Introduction

For nonprofits, missing a single Form 990 deadline isn't just an administrative oversight—daily penalties start accruing. Organizations with gross receipts under $1,309,500 face $25 per day, capped at $13,000 or 5% of gross receipts (whichever is less), while larger nonprofits face $130 per day, up to $65,000. Before most boards realize what's happened, penalties can reach tens of thousands of dollars.

This article covers IRS penalty calculations, key deadlines and extensions, common compliance failures, the risk of automatic revocation, and how to pursue penalty abatement or avoid penalties altogether.

TLDR:

- Nonprofits face daily penalties of $25 to $130 for late or incomplete Form 990 filings, with caps ranging from $13,000 to $65,000

- Missing three consecutive annual filings triggers automatic revocation of tax-exempt status with no warning letter

- File Form 8868 before your original deadline to get an automatic 6-month extension

- Penalty abatement requires documented reasonable cause; first-time penalty relief is not available to nonprofits

- A compliance calendar and dedicated financial oversight close the knowledge gaps that cause most late filings

How the IRS Calculates Late Filing Penalties for Nonprofits

Penalty Tiers Based on Gross Receipts

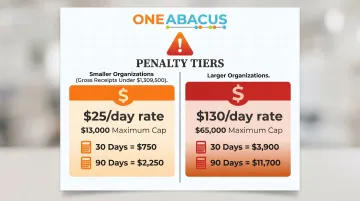

The IRS uses a two-tier penalty structure that scales with organization size. For returns required to be filed in 2026, organizations with gross receipts under $1,309,500 are charged $25 per day, with a maximum penalty capped at the lesser of $13,000 or 5% of gross receipts. Organizations exceeding the threshold face $130 per day, up to a maximum of $65,000.

These amounts reflect recent inflation adjustments under Rev. Proc. 2024-40. Organizations filing 2025 calendar-year returns face the previous rates: $20/day (max $12,000) for smaller organizations and $120/day (max $60,000) for larger ones, with a $1,208,500 gross receipts threshold.

How penalties accumulate:

- A 30-day delay costs a small nonprofit $750 (at $25/day)

- The same delay costs a larger organization $3,900 (at $130/day)

- A 90-day delay puts a small nonprofit at $2,250, still well below the cap

- A 90-day delay costs a larger organization $11,700—approaching 20% of the maximum penalty

A 90-day delay is one missed quarter. At the larger organization rate, that's nearly $12,000 before any abatement requests, compliance letters, or responsible person penalties enter the picture.

The Incomplete Return Trap

The IRS makes clear that penalties apply not only to late filing but also to returns filed with incomplete or incorrect information. Submitting an inaccurate Form 990 carries the same daily consequences as filing nothing at all.

The IRS does not consider a return "filed" until it receives a version that is complete and accurate. Common mistakes that trigger this penalty include:

- Missing schedules (Schedule A for 501(c)(3) organizations, Schedule L for loans/transactions with interested persons)

- Incomplete financial statements or unsupported revenue/expense figures

- Unsigned returns or missing signatures from required officers

- Incorrect classification of activities or programs

Key takeaway: Filing something incomplete by the deadline doesn't stop the penalty clock. The clock stops when the IRS receives a complete, accurate return — not when you submit.

Which Forms Are Subject to Late Filing Penalties

Forms that trigger monetary penalties:

- Form 990 (Return of Organization Exempt From Income Tax)

- Form 990-EZ (Short Form Return)

- Form 990-PF (Return of Private Foundation)

All three are governed by IRC 6652(c) and subject to the tiered daily penalty structure described above.

Form 990-N (e-Postcard) is different: The National Council of Nonprofits confirms that the 990-N carries no monetary penalty for lateness. However, the form's due date cannot be extended, and three consecutive missed filings still trigger automatic revocation of tax-exempt status — the same status revocation risk as organizations filing full 990s.

The Responsible Person Penalty

Form type determines the compliance letter the IRS sends: Letter 2694C for Form 990, Letter 2695C for Form 990-EZ, and Letter 2696C for missing information. Under IRC 6652(c)(1)(B), once any of these letters is issued, the organization has 10 days to respond with a corrected or complete return.

