Introduction

Endowment accounting is the specialized process by which nonprofits record, classify, and report endowment funds in accordance with GAAP and UPMIFA. Unlike general operating fund accounting, it carries additional complexity: donor restrictions, long-term preservation requirements, and legal obligations that leave little room for error.

This guide is written for nonprofit finance staff, CFOs, executive directors, and board members who oversee endowment assets.

At the operational level, endowment accounting is frequently misunderstood. Many organizations hold endowment funds but struggle with how to record investment returns, appropriate spending correctly, or manage underwater funds when market values fall below original gift amounts.

With U.S. nonprofit endowment assets totaling approximately $1.7 trillion as of 2017, the scale of what's at stake makes compliance non-negotiable.

That accountability extends to donors: 75.9% say accurate expense reporting is "very important", and 54.6% are most confident giving when charities report expenses accurately. Proper endowment accounting directly shapes donor confidence, audit outcomes, and long-term institutional credibility.

Key Takeaways

- Donor-restricted endowments belong in net assets with donor restrictions; board-designated funds stay in net assets without donor restrictions

- UPMIFA (49 states) governs spending and management; ASC 958 (GAAP) controls how endowments appear in financial statements

- Most nonprofits spend 4–5% of rolling average endowment value annually to balance current needs with long-term preservation

- Underwater endowments trigger required disclosures and board-documented spending decisions

- Common pitfalls: misclassifying net assets, missing gift documentation, and informal appropriation practices

What Is Endowment Accounting?

Endowment accounting is the specialized branch of nonprofit accounting that governs how endowed gifts and their investment returns are received, classified, invested, spent, and disclosed. The goal is to honor donor intent while maintaining long-term financial sustainability.

Unlike general operating accounts, endowment accounting involves permanent or semi-permanent restrictions on principal, a separate spending policy, and ongoing UPMIFA compliance obligations. Investment returns flow through different net asset categories based on donor stipulations. Spending also requires formal board appropriation — not routine budget allocation.

How those rules apply depends on the type of endowment your organization holds.

Types of Endowments

Nonprofits may hold three types of endowments, each with distinct accounting implications:

True (Donor-Restricted) Endowment:

- Principal is permanently restricted and cannot be spent

- Governed by UPMIFA; classified as net assets with donor restrictions

- Investment returns may be restricted or unrestricted depending on the gift instrument

Board-Designated (Quasi) Endowment:

- Set aside by board action, not donor stipulation

- Classified as net assets without donor restrictions

- Board can redirect these funds at any time

- No legal restrictions, but should follow documented board policy

Term Endowment:

- Donor-imposed restrictions expire after a set time or triggering event

- Accounting treatment shifts from restricted to unrestricted once the condition is met

- Funds may then convert to a true endowment or become available for expenditure

Why Endowment Accounting Compliance Matters for Nonprofits

UPMIFA Establishes Legal Standards

UPMIFA was approved in July 2006 by the National Conference of Commissioners on Uniform State Laws and has been adopted in 49 U.S. states (all except Pennsylvania). It defines prudent investing and spending standards, requires disclosure of underwater endowments, and establishes fiduciary obligations. Noncompliance can trigger legal challenges and reputational damage.

GAAP Requires Clear Disclosure

ASC 958 mandates disclosure of endowment balances, net asset classification, spending policy, and underwater conditions. Auditors scrutinize these areas closely, and misclassification can result in audit findings or restated financials. Organizations using fund accounting systems like NetSuite can automate fund-level tracking and generate required disclosures more efficiently.

Financial Transparency Drives Donor Confidence

Accurate endowment reporting directly supports donor retention. Research shows that 75.9% of donors consider independent monitoring of spending "very important," and 54.6% are most confident giving when charities accurately report expenses. Proper accounting demonstrates stewardship and builds trust with stakeholders.

