Introduction

Picture this: your nonprofit receives 20 hours of pro-bono legal counsel from a board attorney who drafts critical vendor contracts, or a graphic designer donates a complete brand refresh worth thousands of dollars. Your development team celebrates the gift, your programs benefit from the expertise — but then your finance director asks a question that stops everyone in their tracks: Should we record this in our books, and if so, how?

This scenario plays out in nonprofits every day, and most organizations get it wrong. Contributed services follow specific rules under ASC 958-605, the GAAP standard governing nonprofit contribution accounting. Getting these entries wrong can trigger auditor findings, distort your program expense ratios, and erode donor trust when your reported numbers don't tell the full story.

This guide walks you through the recognition criteria that determine when to record contributed services, how to value them at fair market rates, and the journal entries required. It also covers disclosure rules that apply even when services don't qualify for recognition.

Whether you're preparing for an audit or want your financial statements to accurately reflect the true cost of delivering your mission, this guide gives you the framework to get it right.

Key Takeaways

- Contributed services must meet all three GAAP criteria: specialized skill required, provider has that skill, and the organization would otherwise pay for the service

- Qualifying services are recorded as a net-zero transaction — simultaneously debited to expense and credited to in-kind revenue at fair market value

- General volunteer labor and routine board governance duties are excluded from recognition

- Contributed services appear on GAAP financial statements but NOT on Form 990 — reconciliation is required on Part XI, Line 6

- Disclosure is required even for unrecognized services — notes must describe contributed services whether or not they're formally recorded

What Are Contributed Services in Nonprofit Accounting?

Contributed services are donated professional or specialized skills provided to a nonprofit at no charge by someone outside the organization who possesses those skills professionally. This includes services such as:

- Legal representation and contract review

- Medical or clinical consultations

- CPA-level accounting and audit services

- Architectural or engineering design

- Licensed construction or skilled trades work

- Graphic design, branding, or marketing by professionals

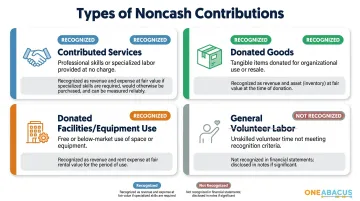

Nonprofits receive many types of noncash contributions, and each carries different accounting treatment:

| Type | Definition | Accounting Treatment |

|---|---|---|

| Contributed services | Specialized professional labor | Subject to three-criteria test; net-zero journal entry |

| Donated goods | Physical items (food, supplies, equipment) | Recorded as asset/expense and revenue; reported on Form 990 |

| Donated facilities/equipment use | Free or below-market rent, loaned vehicles | Valued at market rate differential; recorded if criteria met |

| General volunteer labor | Non-specialized time (event setup, mailings) | NOT recognized under GAAP; disclosed only |

This post focuses on contributed services specifically. Of the four categories above, this one involves the most judgment calls — particularly around the three-criteria test that determines whether recognition is required at all.

These services carry real economic value — costs your organization would otherwise pay out of pocket. GAAP requires recognition when the criteria are met because your financial statements should reflect the true cost of running programs and delivering services, not just cash expenditures.

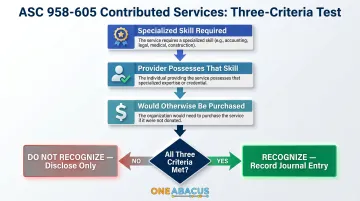

The Three GAAP Criteria for Recognizing Contributed Services

ASC 958-605 is the accounting standard that governs contribution accounting for nonprofits. Under it, contributed services must satisfy all three of the following criteria to be recognized as revenue and expense. If even one criterion fails, the service should NOT be recorded (though disclosure may still be required).

Criterion 1: Specialized Skill Required

The service must require a specialized skill — meaning it's not something any motivated volunteer could perform with general training.

Qualifying examples:

- An attorney drafting partnership agreements or reviewing legal compliance

- A CPA preparing audited financial statements or implementing internal controls

- A licensed contractor performing structural repairs or electrical work

- A physician providing clinical consultations or medical protocol review

- An architect designing facility renovations

Non-qualifying examples:

- Stuffing envelopes or preparing mailings

- Serving food at fundraising events

- Setting up chairs or managing event logistics

- General administrative assistance or data entry

The dividing line is simple: does the work require professional credentials, licensure, or technical expertise that most people don't have? If yes, it qualifies. If not, it doesn't.

Criterion 2: Provided by Someone Possessing That Skill

The person or organization performing the service must hold those skills as part of their professional role. A lawyer's credentials don't automatically qualify every service they provide.

Key distinction:

- An attorney donating legal advice → qualifies

- That same attorney volunteering to design your website → does NOT qualify

Even though they hold a professional license, the service has to fall within their area of actual expertise — not just their general identity as a credentialed professional.

Criterion 3: Would Otherwise Need to Be Purchased

Your organization must demonstrate that it would have purchased this service if it hadn't been donated. This is the practical "but-for" test.

How to apply this criterion:

- Review your budget — was this service line-itemed or planned for?