After that deadline, individual officers or directors responsible for the filing can be personally charged $10 per day, up to $6,500 per return. This penalty is separate from the organizational penalty and creates personal financial exposure for board members and executive directors.

The IRS actively assesses responsible person penalties when organizations ignore compliance letters — this isn't an obscure provision. For small nonprofits with limited organizational penalty exposure, the personal liability can approach or exceed the organizational fine.

Form 990 Deadlines and the Extension Option

Standard due date: Form 990, 990-EZ, and 990-N are due on the 15th day of the 5th month after the end of the organization's fiscal year. For calendar-year organizations, that's May 15.

Automatic 6-month extension: Nonprofits can file Form 8868 to receive an automatic extension, pushing the deadline to November 15 for calendar-year filers. The extension request must be submitted before the original deadline.

What the extension covers (and what it doesn't):

- ✅ Extends the filing deadline by six months

- ✅ Stops daily penalties from accruing during the extension period

- ❌ Does not extend any tax payment obligations (if the organization has unrelated business income tax due, payment is still due by the original deadline)

- ❌ Does not apply to Form 990-N (the e-Postcard cannot be extended)

Extensions are widely used and fully legitimate. That said, an incomplete extension request or a missed extended deadline still triggers the full penalty structure calculated from the original due date—so filing Form 8868 on time matters just as much as filing Form 990 on time.

Why Nonprofits Miss the Filing Deadline

Staff Turnover and Single Points of Failure

When the one person who manages compliance departs, institutional knowledge walks out the door. The remaining team may not know what forms to file, when they're due, or where previous years' supporting documentation is stored.

This structural vulnerability is especially acute in lean nonprofit teams where compliance responsibilities aren't formally distributed. One Abacus Advisory has seen this firsthand. During a leadership transition at the Philadelphia Zoo, both the CFO and Controller departed simultaneously, creating a critical knowledge gap that required immediate external support to maintain filing readiness.

Common Misconceptions That Lead to Non-Filing

Many nonprofits mistakenly believe they don't need to file if:

- The organization had no revenue or activity during the year

- They're too small to matter

- They already file state-level reports

- They're exempt from federal income tax

The reality: Most tax-exempt organizations must file annually regardless of financial activity. The IRS requires Form 990 or 990-N for virtually all 501(c) organizations with few exceptions. Confusion between federal and state filing obligations is one of the most common causes of non-compliance.

Disorganized or Delayed Record-Keeping

When financial data isn't reconciled regularly or is spread across informal systems managed by volunteers, pulling accurate figures together for the 990 becomes a last-minute scramble. This frequently results in:

- Missed deadlines due to incomplete financial statements

- Errors that trigger the incomplete return penalty

- Rushed filings with insufficient supporting documentation

Organizations that wait until April to compile year-end financial data are setting themselves up for delays, errors, or both.

Monthly reconciliations and a chart of accounts aligned with Form 990 categories reduce preparation time and cut error risk — two changes that make a measurable difference at filing time.

The Bigger Risk: Automatic Revocation of Tax-Exempt Status

The Three-Year Rule

An exempt organization that fails to file a required annual return or Form 990-N for three consecutive tax years automatically loses its federal tax-exempt status under IRC 6033(j). No warning letter is issued before revocation takes effect.

This is not an IRS determination—it's automatic revocation by operation of law. The IRS cannot undo a proper automatic revocation, and there is no appeal process.

Financial Consequences of Revocation

Once tax-exempt status is lost:

- The organization becomes subject to federal income tax on its revenues

- State income and property tax exemptions may be lost

- Donors can no longer claim charitable deductions for contributions, directly undermining fundraising capacity

- The organization is publicly listed on the IRS Auto-Revocation List, visible to all donors, grantmakers, and the public

Grant and Reputational Impact

The fundraising damage extends beyond individual donors. Most foundations, government agencies, and corporate grant programs require active tax-exempt status as a condition of funding — a nonprofit whose status has been revoked becomes ineligible for most grants immediately.

The compliance history is permanently visible through the IRS Tax Exempt Organization Search database. Even after reinstatement, the revocation remains on the public record.

