audit trail integrity when properly configured.

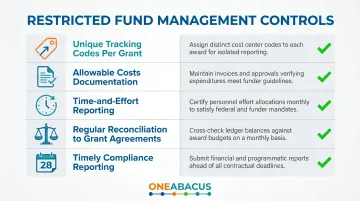

Implement Robust Restricted Fund and Grant Management Controls

Effective restricted fund management requires that each grant or donor restriction have its own tracking code in the accounting system, with regular reconciliation of spending against restriction terms and scheduled release of restrictions when conditions are satisfied.

Those grant management practices become even more consequential for organizations spending federal funds above $1,000,000 — where proper controls are essential to passing the compliance components of a Single Audit. Focus areas include:

- Documentation of allowable costs per grant terms

- Proper time-and-effort reporting for staff charged to federal grants

- Clear policies for fund usage and expenditure approval

- Regular reconciliation of restricted fund balances to grant agreements

- Timely submission of required reports (performance, financial, and compliance)

Common Single Audit findings include Activities Allowed/Unallowed, Allowable Costs/Cost Principles, Cash Management, Eligibility, Procurement, Reporting, and Subrecipient Monitoring. Each of these areas requires documented policies and consistent execution.

Invest in Qualified Financial Leadership Year-Round

The most effective long-term prevention strategy is having qualified, nonprofit-experienced financial leadership involved in the organization's accounting and reporting functions continuously—not just brought in to prepare for the audit.

Many nonprofits cannot justify the cost of a full-time CFO but can access the same quality of financial oversight through a fractional CFO model. One Abacus Advisory, for example, has partnered with organizations like the San Diego Food Bank and Philadelphia Zoo to provide exactly this kind of year-round financial stewardship. A fractional nonprofit CFO can:

- Establish and monitor internal controls tailored to your organization's size

- Ensure GAAP-compliant reporting throughout the year, not just at audit time

- Serve as the primary financial contact for auditors, reducing back-and-forth

- Identify compliance gaps before they become reportable findings

This model provides executive-level expertise at a fraction of full-time salary costs, with flexible engagement tailored to organizational size and complexity.

Tips for Long-Term Audit Readiness

Beyond immediate prevention measures, these ongoing practices keep nonprofits continuously prepared:

- Run quarterly internal financial reviews — even a board finance committee walkthrough of bank reconciliations and financial statements catches control gaps before the external auditor does.

- Maintain a written financial policies and procedures manual covering cash handling, expense approval, payroll, grant management, and financial reporting. Update it whenever staff roles change or new funding sources are added.

- Train staff and build board financial literacy so everyone involved in financial processes understands their role in the control environment and why consistent documentation matters.

- Schedule audit timelines around board calendars well in advance, and hold a pre-audit meeting with the auditor to surface new accounting issues, personnel changes, or unusual transactions. This keeps the process efficient and reduces surprises.

Nonprofits that treat audit readiness as a year-round discipline — not a seasonal sprint — fare better across the board. One Abacus Advisory's fractional CFO services can serve as an ongoing financial partner, maintaining this continuity between audits so nothing falls through the cracks.

Conclusion

Audit deficiencies in nonprofits have identifiable causes — primarily control design gaps, documentation failures, restricted fund mismanagement, and insufficient financial expertise. Each of these is preventable with the right habits and systems.

Proactive financial leadership, clear policies, and disciplined year-round practices separate organizations that consistently receive clean audit opinions from those that repeat the same findings year after year. The organizations that treat audit readiness as an ongoing discipline — not a once-a-year scramble — protect their funding, reduce compliance risk, and give their boards the confidence to focus on mission.

Frequently Asked Questions

What are the 5 C's of audit issues?

The 5 C's—Criteria, Condition, Cause, Consequence, and Corrective Action—come from the GAO's Government Auditing Standards (Yellow Book). Auditors use this framework to document every finding with a clear explanation of what happened, why it happened, and how to fix it.

What are the common mistakes in audit reports?

The most frequently cited issues are:

- Financial statements not prepared in conformity with GAAP

- Missing or inadequate supporting documentation

- Lack of segregation of duties

- Improper tracking of restricted funds

Most of these are preventable with stronger year-round financial controls and qualified oversight.

What is a significant deficiency in auditing?

A significant deficiency is a control deficiency—or combination of deficiencies—serious enough to warrant attention from those charged with governance, but less severe than a material weakness. It signals meaningful risk that a financial misstatement could go undetected or uncorrected.

What is the difference between a significant deficiency and a material weakness?

Both are reportable internal control findings, but a material weakness represents more severe risk. It indicates one or more controls are absent or ineffective such that a material misstatement in the financial statements could result and not be prevented or detected in a timely manner.

Can audit findings cause a nonprofit to lose grant funding?

Yes. Repeated or serious findings—especially material weaknesses or noncompliance in a Single Audit—can lead grantors and government agencies to withhold or decline to renew funding. They treat audit findings as direct evidence of how well an organization manages public resources.

How can nonprofits reduce audit costs?

Audit fees reflect auditor time — the less cleanup work required, the lower the bill. Organizations with well-organized records, GAAP-compliant financials, and strong internal controls consistently pay less. Qualified financial leadership year-round is the single most effective way to keep audit costs down.