How Endowment Accounting Works: Classification and Recording

Endowment accounting moves through five distinct stages:

- Gift receipt and classification

- Principal investment

- Investment return recording

- Annual spending appropriation

- Financial statement disclosure

Each stage carries specific GAAP and UPMIFA requirements.

Net Asset Classification

Donor-restricted endowments must be reported as net assets with donor restrictions. Within this category, distinguish between:

- Permanent restrictions: Principal held in perpetuity

- Temporary restrictions: Earnings available for specific purposes until appropriated

Board-designated endowments stay in net assets without donor restrictions but should be tracked separately in internal records and disclosed in financial statement notes for governance clarity.

Recording Gifts and Investment Returns

Initial Gift Entry:

- Debit: Investment/cash account

- Credit: Net assets with donor restrictions (for donor-restricted endowments)

- Credit: Net assets without donor restrictions (for board-designated endowments)

Investment Returns: Investment returns—including unrealized gains, realized gains, interest, and dividends—must be classified based on donor intent:

- Some earnings remain restricted until formally appropriated

- Others may flow directly to unrestricted net assets if the gift instrument permits

- Returns on board-designated funds always remain unrestricted

Appropriating for Expenditure

Each year, the organization formally "appropriates" funds from the endowment per its spending policy. This is the critical accounting event that reclassifies amounts from net assets with donor restrictions to net assets without donor restrictions, making them available for program use.

Appropriation Entry:

- Debit: Net assets with donor restrictions

- Credit: Net assets without donor restrictions

This entry must be documented and authorized by the board or finance committee. Organizations without a formal appropriation process often find that establishing one is the single most important step toward endowment compliance — and a fractional CFO can help build that structure if internal capacity is limited.

Financial Statement Disclosure

Endowment-related disclosures must include:

- Rollforward schedule: Beginning and ending balances by type showing contributions, returns, appropriations, and other changes

- Net asset composition: Breakdown of donor-restricted vs. board-designated funds

- Investment and spending policies: Description of return objectives and appropriation methodology

- Underwater fund disclosure: Aggregate original gift amounts, current fair values, and deficiencies

- Board interpretation: How the organization interprets UPMIFA regarding spending from underwater funds

Platforms like NetSuite can automate fund-level tracking and generate these disclosures directly from your chart of accounts, cutting the time staff spend on manual year-end reconciliation.

Developing a Compliant Endowment Spending Policy

A written, board-approved spending policy is both a GAAP disclosure requirement and a UPMIFA compliance mechanism. Without one, your organization faces audit risk and has little defense against challenges over fund distribution.

The Rolling Average Approach

The most common spending method uses a fixed percentage (typically 3–5%) applied to the rolling average market value over the prior 3–5 years. Actual spending rates averaged 4.9% in FY25, up from 4.8% in FY24.

This "smoothing" mechanism buffers annual distributions from market swings, keeping budgets stable. Without it, a single down year can force cuts to programs that took years to build.

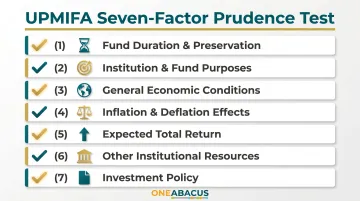

UPMIFA Seven-Factor Test

Every appropriation decision must be evaluated against these seven statutory factors:

- Duration and preservation of the fund

- Purposes of the institution and the endowment fund

- General economic conditions

- Possible effects of inflation or deflation

- Expected total return from income and appreciation

- Other resources of the institution

- The investment policy of the institution

These factors also set the context for UPMIFA's spending ceiling: distributions above 7% of average fair market value create a rebuttable presumption of imprudence under Section 4(d). That said, this provision is optional — not all states have adopted it — so boards should confirm whether their state enacted the threshold before relying on it as a safe harbor.

