Introduction

Nonprofit finance leaders face a persistent tension: joint cost allocation (JCA) offers a legitimate way to report shared program and fundraising expenses accurately—but when misapplied, it triggers state regulatory enforcement, IRS scrutiny, and donor distrust. The stakes are real: in 2009, the California Attorney General required National Veterans Foundation to amend its Form 990 filings after finding JCA criteria were not met. Reported program expenses plummeted from $7.75 million to just $929,000 for that fiscal year—a gap that fundamentally misrepresented the organization's financial profile.

If you oversee nonprofit financial reporting and want to stay on the right side of ASC 958-720-45, this guide is for you. Here's what we cover:

- What JCA is and when it applies

- The three qualifying tests under the standard

- Common pitfalls that trigger enforcement actions

- How regulators spot problems in 990 filings

- Practical steps for getting it right—and when to bring in outside financial expertise

Key Takeaways

- Joint-cost allocation (JCA) allows splitting certain campaign costs between program and fundraising — but only when three specific tests are met

- All three tests—purpose, audience, and content—must pass; failing any one means all costs go to fundraising

- Common mistakes include claiming JCA without a genuine program call to action and selecting audiences based on donor capacity rather than program need

- Improper JCA triggers state enforcement actions, IRS scrutiny, and reputational damage

- Solid documentation, a consistent allocation method, and periodic expert review are your best defenses

What Is Joint Cost Allocation in Nonprofit Accounting?

Joint costs are expenses for activities that simultaneously serve both fundraising and program purposes—such as a direct mail campaign that solicits donations while also delivering a meaningful educational message or call to action. These costs cannot be clearly identified with just one functional category.

The governing standard: ASC 958-720-45 (formerly SOP 98-2) is the GAAP guidance that permits—but tightly controls—how nonprofits may split these costs between functional expense categories on their financial statements and IRS Form 990. Key facts about the standard:

- Incorporated into the FASB Accounting Standards Codification on July 1, 2009

- Serves as the single authoritative source of U.S. GAAP for nonprofit entities

- Applies to both financial statements and IRS Form 990 functional expense reporting

JCA exists because some nonprofit activities genuinely serve dual purposes. The standard was designed to allow accurate reporting of those legitimate cases, not to minimize reported fundraising expenses on paper.

Used correctly, JCA reflects the true nature of an organization's work. Misapplied, it distorts financial transparency and gives donors an inaccurate picture of how their contributions are used.

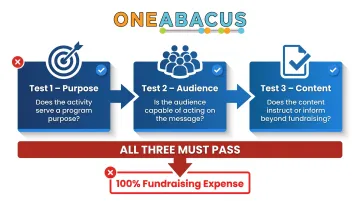

The Three Tests Every Nonprofit Must Pass

Under ASC 958-720-45, a nonprofit must satisfy all three tests—purpose, audience, and content—before any portion of a joint activity's cost can be allocated to program expense. If even one test fails, the entire cost must be classified as fundraising. There is no middle ground: all three criteria must be met, or the full cost goes to fundraising.

Purpose Test

The purpose test asks whether the activity would be conducted even if no donations were solicited. Auditors assess whether a genuine "call to action" that advances the nonprofit's mission is present, not merely a token mention inserted to justify the allocation.

Three sub-tests apply:

- Compensation-or-fees test (negative): Automatically fails if the majority of compensation for any party performing the activity is tied to contributions raised, for example, a commission-based fundraiser

- Separate-and-similar-activities test: Met if a similar program or management activity is conducted separately and without fundraising on a similar or greater scale

- Other-evidence test: A weight-of-evidence approach considering all positive and negative factors

The IRS and state regulators look at whether the program component has substance and is integral to the mission, not incidental to the fundraising ask. A superficial mention of the organization's work doesn't meet this standard.

Audience Test

Who received the communication matters as much as what it said. The audience test asks whether recipients were selected based on their need for the program message or their capacity to donate. If the audience includes prior donors or is selected based on financial ability to give, the criterion is generally not met and all costs are charged to fundraising.

Concrete illustrations:

- Fails: A mailing sent to a purchased donor prospect list selected for financial capacity

- Passes: A mailing sent to parents of students about drug-prevention education, selected based on program need rather than donor history

According to AICPA guidance, selecting the mailing list or campaign audience primarily based on wealth indicators, giving history, or donor scoring rather than connection to the program's intended beneficiary population is a clear failure.

