Introduction

Nonprofit leaders launch and lead organizations because of a compelling mission — to fight hunger, protect wildlife, advance education, or serve their communities. Yet no matter how passionate the purpose, strong financial management is what keeps the mission alive. Without it, even the most well-intentioned organizations risk compliance violations, donor distrust, operational chaos, and in the worst cases, loss of tax-exempt status.

Nonprofit accounting follows distinct rules that differ from for-profit practices. FASB Topic 958, Generally Accepted Accounting Principles (GAAP), and IRS Form 990 create a regulatory framework that demands specialized knowledge. Mismanaging these requirements can cost an organization its credibility and its legal standing.

The stakes are real. According to the Nonprofit Finance Fund's 2025 survey, 36% of nonprofits ended 2024 with an operating deficit — the highest rate in 10 years — and 52% hold three months or less cash on hand. Sound financial practices are what separate organizations that weather these pressures from those that don't.

This guide covers the fundamentals every nonprofit leader and board member should understand: key differences from for-profit accounting, essential financial documents, fund accounting mechanics, compliance obligations, and proven practices for long-term financial health.

Key Takeaways

- Nonprofit accounting follows FASB Topic 958 and GAAP, prioritizing accountability over profit

- Net assets are classified as with or without donor restrictions under ASU 2016-14

- Four core financial statements — Statement of Financial Position, Statement of Activities, Statement of Cash Flows, and Statement of Functional Expenses — form the reporting foundation

- Fund accounting keeps restricted and unrestricted dollars separate, protecting donor intent

- Internal controls and accurate overhead allocation are what auditors, funders, and boards rely on

What Makes Nonprofit Accounting Different?

Nonprofit and for-profit accounting share foundational mechanics — double-entry bookkeeping, accrual basis principles, and detailed transaction recording. The fundamental purpose, however, diverges sharply: for-profit accounting tracks returns to owners, while nonprofit accounting demonstrates stewardship of public trust.

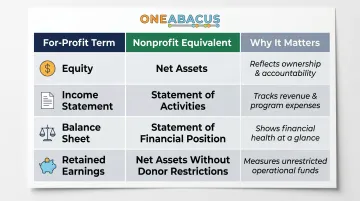

This philosophical difference shapes every aspect of financial reporting. Where a business reports "equity," a nonprofit reports "net assets." A for-profit income statement becomes a "Statement of Activities." The balance sheet is formally called the "Statement of Financial Position." Per FASB ASC 958-205-45-4, these aren't stylistic choices — they're authoritative GAAP requirements.

Terminology Translation

| For-Profit Term | Nonprofit Equivalent | Why It Matters |

|---|---|---|

| Equity | Net Assets | Reflects mission focus, not ownership |

| Income Statement | Statement of Activities | Organized by donor restriction status |

| Balance Sheet | Statement of Financial Position | Emphasizes financial health, not liquidation value |

| Retained Earnings | Net Assets Without Donor Restrictions | Shows flexible resources available |

These structural differences also clarify why nonprofits need two distinct financial functions working in tandem. Bookkeeping handles day-to-day transaction recording — entering donations, paying invoices, reconciling bank statements. Accounting goes further: analysis, compliance oversight, financial reporting, and strategic interpretation.

Many small organizations start with a volunteer bookkeeper. As revenue grows and grant compliance intensifies, professional accounting becomes essential — not optional.

Core Financial Documents Every Nonprofit Needs

Most nonprofit leaders know they need financial statements — but knowing which documents matter, and why, shapes how well your board governs and how confidently you pursue funding. These five documents form the foundation of nonprofit financial accountability.

Statement of Financial Position

Unlike for-profit balance sheets that report "equity," the Statement of Financial Position lists assets, liabilities, and net assets at a specific point in time — answering the fundamental question: What does the organization own, owe, and control?

Net assets are split by restriction status:

- Net assets without donor restrictions (unrestricted)

- Net assets with donor restrictions (temporarily or permanently restricted)

That split isn't just an accounting formality. It tells you exactly how much of your resources you can deploy today versus funds already committed to a donor's designated purpose.