The Revocation Data: 1.2 Million Organizations Lost

Analysis of IRS data by Palavir LLC shows 1,203,394 nonprofits have lost tax-exempt status through automatic revocation from 2010 through March 2025. The peak year was 2010 with 377,410 revocations—the first mass enforcement of the Pension Protection Act provision. Post-2010, revocations stabilized at approximately 35,000 to 65,000 per year.

Of all revocations, 65.8% were 501(c)(3) organizations (792,082 total). California led states with 135,529 revocations.

Reinstatement: Why Prevention Matters More Than Recovery

The organization must:

- File all missing returns for the three consecutive years that caused revocation

- Pay all accumulated penalties

- Submit a new exemption application (Form 1023, 1023-EZ, 1024, or 1024-A) with the appropriate user fee

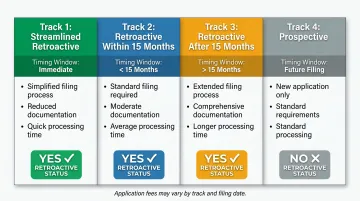

Rev. Proc. 2014-11 governs reinstatement with four tracks:

| Track | Timing | Requirements | Retroactive? |

|---|---|---|---|

| Streamlined Retroactive | Within 15 months | Eligible for 990-EZ/990-N; no prior revocation | Yes |

| Retroactive (within 15 months) | Within 15 months | Reasonable cause for ≥1 year; file delinquent returns | Yes |

| Retroactive (after 15 months) | After 15 months | Reasonable cause for all 3 years; file delinquent returns | Yes |

| Post-Mark Date (Prospective) | Any time | No cause statement required | No |

Reinstatement requires paying a new application fee ($275–$600), filing years of delinquent returns, and waiting months for IRS review — with no guarantee of approval. Throughout that window, the organization remains taxable and locked out of grant funding. A single missed filing cycle is far easier to correct than three years of compounding consequences.

How to Request IRS Penalty Abatement

What Is Penalty Abatement?

The IRS may reduce or eliminate late filing penalties when an organization demonstrates reasonable cause for the failure. This means the organization acted with ordinary business care and prudence but was still unable to comply.

Abatement is not automatic and must be formally requested with documentation. The burden of proof is entirely on the organization.

Circumstances That Typically Qualify as Reasonable Cause

The IRS recognizes these situations as potentially meeting the reasonable cause standard:

- Natural disasters or declared emergencies that prevented access to records or disrupted operations

- Death, serious illness, or unavoidable absence of the person solely responsible for filing, with no backup in place

- Documented IRS system failures or electronic filing rejections that occurred near the deadline and prevented timely submission

Each circumstance requires contemporaneous documentation—medical records, disaster declarations, IRS system error messages with timestamps, etc.

What Does NOT Qualify for Abatement

The IRS consistently rejects these explanations:

- Using a paid tax preparer does not transfer responsibility — the organization is still liable for filing on time

- Claiming ignorance of filing requirements carries no weight; nonprofits are expected to know their obligations

- Financial hardship excuses inability to pay, not failure to file

- Heavy workload or staff shortages are treated as normal operational challenges, not reasonable cause

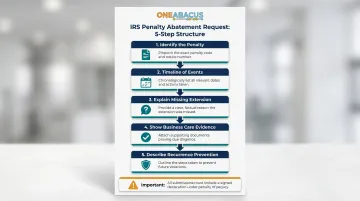

Proper Structure of an Abatement Request

Submit a written statement (under penalty of perjury) attached to or accompanying the filed Form 990. The IRS specifies the statement must address:

- Identify the specific penalty being contested — include the date assessed, dollar amount, and penalty type

- Lay out a clear timeline of what prevented compliance, with specific dates and events

- Explain why no extension was requested, if that applies to your situation

- Show evidence of ordinary business care — what the organization actually did to try to comply

- Describe steps taken to prevent recurrence, such as new filing systems or internal controls

Include all supporting documentation: medical records, disaster declarations, correspondence with the IRS, system error screenshots, etc.

Critical note: First-Time Penalty Abatement (FTA) does NOT apply to Form 990 penalties under IRC 6652(c). The IRS Internal Revenue Manual explicitly excludes these penalties from the FTA program. Only reasonable cause abatement is available.