Content Test

The content test requires the communication to include a specific "call to action" that motivates the recipient to take a program-related step beyond simply donating, such as visiting a clinic, calling a helpline, or changing a behavior relevant to the mission.

What does NOT qualify:

- Describing the organization's work or expressing gratitude

- Asking recipients to "visit a website for more information"

- Generic mission statements or awareness-raising content

What DOES qualify:

- Signing and returning a petition

- Seeing a doctor for specific disease warning signs

- Adopting a pet from a shelter

- Calling a crisis hotline for immediate help

A genuine call to action must be actionable, mission-aligned, and directed at the audience's capacity to act. A mailer with multiple donation requests is not automatically disqualified if a credible program call to action exists, but the program component must have real weight. Regulators and auditors will look past the label to evaluate whether the content would genuinely motivate a behavior change independent of any gift request.

The Most Common Joint Cost Allocation Pitfalls

These are the mistakes that repeatedly appear in state enforcement actions and donor watchdog reports. Each represents a specific, avoidable error.

Pitfall 1: Allocating Without a Genuine Call to Action

Many nonprofits include a generic mission statement or program description in a fundraising appeal and treat this as a call to action. Regulators reject this approach. The call to action must be specific, actionable, and directly tied to the organization's charitable programs—not just awareness-raising.

What fails: "Learn more about our vital work helping homeless veterans by visiting our website."

What passes: "Call our hotline at 1-800-XXX-XXXX if you or a veteran you know needs immediate housing assistance."

The second example directs the recipient to take a concrete, mission-aligned action that delivers a program service. That's the standard regulators apply.

Pitfall 2: Over-Allocating to Program Expense

Organizations that disproportionately push joint costs into program expense end up with ratios that look misleadingly favorable. Charity watchdogs like CharityWatch actively flag this pattern—they typically remove joint costs from program expenses and reallocate them to fundraising when computing letter grades.

Separately, Charity Navigator considers 75% or higher program spending "highly efficient," while organizations below 50% earn zero points in its rating system.

The stakes are real. The National Veterans Foundation case revealed a gap of nearly $6.8 million between reported and actual program spending in a single year. When regulators force reclassification, reported efficiency can drop from 70–80% program spending to under 15%.

Pitfall 3: Audience Selection Based on Donor Potential

Selecting the mailing list or campaign audience primarily based on wealth indicators, giving history, or donor scoring—rather than connection to the program's intended beneficiary population—is one of the most common errors cited by state regulators.

Consider a "don't drink and drive" campaign sent to affluent neighborhoods where residents rarely consume alcohol but have high charitable giving capacity. That's a red flag. The same campaign sent to college students, young professionals, and communities with high alcohol consumption rates? That's compliant. Document your audience selection criteria before the campaign launches—not after.

Pitfall 4: Applying JCA to Activities That Are Purely Fundraising

Some nonprofits attempt to apply joint cost treatment to events, galas, or campaigns with no credible programmatic component. If any "program element" was added retroactively to justify the allocation, regulators will likely treat the entire cost as fundraising.

A gala dinner where organizers add a five-minute "educational presentation," then allocate 30–40% of event costs to program expense, is a typical example. Unless that educational component has genuine substance and would occur independent of the fundraising event, it fails the purpose test.

Pitfall 5: Inconsistent Application Across Periods

ASC 958-720-45 requires allocation methods to be applied consistently across similar activities. Switching methods from year to year—or applying JCA to some campaigns but not comparable ones—raises audit flags and undermines the credibility of your financial statements.

For example: allocating joint costs for a spring direct mail campaign using the physical units method, then switching to the relative direct cost method for a fall campaign with identical characteristics—without documented justification—is exactly the kind of inconsistency auditors flag.

How Regulators and Auditors Identify Red Flags

State attorneys general in California, New York, and Michigan, along with the IRS and nonprofit watchdog organizations like CharityWatch, all monitor nonprofit financial statements, Form 990 filings, and solicitation materials for signs of improper JCA.

Specific signals auditors look for:

- A sudden or dramatic shift in the program-to-fundraising expense ratio without corresponding operational changes

- JCA applied to broad donor acquisition campaigns sent to purchased prospect lists

- Vague disclosure language on Form 990 about the nature of the joint activity and the allocation method used

- Program expense ratios that appear unusually favorable compared to peer organizations

Multi-state enforcement pattern: New York, Michigan, and California have brought enforcement actions alleging that incorrect allocation of joint costs resulted in "materially false statements" in financial documents submitted for state charitable solicitation registration. Regulators view improper JCA use as a "deceptive fundraising practice" that violates state charitable solicitation laws.