Statement of Activities

The Statement of Activities summarizes revenues, expenses, gains, losses, and changes in net assets over a reporting period. It functions like an income statement but organizes information by net asset class.

Key uses:

- Tracking program revenue vs. expenses

- Comparing budget to actual performance

- Demonstrating mission spending to donors and boards

- Supporting grant applications and funder reports

Statement of Cash Flows

Cash flow statements are especially critical for nonprofits managing grant cycles, seasonal revenue, or capital projects — and they reveal something the Statement of Activities cannot. An organization can show a surplus while facing a genuine cash crisis if grant reimbursements arrive weeks after payroll is due. The Statement of Cash Flows exposes those timing mismatches between revenue recognition and actual cash receipts across operating, investing, and financing activities.

Statement of Functional Expenses

This is the one financial statement unique to nonprofits. ASU 2016-14 requires all nonprofits to report expenses by both nature (salaries, rent, supplies) and function (program, management/general, fundraising).

Reporting expenses both ways enables:

- Transparency into how much the organization spends on mission vs. overhead

- Compliance with Form 990 reporting requirements

- Evaluation by charity watchdogs like Charity Navigator

For example, Charity Navigator's rating methodology awards full credit when medium and large donor-funded organizations spend 85% or more on programs; smaller organizations need 70% or more.

Chart of Accounts (COA)

The Chart of Accounts structures every transaction into logical categories — assets, liabilities, net assets, revenue, and expenses — and determines how cleanly all four statements above come together at reporting time.

A well-designed COA:

- Enables accurate grant tracking

- Simplifies audit preparation

- Supports functional expense allocation

- Makes financial reporting faster and more reliable

Fund Accounting: The Foundation of Nonprofit Finances

Fund accounting is the practice of segregating financial resources into separate "funds" based on donor restrictions or intended use. This is what most clearly differentiates nonprofit accounting from business accounting.

Two Net Asset Classifications Under ASU 2016-14

ASU 2016-14 simplified net asset classifications from three categories to two, effective for fiscal years beginning after December 15, 2017:

Net assets without donor restrictions (unrestricted funds):

- Flexible use for any organizational need

- Board-designated funds fall into this category

- May be used for overhead, programs, or reserves

Net assets with donor restrictions:

- Time or purpose restrictions: designated for specific projects, time periods, or purposes; released when conditions are met

- Perpetual restrictions (endowments): the principal must be maintained in perpetuity; only investment income is available for spending

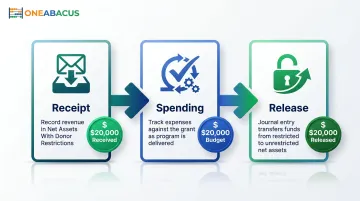

Practical Example: Tracking a Restricted Grant

A foundation awards your nonprofit $20,000 for youth programming. Here's how fund accounting works:

- Receipt: Record $20,000 as revenue in "Net Assets With Donor Restrictions"

- Spending: As you deliver the youth program and incur expenses, track those costs against the grant

- Release: When the program is complete, create a journal entry to "release from restrictions" — transferring the $20,000 from restricted to unrestricted net assets on the Statement of Activities

Per Propel Nonprofits, "When the time or purpose restriction has been met, a journal entry is made to transfer funds from the With Donor Restrictions column to the Without Donor Restrictions column using the 'release from restrictions' line item."

Risk of Commingling Funds

If restricted and unrestricted funds aren't properly separated in your accounting system, you may inadvertently spend donor-designated money on overhead or unrelated programs. This creates:

- Compliance violations that can trigger IRS scrutiny

- Donor trust issues that damage fundraising credibility

- Board fiduciary liability for misuse of restricted assets

- Potential loss of tax-exempt status if the IRS discovers systemic mismanagement

Beyond compliance risks, fund commingling distorts financial reporting. Without proper tracking, your income statement may show inflated surpluses in year one of a multi-year grant, followed by artificial deficits in subsequent years.

Impact on Overhead Ratios and Public Ratings

Proper fund accounting directly informs the overhead ratio visible to donors and watchdog organizations. Charity Navigator evaluates nonprofits on program expense ratios, fundraising efficiency, and working capital. Accurate functional expense allocation, which depends on sound fund accounting, determines your public rating and donor confidence.