- Document that you sought quotes or researched market rates

- Note in your gift file that the service met an identified organizational need

- Confirm honestly that you would have paid for this — if not, it doesn't qualify

Example: If a board member offers pro-bono strategic consulting but your organization had no budget, no plan, and no intention to hire a consultant, the service should not be recorded — even if it's valuable.

That said, one important exception exists outside of these three criteria.

Exception for affiliated entities: If contributed services come from an affiliated organization — such as a parent entity providing shared HR or finance support — those services must be recorded even when the three criteria above are not met. These are treated as equity transfers (essentially internal resource movements between related entities) and measured at the affiliate's cost to provide the service, not fair market value.

How to Record Contributed Services: Step-by-Step

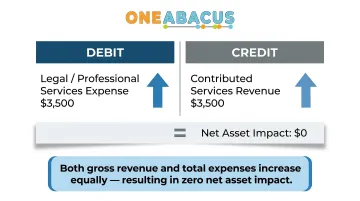

When all three GAAP criteria are met, contributed services are recorded as a net-zero journal entry — a simultaneous debit to the appropriate expense account and credit to in-kind contribution revenue.

Why it matters: This transaction does NOT change your cash position, but it does increase both gross revenue and total expenses on your Statement of Activities. This affects metrics like program expense ratios and provides transparency to funders who want to see the full economic cost of your programs.

Journal Entry Example

An attorney (board member acting outside normal board duties) donates 10 hours of contract review at a fair market rate of $350/hour.

| Account | Debit | Credit |

|---|---|---|

| Legal Expense (or Professional Services Expense) | $3,500 | |

| Contributed Services Revenue (unrestricted) | $3,500 |

Result: Your Statement of Activities shows $3,500 in additional revenue and $3,500 in additional expense. Net assets remain unchanged, but your reported activity accurately reflects the resources consumed.

The Board Member Exception

Many board members bring professional expertise, but services performed as part of normal governance duties do NOT qualify. This includes:

- Attending board meetings and committee meetings

- Reviewing financial statements in their fiduciary role

- Providing general business perspective or strategic input

- Voting on organizational matters

Work qualifies when it falls outside standard board responsibilities — performed at the organization's specific request using the member's professional expertise. For example:

- A board member who is an attorney drafting employment contracts for the organization

- A board member who is a CPA performing a financial statement audit (if the organization would otherwise hire an auditor)

- A board member who is a licensed contractor overseeing facility renovations

Document the distinction clearly: note that the service was requested, falls outside governance duties, and meets the three-criteria test.

Timing and Recognition

Two timing rules apply when recording these entries:

- Record at the time of service — not when promised. A lawyer's pledge to provide future legal work is not recognized until the work is actually performed.

- Measure value at the date of service — not at a historical or estimated future rate. If rates change between promise and delivery, use the rate in effect when the work occurs.

Because these entries increase both revenue and expenses without affecting cash, label them in internal reports so leadership can distinguish non-cash activity from operating results. Nonprofit finance advisors, including fractional CFOs at One Abacus Advisory, often build this communication into standard board reporting so directors understand what these transactions mean for program expense ratios and overall financial health.

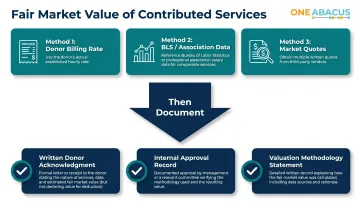

How to Value Contributed Services at Fair Market Value

Contributed services must be recorded at fair market value (FMV) at the time the service is provided. FMV is defined as what a willing buyer would pay a willing seller for the same service in the open market. Do not use internal cost estimates or discounted "nonprofit rates."

Practical Methods for Establishing FMV

1. Reference the donor's standard billing rate

Ask the professional for their typical fee schedule or hourly rate. Even if your organization could not afford that rate, the market rate is what you record. The exception: if the professional typically provides discounted rates to all nonprofits, use the discounted rate.

2. Consult publicly available rate data

Use authoritative sources to benchmark professional services:

- BLS Occupational Employment and Wage Statistics (OEWS): Covers approximately 830 occupations with state- and metro-level data. The May 2024 report shows a U.S. mean wage of $67,920 across all occupations.

- Professional association fee surveys: Many bar associations, medical societies, and accounting organizations publish rate surveys.

- Market research: Obtain quotes from 2-3 comparable providers in your region to establish a reasonable range.

One common misconception: the Independent Sector's volunteer time benchmark of $34.79 per hour (April 2025) covers general volunteer labor only. It does not apply to specialized professional services and should not be used for GAAP valuation purposes.

Documentation Requirements

Maintain supporting documentation for each contributed service recognized:

- Written acknowledgment from the donor confirming the service type, hours rendered, and their standard professional rate

- Internal approval or request confirming the organization solicited and would have purchased the service

- Valuation methodology explaining how FMV was established for each engagement

Proper documentation is required for audit purposes and to comply with ASU 2020-07's expanded disclosure rules. Capturing your valuation approach in your gift acceptance policy creates a repeatable standard that holds up under audit scrutiny.