Underwater Endowment Spending

Spending from underwater endowments is permitted under UPMIFA but must be done prudently. Organizations should:

- Apply the seven-factor test with extra diligence

- Consider temporarily reducing appropriations

- Disclose underwater status in financial statements, including management's approach

- Document the board's prudence analysis in meeting minutes

Common Endowment Accounting Pitfalls to Avoid

Misclassifying Net Assets

Conflating donor-restricted and board-designated endowments is one of the most common and costly errors. It can result in reporting unrestricted assets as restricted (or vice versa), misleading the board and auditors. Each type requires different accounting treatment and cannot be reported in aggregate without clear disclosure.

Neglecting Fund-Level Documentation

Weak or missing gift instruments (the original donor agreements) make it impossible in practice to enforce donor intent. Organizations should maintain complete files for each endowment gift including:

- Gift agreement with original restrictions

- Original gift value for underwater comparison

- Any subsequent amendments or clarifications

- Board resolutions for board-designated funds

Failing to Identify Underwater Endowments

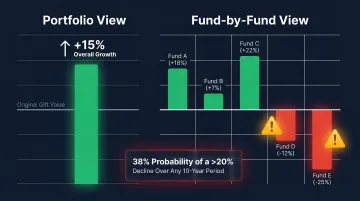

Many organizations discover underwater funds only at audit time. Underwater status must be assessed fund-by-fund, not just at the portfolio level—a portfolio can be up overall while individual funds are underwater. Market downturns are structural, not exceptional, with modeling showing a 38% probability of a greater-than-20% decline over any 10-year period.

Over-Relying on Informal Spending Practices

Some organizations distribute endowment earnings without a formal appropriation entry or board approval process. This creates a compliance gap and makes it difficult to distinguish operating income from endowment distributions.

Beyond identification and reporting issues, this is fundamentally a governance problem. Organizations that lack a formal spending policy—one that's documented, approved by the board, and applied consistently—are exposed at every audit. Fractional CFO support, such as what One Abacus Advisory provides to nonprofits, can help establish these processes without the overhead of a full-time hire.

Frequently Asked Questions

What is the 5% rule for nonprofit endowments?

The "5% rule" is a common spending benchmark—many nonprofits spend approximately 4–5% of their endowment's rolling average market value annually. This is not a legal mandate but a widely adopted best practice that balances current distributions with long-term principal preservation under UPMIFA. Note: The 5% minimum distribution requirement under IRC Section 4942 applies only to private foundations, not public charities.

What is the 120 rule for endowments?

No authoritative nonprofit accounting, legal, or regulatory source defines a "120 rule" specific to endowment management. The term appears to originate from personal finance, where "120 minus your age" is used for equity allocation. This is not recognized in UPMIFA, IRS regulations, or GAAP nonprofit endowment literature.

What is an endowment fund in a charity?

An endowment fund in a charity is a pool of donated assets invested for the long term, where the principal is typically preserved in perpetuity and only the investment returns (or a set percentage of total value) are used to support the charity's programs or operations.

What is the difference between a true endowment and a quasi-endowment?

A true endowment is created by a donor requiring the principal be held permanently (legally restricted under UPMIFA), reported as net assets with donor restrictions. A quasi-endowment is set aside by board decision and can be redesignated or spent at the board's discretion, reported as net assets without donor restrictions.

How are endowment funds classified on a nonprofit's balance sheet?

Donor-restricted endowments are reported as net assets with donor restrictions; board-designated endowments are reported as net assets without donor restrictions (but should be disclosed separately in notes). Investment returns move between categories depending on donor intent and the appropriation process. Under ASU 2016-14 (effective 2017), all nonprofits use this two-category classification system.

What happens when a nonprofit endowment goes underwater?

An underwater endowment occurs when the fund's current fair value falls below the original gift amount. Under UPMIFA, spending may continue but must be prudent and documented using the seven-factor test. The organization is required to disclose the underwater status in financial statements including aggregate original gift values, current fair values, and the deficiency amount.