Compliance Requirements: Form 990, GAAP, and State Filings

GAAP for Nonprofits

Generally Accepted Accounting Principles (GAAP) as codified by the Financial Accounting Standards Board (FASB) govern nonprofit financial reporting. Specifically, FASB ASC 958 provides the official accounting standards for recognizing, measuring, presenting, and disclosing contributions, net assets, and nonprofit-specific transactions.

ASU 2016-14 represents the most significant update to nonprofit financial reporting in over 20 years, addressing:

- Net asset classification (two classes instead of three)

- Functional expense reporting requirements

- Liquidity disclosures to show available resources

- Enhanced transparency for donor and board decision-making

GAAP compliance is expected by auditors, grant-makers, major donors, and regulators. Nonprofits that fail to follow GAAP risk audit qualifications, grant disqualifications, and reputational damage.

IRS Form 990 Requirements

Form 990 is the annual information return required of tax-exempt organizations. The filing deadline is the 15th day of the 5th month after fiscal year-end — May 15 for calendar-year filers.

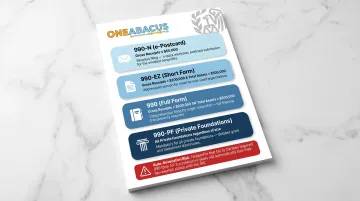

Form 990 variants by size:

| Form | Eligibility |

|---|---|

| 990-N (e-Postcard) | Gross receipts normally $50,000 or less |

| 990-EZ | Gross receipts under $200,000 AND total assets under $500,000 |

| 990 (full) | Gross receipts $200,000+ OR total assets $500,000+ |

| 990-PF | Private foundations, regardless of size |

Critical: Three consecutive years of non-filing triggers automatic revocation of tax-exempt status. Since the initial mass revocation of approximately 275,000 organizations in 2011, the IRS has auto-revoked roughly 50,000 additional organizations per year. A compliance calendar with built-in reminders is the simplest way to keep this from happening to your organization.

Unrelated Business Taxable Income (UBTI)

Income from activities not substantially related to your nonprofit's exempt purpose may be taxable. The Tax Cuts and Jobs Act of 2017 requires each unrelated business activity to be accounted for separately — losses from one activity cannot offset income from another.

This "siloing" requirement has real consequences for organizations with multiple unrelated revenue streams:

- Each activity must be tracked and reported independently

- Losses in one activity cannot reduce taxable income in another

- Organizations may owe taxes even when their unrelated activities net to zero overall

State-Level Compliance

Approximately 40 states require charitable registration before soliciting donations. Many states have annual filing requirements beyond Form 990, with varying deadlines and formats. Falling out of good standing can restrict your fundraising activities, trigger fines, or cost you state-level tax exemptions — risks that compound quickly if multiple states are involved.

Audit Requirements

Organizations expending $1,000,000 or more in federal awards during their fiscal year must undergo a single audit under 2 CFR Part 200. The federal government recently raised this threshold from $750,000, providing some relief to mid-sized nonprofits.

Strong internal practices reduce audit friction significantly. Organizations with clean records, documented policies, and consistent fund tracking spend far less time — and money — getting through the process.

Best Practices for Nonprofit Financial Management

Implement Strong Internal Controls

Internal controls are your first line of defense against fraud, errors, and financial mismanagement. ACFE's 2020 Report to the Nations found that **35% of nonprofit fraud cases stemmed from a lack of internal controls**, with a median loss of $75,000 — potentially devastating for a small organization.

Essential controls include:

- Dual authorization on significant disbursements

- Separation of duties between cash handling and recordkeeping

- Monthly bank reconciliations performed by someone other than the bookkeeper

- Management review of financial reports and anomalies

- Anti-fraud training for staff and volunteers

Monitor Budget-to-Actual Performance

An operating budget only earns its value when leadership actively tracks performance against it. Nonprofits should compare actual revenues and expenses against budget monthly or quarterly — and understand variances before they become crises.