Disclosure and Form 990 Reporting Requirements

One of the most confusing aspects of contributed services accounting is the GAAP vs. Form 990 divergence. These services appear in your audited financial statements but are explicitly excluded from Form 990. Understanding where they diverge — and how to document that gap — protects your organization at audit time.

GAAP vs. Form 990: The Reconciliation Challenge

Under GAAP, contributed services that meet the three recognition criteria appear as both revenue and expense on your Statement of Activities. Form 990 treats them differently — the IRS instructions explicitly state that donations of services are not contributions, even when GAAP requires you to record them.

This creates a reconciling difference you must address on:

- Form 990 Part XI (Reconciliation of Net Assets), Line 6: "Donated services and use of facilities"

- Schedule D Parts XI and XII: Reconciliation of Revenue and Expenses between GAAP statements and Form 990 reported amounts

Organizations with audited financial statements must explain these differences in Schedule D's narrative section.

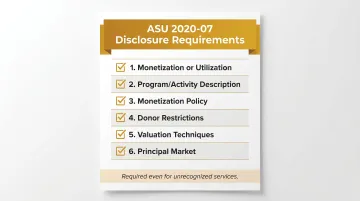

Disclosure Requirements Under ASU 2020-07

Even if contributed services do not meet the three GAAP recognition criteria, disclosure is still required in the notes to your financial statements. Skipping this step could trigger an audit finding.

ASU 2020-07 (effective for fiscal years beginning after June 15, 2021) expanded disclosure requirements for contributed nonfinancial assets, including services. Organizations must now provide:

Contributed services must appear as a distinct line item in the Statement of Activities, separate from cash contributions. Beyond that, six specific note disclosures are required for each category of contributed service:

| Disclosure | Description |

|---|---|

| 1. Monetization or utilization | Whether the services were monetized or used during the period |

| 2. Program/activity description | Which programs or activities utilized the services |

| 3. Monetization policy | Your policy (if any) about monetizing rather than utilizing services |

| 4. Donor restrictions | Any donor-imposed restrictions on the services |

| 5. Valuation techniques | How FMV was determined, including inputs per ASC Topic 820 |

| 6. Principal market | The market used to arrive at fair value measurement |

For unrecognized services: While not required to quantify the value, you must describe the nature and extent of contributed services received. Example note disclosure:

"During the year, the Organization received pro-bono legal services from board members and community volunteers valued at approximately 200 hours. These services did not meet the criteria for recognition under ASC 958-605 because the Organization would not have otherwise purchased the services."

Practical Recommendation

Develop or update a written contributed services policy covering:

- Recognition criteria and decision framework

- Valuation methods and documentation requirements

- Approval process for accepting and recording contributed services

- Disclosure procedures and annual review schedule

Review this policy annually and make sure your finance team applies it consistently. Nonprofits without dedicated finance staff often benefit from a fractional CFO who can build these policies from scratch and keep them current — which is exactly the kind of work One Abacus Advisory does with organizations navigating audit preparation and compliance.

Frequently Asked Questions

How do you account for donated services?

Qualifying donated services (meeting all three GAAP criteria) are recorded as a simultaneous debit to the appropriate expense account and credit to in-kind contribution revenue. The entry is made at fair market value on the date the service is rendered, creating a net-zero impact on net assets but increasing both total revenue and total expenses.

Do nonprofits have to report in-kind donations?

In-kind donations of goods must be reported on Form 990 (Part VIII, line 1g), but contributed services are explicitly excluded from those revenue and expense lines — they appear only in GAAP financial statements as a reconciling item on Form 990 Part XI, Line 6. Note disclosure is still required even for services that don't meet formal recognition criteria.

How do you record donations received in nonprofit accounting?

Cash donations are recorded as a debit to cash and credit to contribution revenue, classified by net asset category. In-kind contributions are recorded as a simultaneous debit to the relevant expense or asset account and credit to in-kind contribution revenue at fair market value. Recognition timing depends on any donor-imposed conditions.

Is donating services to a nonprofit tax deductible?

No. The value of donated services is NOT tax-deductible for the donor, per IRS Publication 526. Only unreimbursed out-of-pocket expenses directly incurred while performing the service (such as mileage at 14 cents per mile or materials purchased) may qualify for deduction. Nonprofits should not issue charitable gift receipts for the service value itself.

What is the best accounting method for nonprofit organizations?

Accrual-basis accounting is the preferred method for nonprofits because it properly captures pledges, contributed services, deferred revenue, and other transactions in the period they are incurred. Accrual basis is required for GAAP compliance, audited financial statements, and accurate contributed service recognition. Cash-basis accounting does not capture noncash transactions like contributed services at all.

Need help navigating contributed services accounting or preparing for your next audit? One Abacus Advisory provides fractional CFO and accounting optimization services tailored to nonprofits — from ASU 2020-07 disclosures and GAAP-to-Form-990 reconciliation to audit preparation and in-kind accounting clarity. With over 25 years of nonprofit financial experience, our team delivers compliance-ready, transparent reporting practices built around your mission. Schedule a free consultation to discuss your organization's specific needs.