When to Engage a Professional

Consider consulting a CPA or tax attorney with nonprofit compliance experience for:

- Multi-year penalties

- Combined penalty types (late filing + incomplete return + responsible person penalties)

- Total penalty amounts exceeding $10,000 or representing more than 5% of annual operating budget

- Previous unsuccessful abatement requests

In these situations, a professional can draft a stronger written argument, anticipate IRS objections, and navigate the appeals process if the initial request is denied.

How to Prevent Late Filing Penalties Going Forward

Build a Compliance Calendar with Layered Reminders

Map every annual filing obligation—Form 990, state registrations, employment tax returns—and set alerts at 90, 60, 30, and 7 days before each deadline. This ensures that gathering documents, correcting records, and filing all happen with time to spare.

- Document who is responsible for each task

- Designate a backup for every compliance responsibility

- Include extension filing deadlines on the calendar (Form 8868 must be filed before the original due date)

- Review and update the calendar annually after fiscal year-end

Maintain Financial Records Throughout the Year

Monthly reconciliations rather than year-end compilation dramatically reduce preparation time and error risk. Standardized bookkeeping practices include:

- A well-structured chart of accounts aligned with Form 990 categories

- Regular document digitization (receipts, contracts, grant agreements)

- Consistent categorization of revenue and expenses

- Monthly financial statement close process

Organizations that reconcile monthly can generate a draft Form 990 in days rather than weeks.

How Fractional Financial Leadership Closes the Gap

Many nonprofits rely on a single staff member to manage compliance calendars, financial records, and filing deadlines. When that person leaves, the institutional knowledge goes with them. Fractional financial leadership addresses this directly by embedding ongoing oversight into the organization's structure rather than into any one employee.

When the Philadelphia Zoo lost both its CFO and Controller simultaneously, One Abacus Advisory stepped in with fractional CFO and Controller support to maintain uninterrupted operations. The team optimized the Zoo's NetSuite environment, improved month-end close and board reporting, and kept all regulatory filings on track through the transition.

One Abacus Advisory's Accounting Optimization service focuses on strengthening financial systems, improving reporting accuracy, and maintaining regulatory compliance—targeting the root causes that lead to late filings in the first place. For nonprofits that can't justify a full-time CFO hire, this model delivers the same compliance rigor at a fraction of the cost.

Frequently Asked Questions

What is the late filing penalty for a 501(c)(3)?

For returns filed in 2026, organizations with gross receipts under $1,309,500 face $25 per day (max $13,000 or 5% of gross receipts, whichever is less). Larger organizations face $130 per day (max $65,000). The same rates apply to incomplete or inaccurate returns.

Can a nonprofit lose its tax-exempt status for filing Form 990 late?

A single late filing triggers penalties but not revocation. However, failing to file for three consecutive years results in automatic revocation of tax-exempt status under federal law, with no warning letter issued beforehand.

How do I request penalty abatement from the IRS for a late Form 990?

Submit a written statement demonstrating reasonable cause, attached to the completed Form 990. Include a timeline of events, supporting documentation (such as medical records, disaster declarations, or IRS error messages), and a signed declaration under penalty of perjury.

What counts as reasonable cause for a late Form 990?

Qualifying circumstances include natural disasters, death or serious illness of the person solely responsible for filing, and documented IRS system failures. Ignorance of filing requirements, reliance on a preparer, and financial hardship do not qualify.

Can I get an extension on my Form 990 filing deadline?

Yes. File Form 8868 before the original due date to receive an automatic 6-month extension. The extension covers filing only—not any associated tax payments. Form 990-N (e-Postcard) cannot be extended.

What happens if a nonprofit has never filed a Form 990?

Unfiled returns accumulate daily penalties for each year required. Missing three consecutive years triggers automatic revocation, and reinstatement requires filing all delinquent returns, paying penalties, and submitting a new exemption application to the IRS.

IRS late filing penalties for nonprofits are immediate and escalating—but the bigger risk is automatic revocation after three consecutive years of non-filing. Compliance calendars, monthly financial reconciliations, and dedicated financial oversight close the single-person knowledge gaps that cause most late filings. Treat Form 990 as a year-round operational discipline, and revocation risk drops to near zero.

For nonprofits seeking ongoing compliance oversight and filing readiness support, schedule a free consultation with One Abacus Advisory to discuss fractional CFO and senior finance services tailored to your organization's needs.