Regular financial monitoring enables:

- Early detection of revenue shortfalls

- Timely course corrections on overspending

- Informed program and staffing decisions

- Proactive communication with boards and funders

Build and Maintain Operating Reserves

The National Council of Nonprofits recommends nonprofits maintain 3 to 6 months of operating expenses as cash reserves. Yet NFF's 2025 survey found that 52% of nonprofits hold three months or less — well below that benchmark.

Operating reserves provide:

- A financial buffer during funding gaps or unexpected costs

- Flexibility to seize strategic opportunities

- Credibility with lenders, funders, and partners

- Stability during economic downturns or leadership transitions

When to Bring in Professional Financial Help

The Spectrum of Financial Staffing

A volunteer bookkeeper may suffice for a startup nonprofit with minimal transactions and no grant restrictions. But as organizations grow, the complexity of grant compliance, fund tracking, audit preparation, and financial reporting quickly exceeds volunteer capacity.

Professional financial leadership — either in-house or outsourced — becomes essential when:

- Revenue exceeds $500,000 annually

- The organization manages multiple restricted grants

- Leadership transitions create continuity risk

- Board members lack confidence in financial reports

- Audit findings indicate control weaknesses

The Fractional CFO Model

The fractional CFO model provides executive-level financial leadership without the cost of a full-time hire. For nonprofits with revenues under $10 million, it's a practical middle ground — access to experienced financial leadership without the overhead of a full-time hire.

Fractional CFO services typically include:

- Financial oversight and reporting

- Budget development and cash forecasting

- Audit preparation and compliance support

- Board presentations and governance support

- Financial planning aligned with organizational mission

That real-world application is where this model proves its value. One Abacus Advisory, for instance, has partnered with organizations like the San Diego Food Bank, Philadelphia Zoo, and Laguna Playhouse through periods of growth and leadership transition.

During the Philadelphia Zoo's CFO and Controller transition, One Abacus optimized their NetSuite environment, improved month-end close processes, and built stronger financial literacy across the executive team — outcomes that would have stalled without dedicated interim leadership.

The Value of Nonprofit-Specific Expertise

A financial professional who understands FASB Topic 958, fund accounting, Form 990 preparation, and grant compliance will be far more effective than a generalist. That depth of knowledge reduces compliance risk, shortens problem-solving cycles, and gives boards the clarity they need to make sound decisions.

Nonprofits benefit most when their financial advisors bring:

- Deep knowledge of nonprofit accounting standards

- Experience with grant management and compliance

- Proficiency in nonprofit accounting platforms (NetSuite, Sage Intacct, QuickBooks Online)

- Understanding of charity ratings and transparency expectations

- Ability to translate financial data into actionable insights

Frequently Asked Questions

What is the financial accounting for not-for-profit organisations?

Nonprofit financial accounting is the system for recording, classifying, and reporting an organization's financial activity in accordance with FASB Topic 958 and GAAP. It focuses on accountability and stewardship of donor contributions rather than profit maximization.

What accounting guidelines do nonprofit firms follow?

Nonprofits follow GAAP as set by FASB, specifically ASU 2016-14 (Topic 958), which governs net asset classification, functional expense reporting, and liquidity disclosures. They must also comply with IRS Form 990 filing requirements.

What are the 7 pillars of accounting?

The core principles of accounting include accuracy, consistency, transparency, going concern, matching, accrual basis, and accountability. For nonprofits, accountability carries particular weight — organizations must demonstrate that every dollar was spent according to donor intent and mission purpose.

What is fund accounting and why does it matter for nonprofits?

Fund accounting is the practice of segregating resources by donor restriction or purpose. It ensures nonprofits spend contributions as donors intended, which is essential for donor trust, regulatory compliance, and accurate financial reporting.

Do nonprofits need to file taxes?

While 501(c)(3) nonprofits are exempt from federal income tax, they must file Form 990 annually with the IRS. They may also have state filing obligations and must pay tax on unrelated business income exceeding certain thresholds.

What financial statements do nonprofits produce?

Nonprofits produce four core statements: Statement of Financial Position, Statement of Activities, Statement of Cash Flows, and Statement of Functional Expenses. Each differs in name and structure from for-profit equivalents, with the Statement of Functional Expenses being unique to nonprofits.