When a nonprofit's reported fundraising cost percentage appears unusually low relative to peers, it draws scrutiny from both regulators and donors consulting charity rating sites. BBB Wise Giving Alliance Standard 13 specifies that when more than 50% of an organization's joint costs are allocated to program services, it triggers a request for additional documentation.

Watchdog flags carry real consequences. CharityWatch adjusts ratings for questionable joint cost allocation, dropping an organization's letter grade from A to C or lower based solely on JCA practices — a reputational hit that can affect donor trust as directly as a regulatory inquiry.

Best Practices for Compliant Joint Cost Allocation

Proper JCA starts with a written policy that defines the organization's criteria for determining when a joint activity qualifies, which allocation method will be used, and who is responsible for making and documenting that determination each reporting period.

Acceptable allocation methods include:

- Physical units method: Costs allocated based on units of output (e.g., number of lines, square inches, or pages devoted to each function)

- Relative direct cost method: Uses the ratio of direct costs of each component to allocate remaining indirect/joint costs

- Stand-alone price method: Determines proportions based on what each component would have cost if conducted independently

ASC 958-720 does not mandate a specific method but requires methodology to be rational, systematic, reasonable, and applied consistently. Whatever method you choose must be documented and used for all similar activities.

Document Before the Campaign Launches

Contemporaneous documentation is non-negotiable—before a campaign launches, not after. Organizations should document:

- Why they believe each of the three tests is met

- How they selected the audience

- What the specific call to action is

- How costs were actually allocated

Keep this documentation in audit-ready form. The IRS Form 990 Instructions explicitly state: "Any method of allocating joint costs must be reasonable under the facts and circumstances of each case."

Form 990 Reporting Requirements

Joint costs must be disclosed in the notes to financial statements and on Form 990, Part IX (Statement of Functional Expenses), Line 26. Organizations must:

- Report total joint costs in Column (A)

- Show how much was allocated to program services in Column (B)

- Show how much was allocated to fundraising in Column (D)

- Check the box only if the organization followed SOP 98-2 / ASC 958-720

- Include a description of the activities and allocation method used

Vague disclosures draw auditor questions. Be specific about the nature of the joint activity and the rationale for your allocation method.

The Role of Fractional Financial Leadership

Experienced nonprofit financial leadership—whether in-house or fractional—reduces audit risk by catching allocation errors before they reach the 990. A fractional CFO can establish JCA policies, review campaigns prior to cost allocation, and ensure disclosures hold up under scrutiny. One Abacus Advisory provides this kind of hands-on oversight, working directly with nonprofit boards and executive directors on compliance-sensitive reporting like JCA.

Frequently Asked Questions

What exactly counts as a "call to action" for joint cost allocation purposes?

A genuine call to action is a specific, actionable step that advances the nonprofit's mission and is directed at the recipient's capacity to act—such as "call this hotline," "get tested," or "use this resource." Mere mission description, expressions of gratitude, or invitations to "learn more" do not qualify under ASC 958-720-45.

Can a nonprofit use any allocation method it wants when splitting joint costs?

ASC 958-720-45 does not mandate a specific method but requires the chosen approach to be reasonable, well-documented, and applied consistently across similar activities and reporting periods.

How are joint costs disclosed on IRS Form 990?

Joint costs appear in the Statement of Functional Expenses (Part IX, Line 26) and must be disclosed with a description of the activities and the allocation method used. Organizations report total joint costs in Column (A), program allocation in Column (B), and fundraising allocation in Column (D). Inadequate disclosure is a red flag for auditors.

What happens if a nonprofit fails the three tests but allocated costs to program anyway?

The organization may face state enforcement action for filing materially false financial statements in charitable solicitation filings, IRS scrutiny during audits, and damage to donor trust if flagged by charity watchdog organizations like CharityWatch or Charity Navigator—potentially resulting in downgraded ratings.

Does joint cost allocation apply to digital fundraising campaigns, not just direct mail?

Yes. JCA applies to any solicitation activity—including email, social media, podcasts, YouTube, and digital advertising—as long as the same three tests (purpose, audience, content) are met. The 2025 IRS Form 990 instructions confirm that a combined educational campaign and fundraising solicitation occurs "by mail, telephone, broadcast media, or any other means."

How often should a nonprofit review its joint cost allocation policy?

Review the policy at least annually, before major campaigns, and whenever programs or fundraising activities change materially. Boards should treat this as part of their financial oversight responsibilities—not a one-time administrative task.